Roofing Pricing Guide: How to Price Your Jobs Profitably

How roofing contractors should price their work — covering cost per square, overhead recovery, material markup, insurance claims, and mistakes that erode margin.

Most roofing contractors have a solid handle on installation technique but a shakier grip on whether the price they quoted will actually make money.

The pricing mechanics in roofing are different from other trades. The industry has its own unit of measure, its own labor productivity benchmarks, and a whole category of work — insurance restoration — that runs on insurance company software and requires a different skill set entirely. Getting pricing right requires understanding all three.

The Roofing Square: The Unit Everything Else Builds On

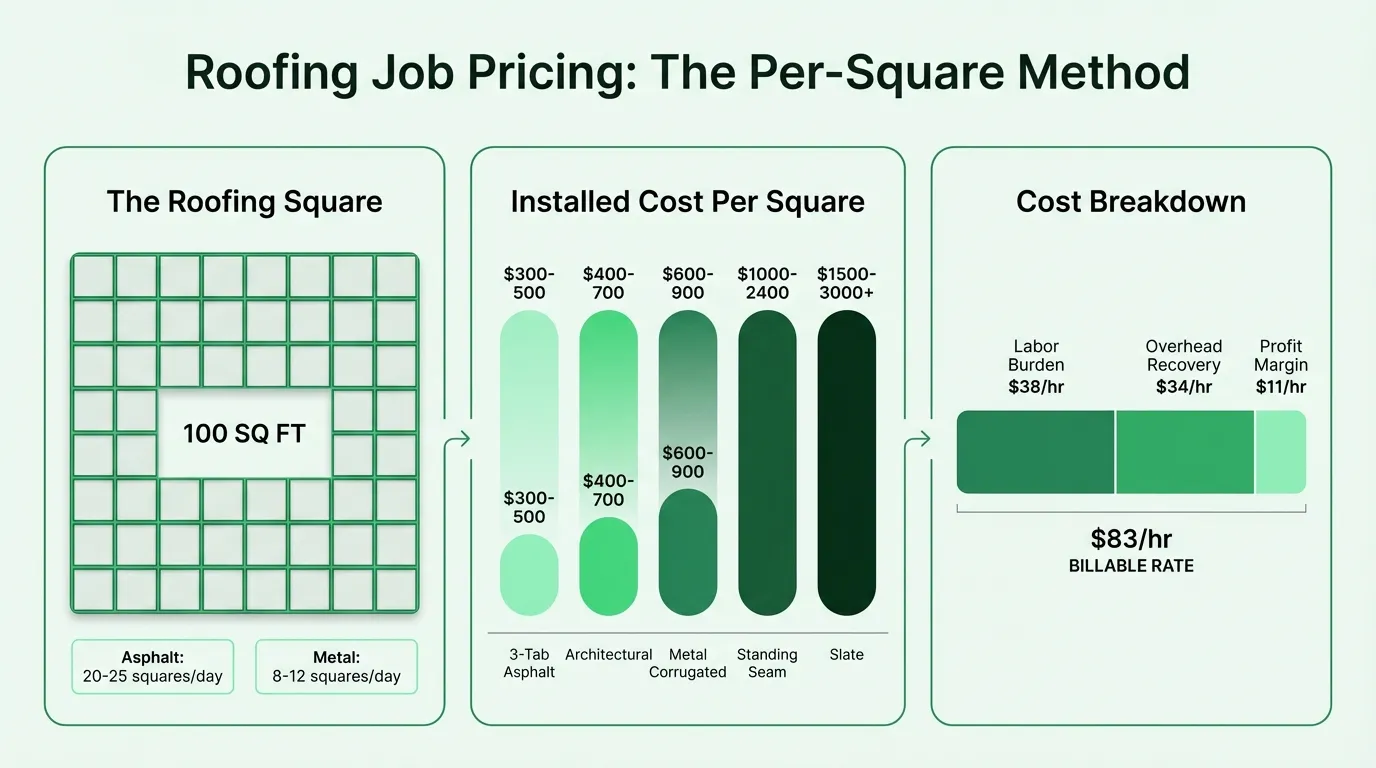

A roofing square equals 100 square feet of roof surface. It's the standard measurement unit for estimating, bidding, ordering materials, and quoting customers across the entire industry, both residential and commercial.

The reason per-square pricing dominates over hourly is practical: once you know the number of squares, material needs are largely fixed and labor productivity is predictable. An experienced crew installs 20–25 squares of asphalt shingles per day on a simple roof. Metal roofing runs 8–12 squares per day. Tile and slate come in at 4–8 squares per day due to the weight, care, and precision involved.

These benchmarks let you build a price from the ground up rather than guessing.

Installed Cost Per Square by Material

What contractors charge for a complete installation (labor plus materials) varies significantly by material type:

| Material | Installed Cost Per Square |

|---|---|

| 3-tab asphalt shingles | $300–$500 |

| Architectural asphalt shingles | $400–$700 |

| Premium/designer asphalt | $600–$900 |

| Metal (corrugated/ribbed) | $600–$900 |

| Standing seam metal | $1,000–$2,400+ |

| Concrete tile | $1,000–$1,400 |

| Clay tile | $1,200–$1,800 |

| Slate | $1,500–$3,000+ |

| TPO (flat/low-slope) | $500–$1,500 |

These are total installed prices — what the customer pays — not contractor costs. Your cost structure sits underneath these numbers and determines whether you're making money at a given price point.

One additional cost that many contractors miss: tear-off. Removing an existing roof adds $1–$3 per square foot in labor, plus dumpster rental. Multi-layer tear-offs add another $25–$60 per square depending on how many layers and the material type. If you're not including tear-off as a separate line item in estimates, you're burying a real cost somewhere else — usually in margin.

Building a Billable Rate

Roofing contractors charge customers $75–$100 per hour on time-and-materials work. The average roofer earns $21–$24 per hour in wages. The gap between those two numbers isn't pure profit — it's what's needed to cover the actual cost of running a roofing business.

Here's why.

Labor burden. A roofer earning $22/hour costs significantly more than $22/hour to employ. Add employer payroll taxes (7.65%), workers' compensation insurance (the biggest variable in roofing), health benefits, and paid time off, and the true employment cost rises to $32–$45/hour before any overhead.

Workers' compensation is the number that surprises most roofing contractors when they first look at it closely. Roofing falls under NCCI Class Code 5551, one of the highest-risk classifications in construction. Workers' comp rates run $9.90–$15.25 per $100 of payroll nationally, with high-cost states like California reaching $24–$80 per $100. On a $22/hour wage, California workers' comp alone can add $5–$18 per hour to labor cost.

Overhead. Every hour of field work needs to carry a share of all non-job costs: vehicles and fuel, general liability insurance (typically $267/month for a small roofing company), commercial auto, tools and equipment, office rent, software, marketing, and administrative time.

A small roofing operation with $800–$1,000/month in insurance costs alone, plus vehicles, office, and admin, can easily carry $150,000–$200,000 in annual overhead. Spread across realistic billable hours (not theoretical capacity — actual hours billed, after accounting for quoting time, drive time, and weather delays), that translates to $30–$40 per billed hour of overhead recovery needed.

The Rate Calculation

| Component | Amount |

|---|---|

| Fully loaded field wage | $38/hr |

| Overhead recovery | $34/hr |

| Break-even cost | $72/hr |

| Profit (15%) | $11/hr |

| Billable rate | $83/hr |

A contractor charging $65/hour at this cost structure is losing money on every hour billed, regardless of how busy they are. Test your own numbers with the roofing break-even calculator to find the minimum rate your overhead supports. Per-square pricing should reflect the same structure — calculate your actual labor cost per square (hours × loaded rate), add materials with markup, add overhead, add profit.

Material Markup

Materials should never be priced at cost. Purchasing, transporting, staging, and managing materials has real costs, and contractors take on price risk and warranty responsibility that suppliers don't.

Standard markup ranges for roofing materials:

| Material Category | Typical Markup |

|---|---|

| Standard shingles, felt, standard underlayment | 20–35% |

| Specialty materials (metal panels, clay tile) | 35–40% |

| Small consumables (flashing, fasteners, sealants) | 40–50% |

One formula error that costs roofing contractors real money: markup and margin are not the same thing.

A 25% markup on $400 in materials yields a $500 price — but that's a 20% gross margin, not 25%. To hit a specific margin target, the correct formula is:

Selling Price = Cost ÷ (1 – Target Margin)

For a 30% gross margin on $400 in materials: $400 ÷ 0.70 = $571.43. Using markup percentages when you mean margin consistently leaves money on the table, especially on larger jobs.

Also factor in waste. Simple roofs need 10–15% extra material for cuts and overlaps. Complex roofs with hips, valleys, dormers, and multiple penetrations need 15–20%+. Ordering tight and running short costs more than ordering right the first time. The roofing markup calculator converts between markup and margin targets so your material pricing is precise.

Residential vs. Commercial Roofing

Residential and commercial roofing aren't just different job sizes — they're different businesses with different materials, equipment, margin profiles, and financial structures.

Residential replacement is typically asphalt shingles on sloped roofs — 1-to-3-day jobs, familiar material, predictable productivity. Margins run 20–35% gross on replacements, 30–50% on repairs.

Commercial roofing predominantly involves flat or low-slope systems: TPO, EPDM, modified bitumen, built-up roofing. These require specialized equipment — hot air welding machines for TPO alone can cost tens of thousands of dollars — and different installation skills.

Commercial margins run 10–20% gross — lower percentage, but the revenue per job is much higher. The tradeoff:

- Payment terms. Commercial clients often pay net-30 to net-90. You're financing material and labor costs for weeks or months before the check arrives. On a $150,000 commercial job, that's real capital tied up.

- Insurance requirements. Commercial work often requires $2M–$10M in general liability limits and contractor bonds. These are overhead costs that don't apply to residential work.

- Equipment capital. The hot air welders, spray rigs, and specialized lifts required for commercial flat roofing represent significant capital investment before the first job is bid.

If you're doing both residential and commercial work, price them with separate overhead models. Running a blended rate will either price you out of residential work or underprice your commercial work — almost always the latter.

Need a ready-made budget template for your roofing?

Download a pre-built spreadsheet with industry-specific categories, formulas, and formatting.

Insurance Restoration Work

Storm damage claims represent a significant portion of the residential roofing market in hail-prone and hurricane-affected regions. But insurance work has its own financial mechanics that catch underprepared contractors off guard.

Insurance companies estimate claims using Xactimate software, which generates scope-of-work estimates based on regional pricing databases. These estimates are a starting point — not a final number, and not always an accurate reflection of what jobs actually cost.

Initial insurance estimates routinely miss line items: dumpster rental, permit fees, code-upgrade requirements (drip edge, ice and water shield, ridge vent replacements), specific flashing components, and tear-off complexity for multi-layer roofs. A contractor who signs the initial estimate without reviewing it absorbs these missing costs out of margin.

The supplement process is how contractors recover their true costs. A supplement is a formal submission to the insurance adjuster requesting additional payment for line items missing from the initial estimate. Contractors who understand supplementing — and document their work with photos before, during, and after — recover what they're owed. Those who don't subsidize the insurance company's initial underestimate.

The industry-recognized structure for overhead and profit on insurance work is 10% overhead plus 10% profit on top of direct costs — the "10/10" standard most adjusters acknowledge when a general contractor is coordinating multiple trades.

Common Pricing Mistakes

Not knowing your overhead rate. If you don't know what your annual overhead costs, and if you don't know how many hours your crews actually bill (not how many they work), you can't know whether your prices cover costs. This is the most common and most costly gap.

Measurement errors. Measurement mistakes typically add 7–15% to material costs when not caught before ordering. The industry has shifted to satellite and drone measurement tools precisely because manual measurement on complex roofs is error-prone. Estimate the wrong square footage and you've priced the wrong job.

Forgetting multi-layer tear-off costs. A single-layer tear-off and a three-layer tear-off are not the same job. Missing the extra $25–$60 per square on a multi-layer tear-off on a 25-square roof is a $625–$1,500 underestimate on a single job.

Single-option estimates. Presenting only one price means you've already decided what the customer wants. Tiered pricing — good/better/best across shingle grades or warranty levels — lets customers self-select. Industry data shows that contractors using tiered pricing are roughly twice as likely to have customers choose their highest-value option.

Scope creep without change orders. Additional work on a fixed-price job — replacing decking boards found during tear-off, adding ventilation discovered to be inadequate — must have a written change order at an agreed price before work starts. "While you're already here" is revenue if documented. It's a donation if it's not.

Tracking Whether Your Pricing Works

Pricing improves through feedback. Track these numbers on completed jobs:

- Gross profit margin per job (revenue minus direct labor and materials, divided by revenue). Target: 20–35% on residential replacement. If you're consistently landing at 10–12%, your estimates are off somewhere — usually labor hours or overlooked tear-off costs.

- Labor hours: estimated vs. actual. If jobs regularly run over estimate, adjust time assumptions for similar future work. Systematically over-running estimates means your flat prices are underpriced.

- Material cost variance. What you estimated vs. what you spent. Large unfavorable variances often point to missed waste factors, multi-layer tear-off complexity, or code-upgrade items that weren't in the original bid.

The Roofing Budget Template provides a job-costing structure for tracking estimated vs. actual costs across labor, materials, and subcontractors. For a broader financial view of your business, the Roofing Income Statement Template gives you a model built around how roofing contractor finances actually work, with separate lines for residential and commercial margins.

The Starting Point

The contractors consistently making money at roofing share one characteristic: they know their numbers. They know their overhead rate, their loaded labor cost, and their actual crew productivity on each material type. That knowledge converts to prices that hold up under scrutiny and produce real margin.

If you're not sure whether your current pricing covers costs, start with the overhead calculation above. Add up annual overhead, divide by actual billable field hours, and check whether that number is showing up in your estimates. Most contractors who run this exercise for the first time find the answer useful — even if it's uncomfortable.

Last updated: March 25, 2026

Frequently Asked Questions

Related Articles

Auto Repair Pricing Guide: How to Price Your Shop Profitably

How auto repair shop owners should price labor and parts — covering labor rate calculation, flat-rate hours, parts markup matrices, diagnostic fees, and the metrics that matter.

Cleaning Service Pricing Guide: How to Price Your Business Profitably

A practical guide to cleaning service pricing — covering hourly vs. flat rate vs. per square foot models, price benchmarks by service type, labor cost math, and the common mistakes that keep cleaning businesses from hitting their margin targets.

Construction Pricing Guide: How to Price Your Work Profitably

How contractors should price construction work — covering labor burden, overhead recovery, material markup, pricing methods, and the mistakes that quietly erode margin.

Electrical Pricing Guide: How to Price Your Work Profitably

How electricians and electrical contractors should price their work — covering hourly rates, flat-rate pricing, overhead recovery, material markup, and common mistakes that erode margin.

Hotel Sales Forecast: A Practical Example and Guide

How to build a hotel sales forecast — covering rooms, F&B, events revenue, key metrics like RevPAR and ADR, booking pace, and the rolling forecast structure that keeps you ahead.

Landscaping Pricing Guide: How to Price Your Work Profitably

A practical guide to landscaping pricing — covering hourly rates, per-square-foot benchmarks, overhead recovery, and the markup math that determines whether you're making money.