Restaurant Payroll Tips: Cut Costs and Stay Compliant

Practical restaurant payroll tips covering labor cost benchmarks, tip credits, overtime rules, FICA tip credit, and common mistakes operators make.

Labor is the largest controllable cost in most restaurants, and also the one with the most compliance complexity. For full-service restaurants, wages and benefits averaged 36.5% of sales in 2024, per National Restaurant Association data — up from the historical average near 33%. For limited-service operators, the figure was 31.7%, compared to a historical average near 28%.

Those numbers are high enough that a restaurant running even two or three percentage points above target — through scheduling inefficiency, payroll errors, or missed tax credits — can turn a marginal operation into a losing one. This guide covers the payroll mechanics, compliance requirements, and common mistakes that have the biggest impact on restaurant operators.

Know Your Labor Cost Target Before You Optimize

Before trying to reduce labor cost, establish where you actually are. Labor cost percentage is wages plus benefits divided by total sales.

Labor Cost % = Total Labor Cost ÷ Total Sales

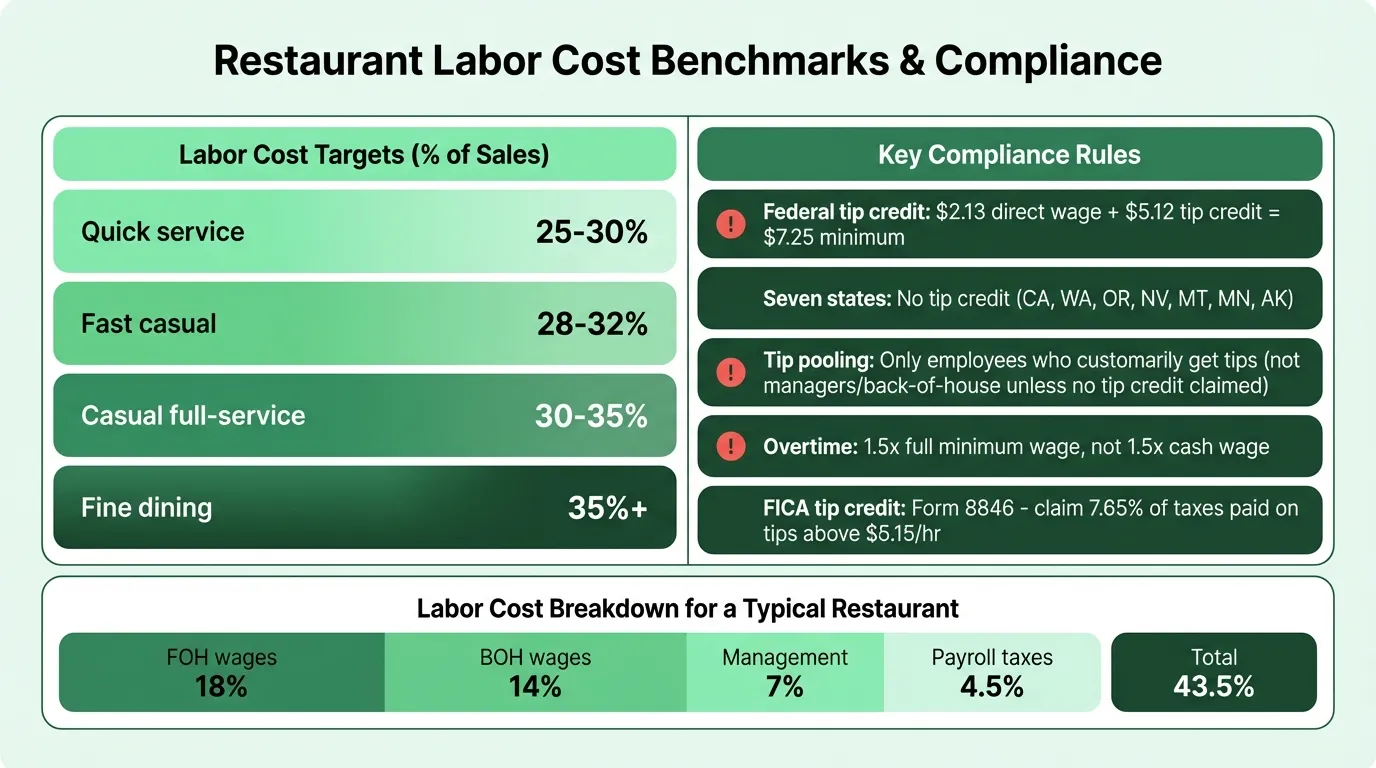

Industry benchmarks by segment:

| Segment | Labor Cost Target (% of sales) |

|---|---|

| Quick service / fast food | 25–30% |

| Fast casual | 28–32% |

| Casual full-service | 30–35% |

| Fine dining | 35%+ |

NRA 2024 data shows the gap between profitable and unprofitable operators is visible in labor cost. Profitable limited-service restaurants averaged 30.0% labor cost; those reporting losses averaged 34.1%. That 4-point difference on a restaurant doing $1.5M in annual sales is $60,000 — the difference between a modest profit and a significant loss.

Labor cost alone is only part of the picture. Prime cost — food cost plus labor combined — is the more complete profitability indicator. Target 55–65% of sales. A restaurant running 32% food cost and 38% labor has a 70% prime cost, which leaves 30% of revenue to cover rent, utilities, and everything else. That margin doesn't support a viable business at most revenue levels. The restaurant break-even calculator shows the revenue level required to cover fixed costs at different prime cost percentages.

Track both metrics monthly in your P&L. The Restaurant P&L Template structures these line items so prime cost is visible each month without manual calculation.

The Federal Tip Credit: How It Works and What It Requires

Under the Fair Labor Standards Act, employers can pay tipped employees a direct cash wage of $2.13 per hour — lower than the $7.25 federal minimum wage — and count employees' tips toward making up the difference. This is called the tip credit, and the maximum tip credit is $5.12 per hour ($7.25 − $2.13).

The tip credit is only valid under specific conditions:

- The employee must be a tipped employee — meaning they regularly earn $30 or more per month in tips

- The employer must notify the employee of the tip credit arrangement before it applies

- The employee must actually receive enough in tips to bring total compensation to $7.25 per hour for every workweek. If tips fall short in any week, the employer must make up the gap on that paycheck — not at the end of the quarter or year

The tip credit is not available in seven states: Alaska, California, Minnesota, Montana, Nevada, Oregon, and Washington. These states require the full state minimum wage regardless of tips. If you operate in any of these states, all employees — tipped or not — are paid the same minimum hourly rate.

The dual jobs rule (restored December 2024)

The Department of Labor restored the dual jobs rule in late 2024: you can only claim the tip credit for hours an employee works in a tipped occupation. If you assign a server to extended side work — cleaning, stocking, prep — beyond what's incidental to serving, those hours must be paid at the full minimum wage.

In practice, this means tracking when tipped employees switch to non-tipped tasks and ensuring the tip credit isn't applied to that time. POS-integrated time-tracking software handles this automatically; manual scheduling creates compliance exposure.

Tip Pooling: What's Allowed

Tip pooling lets employers require tipped employees to contribute a portion of their tips to a shared pool distributed among eligible employees. The rules:

- Who can participate: Employees who customarily and regularly receive tips — servers, bartenders, bussers, counter staff

- Who cannot participate: Managers, supervisors, or any employee with authority over hiring, firing, or discipline. This is firm under the FLSA and DOL enforcement guidance

- Back-of-house: Cooks, dishwashers, and prep staff can only join a tip pool if the employer pays all employees the full minimum wage and claims no tip credit. If you're claiming the tip credit, back-of-house is excluded from the pool entirely

One distinction many operators get wrong: service charges (the mandatory 18% gratuity on large parties, or a house fee added to every check) are not tips. They're wages. They belong to the employer to distribute as they see fit, they're subject to regular payroll taxes, and they don't qualify for the FICA tip credit. An employer can choose to pass service charges to employees, but those amounts are taxed as regular wages — not as tips.

The FICA Tip Credit: A Tax Benefit Most Restaurants Miss

The FICA tip credit — filed using IRS Form 8846 — allows food and beverage employers to claim a federal tax credit equal to the employer's share of FICA taxes (7.65%) paid on employee tips above the federal minimum wage threshold ($5.15/hour in the credit calculation).

The mechanics:

- For every dollar in tips above $5.15/hour that employees receive, the employer pays 7.65% in FICA taxes. The credit reimburses that tax expense

- The credit applies only to tips, not to the direct wages paid to tipped employees

- It's filed annually as part of the employer's federal tax return

For a restaurant where servers collectively earn $300,000 in tips annually above the threshold, the FICA tip credit is roughly $22,950. That's a direct dollar-for-dollar reduction in federal tax liability — not a deduction.

Despite being one of the more valuable restaurant-specific tax benefits available, it's one of the most commonly missed. Many small restaurant operators don't know it exists. Work with an accountant who specializes in restaurants to ensure Form 8846 is filed correctly — the restaurant accounting tips guide covers what to look for when choosing a restaurant-experienced CPA.

Note on 2025–2026 changes: Federal tax legislation passed in 2025 allows tipped employees to deduct up to $25,000 annually in qualified tip income from their personal federal income tax. This doesn't change employer payroll obligations — FICA withholding and employer FICA contributions on tip income are unchanged. Restaurants will have new W-2 reporting requirements for tip income and overtime beginning in 2026.

Need a ready-made budget template for your restaurant?

Download a pre-built spreadsheet with industry-specific categories, formulas, and formatting.

Overtime Rules for Tipped Employees

Overtime for a tipped employee is calculated at 1.5 times the full minimum wage — not the cash wage you actually pay them.

At the federal minimum wage of $7.25:

- Regular rate: $7.25/hour

- Overtime rate: $10.88/hour (1.5 × $7.25)

This applies regardless of what you pay in direct wages. A server earning $2.13/hour in direct wages plus tips still has an overtime rate of at least $10.88/hour.

A common error: applying the 1.5x multiplier to the $2.13 cash wage and calculating overtime at $3.20/hour. That's a compliance violation and back-pay exposure.

If an employee works multiple roles in the same workweek — server for 30 hours, then dishwasher for 15 hours — all hours count toward the 40-hour overtime threshold. The overtime rate applies to the blended regular rate across all roles.

Common Payroll Mistakes That Cost Money

1. Missing the tip credit shortfall. The requirement to make up any minimum wage shortfall applies per workweek, not per pay period. A biweekly payroll run can mask weeks where a slow Tuesday meant tips fell short. Run a weekly check confirming each tipped employee's total compensation clears minimum wage.

2. Including service charges in tip pool calculations. Service charges are wages; tips are tips. Mixing them distorts tip pool distributions and creates tax reporting errors.

3. Not filing Form 8846. A straightforward annual tax credit that many small operators don't know to claim. Ask your accountant specifically about it.

4. Manual time tracking. 27% of restaurants still use manual scheduling despite available software. Manual tracking introduces errors in overtime calculation, dual jobs rule compliance, and tip credit eligibility. At an average direct cost of $291 per payroll error, this is a measurable expense.

5. Misclassifying employees as contractors. Common with delivery staff, catering servers, and part-time help. The IRS and DOL use a multi-factor test — behavioral control, financial control, and relationship type — to determine employment status. Misclassification triggers back taxes, penalties, and exposure to wage claims.

6. Using the wrong overtime base for salaried managers. Non-exempt salaried employees (managers whose annual salary doesn't meet the FLSA threshold) are entitled to overtime at 1.5x their regular rate. The regular rate for a salaried employee is their weekly salary divided by the hours that salary is intended to compensate.

Building a Payroll System That Works

A few structural decisions reduce payroll complexity and compliance risk over time:

Weekly payroll cycles. Industry data from RASI shows a 26% increase in employee retention for restaurants running weekly payroll. Employees in hourly jobs have less financial buffer than salaried workers; faster access to earnings improves stability and reduces voluntary turnover. Weekly payroll also surfaces tip shortfall errors every seven days instead of every fourteen.

POS-integrated time tracking. When clock-in/clock-out data flows directly from your POS to payroll, you eliminate manual data entry, capture credit card tips automatically, and get accurate overtime calculations without spreadsheet reconciliation.

A tip credit eligibility review each pay period. Run a report confirming that every employee using the tip credit met the minimum wage threshold for every workweek in the period. This takes five minutes with proper payroll software and eliminates the compliance exposure from undetected shortfalls.

Clear documentation of tip pooling. Write down the pool structure, eligible participants, and distribution formula. Post it where staff can see it. If the DOL ever investigates a tip pooling complaint, documentation of a compliant structure is your first line of defense.

How Payroll Fits Into the Overall Financial Picture

Payroll is your largest controllable expense line, but it exists in the context of your full cost structure. A restaurant managing labor to 32% while food cost runs 38% still has a 70% prime cost problem.

The tracking tools that make payroll actionable are the same ones that make your full P&L actionable. The Restaurant Budget Template lets you set monthly labor cost targets against projected revenue, so you're scheduling against a budget rather than scheduling and hoping the math works out. The Restaurant Income Statement Template gives you the monthly view to track whether labor is trending within target.

Payroll compliance protects you from penalties and back-pay claims. Payroll management — scheduling to a labor cost target, claiming the FICA tip credit, eliminating overtime errors — is how you preserve the margin that makes the operation viable. To see how labor savings flow through to cash on hand, the restaurant cash flow example walks through a full monthly and weekly statement.

Last updated: March 25, 2026

Frequently Asked Questions

Related Articles

Auto Repair Pricing Guide: How to Price Your Shop Profitably

How auto repair shop owners should price labor and parts — covering labor rate calculation, flat-rate hours, parts markup matrices, diagnostic fees, and the metrics that matter.

Cleaning Service Pricing Guide: How to Price Your Business Profitably

A practical guide to cleaning service pricing — covering hourly vs. flat rate vs. per square foot models, price benchmarks by service type, labor cost math, and the common mistakes that keep cleaning businesses from hitting their margin targets.

Construction Pricing Guide: How to Price Your Work Profitably

How contractors should price construction work — covering labor burden, overhead recovery, material markup, pricing methods, and the mistakes that quietly erode margin.

Electrical Pricing Guide: How to Price Your Work Profitably

How electricians and electrical contractors should price their work — covering hourly rates, flat-rate pricing, overhead recovery, material markup, and common mistakes that erode margin.

Hotel Sales Forecast: A Practical Example and Guide

How to build a hotel sales forecast — covering rooms, F&B, events revenue, key metrics like RevPAR and ADR, booking pace, and the rolling forecast structure that keeps you ahead.

Landscaping Pricing Guide: How to Price Your Work Profitably

A practical guide to landscaping pricing — covering hourly rates, per-square-foot benchmarks, overhead recovery, and the markup math that determines whether you're making money.