Construction Pricing Guide: How to Price Your Work Profitably

How contractors should price construction work — covering labor burden, overhead recovery, material markup, pricing methods, and the mistakes that quietly erode margin.

Most construction contractors are skilled tradespeople running undercapitalized businesses. They know how to build things. They're less certain about whether the price they quoted will actually cover their costs — let alone produce a profit.

The result shows up in the numbers. According to CFMA benchmark data, the average construction contractor nets around 6.3% of revenue before taxes. The top 25% reach nearly 12%. The gap isn't usually in field execution. It's usually in how contractors price their work.

This guide covers the mechanics of profitable construction pricing: how to build a labor rate, how to recover overhead, how to mark up materials and subcontractors, and how to choose the right contract structure for a given job.

The Four Pricing Methods

Most contractors use more than one pricing approach depending on job type and client.

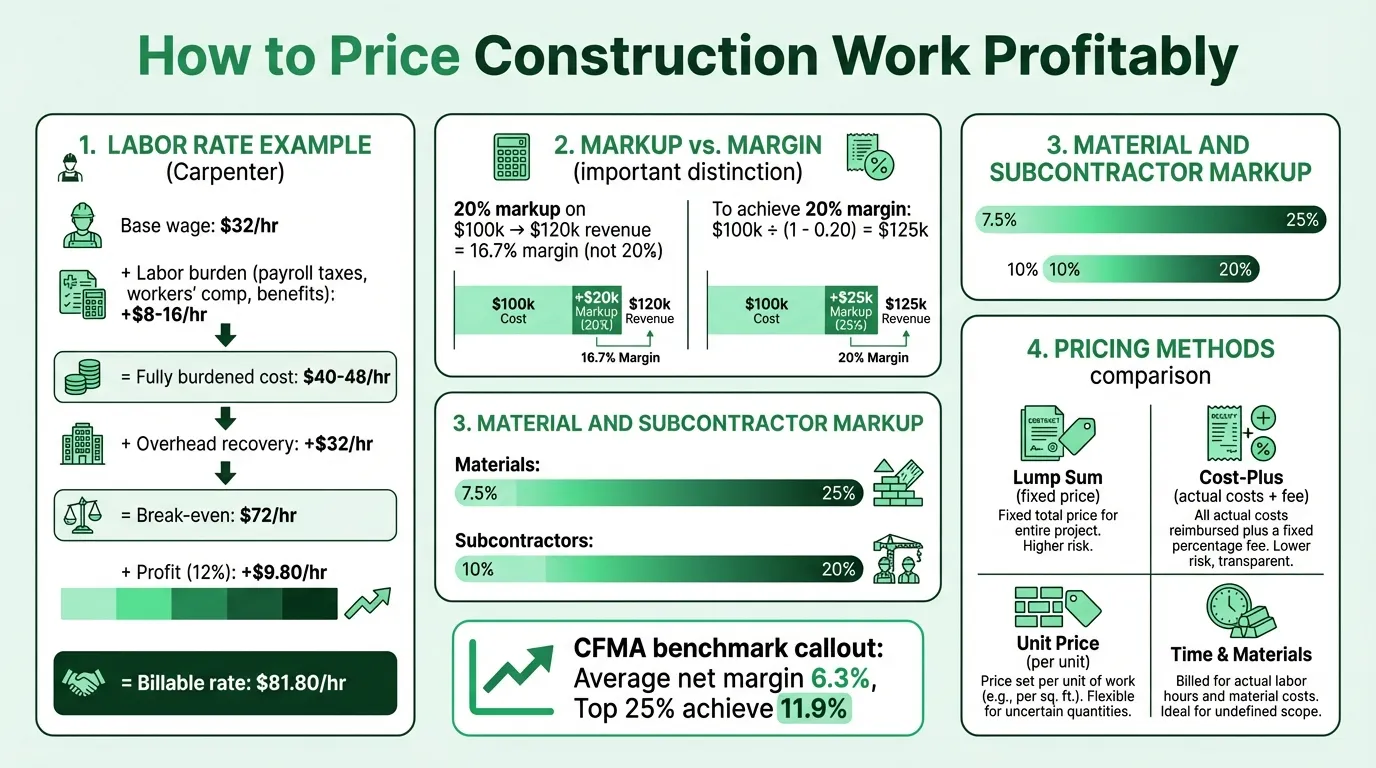

Lump sum (fixed price) gives the owner a single price for a defined scope. If you finish under budget, you keep the savings. If costs run over, you absorb the overrun. This is appropriate when the scope is well-defined, drawings are complete, and you have enough history with similar work to estimate accurately. On a poorly defined project, lump sum pricing forces you to load contingency into the price or risk eating overruns.

Cost-plus charges the owner for actual labor and material costs, plus a fixed fee or percentage for overhead and profit. The owner has cost transparency and bears cost risk — the contractor earns the fee regardless of how efficiently the work goes. Common on complex, fast-track, or relationship-based projects where the owner values transparency over price certainty.

Unit price sets a price per measurable unit of work — per linear foot of pipe, per cubic yard of concrete, per square foot of framing. Each unit price is all-inclusive: direct costs, overhead, and profit. Used heavily on public infrastructure and work where quantities aren't fully known at bid time. The total contract value scales up or down as actual quantities are measured.

Time and materials (T&M) bills for hours worked at a predetermined labor rate plus actual material costs with markup. The labor rate is supposed to embed overhead and profit, not just wages. Common for service and repair work, change orders, or jobs where scope won't be clear until work is underway. Without a not-to-exceed cap, the owner carries open-ended cost exposure.

No method is inherently right or wrong. What matters is that whichever you use, the numbers inside it are based on your actual costs — not a competitor's rate, not a round number that "sounds about right."

Why Your Hourly Rate Isn't Your Wage

The most expensive pricing mistake in construction: building a labor rate around desired take-home pay instead of actual business costs.

Here's the problem. A carpenter paid $28/hour in wages doesn't cost $28/hour to employ. Add employer payroll taxes (7.65%), workers' compensation insurance (construction trades typically run 8–20% of wages depending on trade and state), health benefits, paid time off, and tool allowances, and the fully burdened labor cost lands at $38–$45/hour for a non-union contractor. Union contractors carry a labor burden of 60–70% of wages due to fringe benefit packages.

Then there's overhead — every business cost that isn't direct labor or direct material on a specific job.

Building the Overhead Recovery Rate

Total overhead includes:

- Vehicle payments, fuel, insurance, and maintenance

- General liability insurance and contractor bonds

- Office rent, utilities, accounting, and software

- Licensing fees, continuing education, and permits

- Estimating time, marketing, and administrative salaries

- Warranty callbacks and rework

Smaller contractors ($0–$50M revenue) typically run overhead at 20–25% of revenue. Mid-size firms ($50M–$100M) run 15–20%. The widely cited industry target — the "ten-ten rule" — aims for 10% overhead and 10% profit as a minimum baseline.

To calculate overhead recovery per billable hour:

- Add up annual overhead. Every cost that isn't direct labor or material on a job. Say that totals $180,000.

- Calculate realistic billable hours. Not theoretical capacity — actual billable hours, accounting for non-billable time (quoting, travel, training, administrative tasks). If you have four field workers and each bills about 1,400 hours, that's 5,600 billable hours.

- Divide. $180,000 ÷ 5,600 = $32.14 overhead per billable hour. That amount must be in every labor hour you sell.

| Component | Amount |

|---|---|

| Fully burdened labor cost | $40/hr |

| Overhead recovery | $32/hr |

| Break-even cost | $72/hr |

| Profit (12%) | $9.80/hr |

| Billable rate | $81.80/hr |

A contractor charging $65/hour on this cost structure loses money on every hour billed — regardless of how busy they are. Use the construction break-even calculator to find the minimum rate and volume where your business stops losing money.

Material and Subcontractor Markup

Materials should never be priced at cost. Purchasing materials, storing them, transporting them to site, handling returns and defects, and managing supplier relationships all have real costs. Contractors also carry the risk of price volatility — and on larger jobs, they're effectively financing materials for 30–60 days before the owner pays.

Typical markup ranges:

| Material Category | Typical Markup |

|---|---|

| Standard framing, lumber, general materials | 15–25% (residential), 7.5–10% (large commercial) |

| Specialty materials and finishes | 20–30% |

| Small consumables | 30–50% |

Subcontractor markup covers coordination, management, schedule oversight, and — critically — the liability the GC assumes for subcontractor work and warranty. GCs typically add 10–20% to subcontractor billings. On custom residential work, a 20% markup on all hard costs (labor, materials, subs) is standard.

One formula issue that trips up many contractors: markup and margin are not the same thing.

- A 20% markup on $100,000 in costs yields $120,000 revenue — that's a 16.7% gross margin, not 20%.

- To hit a target margin, use:

Selling Price = Cost ÷ (1 – Target Margin) - For a 20% gross margin: $100,000 ÷ (1 – 0.20) = $125,000

Contractors who quote margins as markups consistently underprice their work. On a $2M project, that confusion means leaving $40,000–$60,000 on the table. Run both numbers side by side with the construction markup calculator to see the difference on your actual jobs.

Need a ready-made budget template for your construction?

Download a pre-built spreadsheet with industry-specific categories, formulas, and formatting.

Residential vs. Commercial Pricing

Residential and commercial construction operate on different economic structures. Running a blended rate across both will either price you out of residential work or underprice commercial — usually the latter.

Gross margins: Residential contractors typically achieve 18–25% gross margin. Commercial GCs run 10–20%, with industrial and heavy work compressing further to 8–15%.

Why residential margins are higher:

- Smaller project scale means overhead absorbs as a higher percentage of each job

- Repeat-customer dynamics support premium pricing

- Less competitive bidding pressure than public commercial work

Why commercial requires different pricing:

Bonding and insurance. Residential work typically requires $1M in general liability. Commercial jobs often mandate $2–25M, plus contractor performance and payment bonds. These are real overhead costs that residential pricing doesn't need to cover.

Payment terms. Residential clients often pay on delivery milestones within weeks. Commercial clients pay net-30 to net-60 on approved pay applications. On a $500,000 subcontract, you may be financing six weeks of labor and materials before the first check clears. That cost of capital has to come from somewhere.

Prevailing wage. Any public or federally funded project may require prevailing wage rates — set by the Davis-Bacon Act and similar state laws — which can run 40–80% above standard market wages depending on trade and location. Bidding a prevailing wage job at standard labor rates is a losing proposition.

Documentation overhead. Submittals, as-built drawings, RFI responses, certified payrolls, change order documentation — none of this is billable field time, but all of it consumes hours. This overhead doesn't disappear; it shows up as unbilled time against your billable hour count.

If you're tracking job-level profitability across both residential and commercial work, the Construction P&L Template gives you a clean structure for separating revenue and costs by job type.

Common Pricing Mistakes

Underestimating labor burden. This is the most common and most costly mistake. Using base wage rates in estimates without adding payroll taxes, workers' comp, and benefits understates labor cost by 25–70% depending on whether you're union or non-union.

Not recovering overhead. Many contractors include direct job costs in estimates but fail to add overhead. If a $400,000 job has $320,000 in direct labor and materials, the 20% remaining has to cover overhead and profit. If overhead alone runs 18% of revenue, there's nothing left.

Using outdated material pricing. Construction material prices — lumber, steel, copper, concrete — move constantly. A quote built on supplier pricing from three months ago may be significantly wrong. Price materials from current quotes, especially on jobs with longer lead times between bid and start.

Ignoring contingency. Industry practice suggests 5–15% contingency depending on project complexity and how developed the drawings are. Contractors who skip contingency absorb unforeseen conditions — soil problems, unknown utilities, existing structure surprises — directly against margin.

Scope creep on fixed-price work. "While you're already here" is the most expensive phrase in construction. Every addition to a lump sum scope is a change order. Without a written change order at an agreed price before work starts, additional work becomes a donation. Track changes to scope from the moment they're mentioned.

Confusing busy with profitable. A full backlog is reassuring but not the same as profitability. If you're fully booked at rates that don't recover overhead, being busier makes the loss bigger. Tracking gross profit margin by job — not just revenue and total costs — tells you which work is actually profitable. The construction income statement example shows how job-level margins roll up into company-wide performance.

Job Costing: The Feedback Loop

Pricing decisions only improve if you track actual vs. estimated costs on completed jobs. The three numbers to watch:

Gross profit margin by job. Revenue minus direct labor and materials, divided by revenue. If you target 20% gross margin and regularly land at 12–14%, your estimates are systematically off somewhere — usually labor productivity, scope interpretation, or untracked change orders.

Labor hours: estimated vs. actual. If jobs consistently run over estimated hours, your time estimates need to go up. If they consistently come in under, you're padding estimates and possibly leaving bids on the table.

Material cost variance. What you estimated vs. what you actually spent. Large favorable variances may indicate over-estimated materials; large unfavorable variances often point to scope changes not captured as change orders, waste, or rework. The Construction Expense Tracker Template helps you log material costs in real time against budget categories.

The Construction Budget Template gives you a job-cost structure to track estimated vs. actual across labor, materials, and subcontractors by phase. Running that comparison on every completed job — even a quick version — is how pricing improves over time.

What the Numbers Say

According to CFMA data, the average construction contractor earned 6.3% net income before taxes in 2023 — the best performance in recent years. The top 25% of contractors earned 11.9%. The gap between average and top-quartile performance is almost entirely explained by pricing discipline and overhead management, not technical skill.

The contractors who consistently hit the high end of the range are not doing more complex work. They know their overhead rate. They track labor burden accurately. They run job cost reports regularly. And they don't confuse markup with margin.

If you're not sure where your current pricing stands, start with the overhead calculation in Step 3 above. Calculate your actual overhead recovery rate per billable hour and compare it to what you're including in estimates. That single comparison usually tells you what you need to know.

For a more complete view of construction company finances — revenue by job type, overhead allocation, and net income tracking — the Construction Income Statement Template provides a financial model built around how construction businesses actually work.

Last updated: March 25, 2026

Frequently Asked Questions

Related Articles

Auto Repair Pricing Guide: How to Price Your Shop Profitably

How auto repair shop owners should price labor and parts — covering labor rate calculation, flat-rate hours, parts markup matrices, diagnostic fees, and the metrics that matter.

Cleaning Service Pricing Guide: How to Price Your Business Profitably

A practical guide to cleaning service pricing — covering hourly vs. flat rate vs. per square foot models, price benchmarks by service type, labor cost math, and the common mistakes that keep cleaning businesses from hitting their margin targets.

Electrical Pricing Guide: How to Price Your Work Profitably

How electricians and electrical contractors should price their work — covering hourly rates, flat-rate pricing, overhead recovery, material markup, and common mistakes that erode margin.

Hotel Sales Forecast: A Practical Example and Guide

How to build a hotel sales forecast — covering rooms, F&B, events revenue, key metrics like RevPAR and ADR, booking pace, and the rolling forecast structure that keeps you ahead.

Landscaping Pricing Guide: How to Price Your Work Profitably

A practical guide to landscaping pricing — covering hourly rates, per-square-foot benchmarks, overhead recovery, and the markup math that determines whether you're making money.

Manufacturing Inventory Management: Best Practices

Practical manufacturing inventory management best practices — covering ABC analysis, MRP, WIP control, safety stock, and the metrics that matter most on the shop floor.