Real Estate Agent Budget Example: Commission-Based Finances

A real estate agent budget example covering GCI, broker splits, expense benchmarks, quarterly tax reserves, and seasonality for commission-based income.

Real estate is one of the few professions where you can earn six figures with no guaranteed salary — and also earn almost nothing your first two years. According to the 2025 NAR Member Profile, the median REALTOR gross income was $58,100 in 2024. Agents with zero to two years of experience had a median income of $8,100, with 62% earning under $10,000.

The volatility is the defining challenge of the business. A budget for a real estate agent isn't just an expense tracker — it's a cash flow survival plan built around income that arrives unpredictably, in large chunks, after 30–60 day closing timelines.

The Commission Math Before You Budget

Real estate budgets start with Gross Commission Income (GCI) — the total commission earned before any splits or deductions. This is the industry-standard top-line metric, equivalent to gross revenue.

How the math flows:

- Home sells for $400,000 at a 2.5% commission rate → $10,000 GCI

- Broker split taken (for a 70/30 agent: 30% to brokerage) → agent receives $7,000

- Agent's Net Commission Income (NCI): $7,000 — before expenses or taxes

The broker split matters enormously for budgeting. Common structures:

| Split Structure | Agent Keeps | Notes |

|---|---|---|

| New agent, traditional | 50–60% | Standard for first 1–2 years |

| Experienced agent | 70–80% | Earned through volume |

| Cap model (eXp, KW) | 80% until cap, then 100% | eXp: $16,000 annual cap; KW: 70/30 with $3,000/transaction cap |

| Flat-fee brokerage | 90–100% minus flat fee | Agent pays $500–$1,500/transaction flat |

| Desk fee model | 100% minus monthly fee | Agent pays $35–$75/month desk fee |

The cap model benefits high-volume agents: once the annual cap is hit, the agent keeps 100% for the rest of their anniversary year. An agent who hits the eXp cap at transaction eight keeps the full commission on transactions nine through twenty. Track GCI and broker splits automatically with Carvd.

For budgeting purposes, always use NCI — what arrives in your bank account — not GCI.

Real Estate Agent Expense Benchmarks

Here's how expenses typically break down as a percentage of GCI, based on IRS sole proprietor data and NAR member surveys:

| Expense Category | Benchmark Range (% of GCI) |

|---|---|

| Marketing and lead generation | 10–20% |

| Vehicle and transportation | 6–10% |

| Technology (CRM, MLS access, software) | 2–4% |

| MLS and association dues | 1–2% |

| E&O insurance | 0.5–1% |

| Health insurance (self-funded) | 5–10% |

| Professional development and licensing | 1–2% |

| Transaction costs (photography, signage, staging) | 2–5% |

| Office and supplies | 1–2% |

| Total business expenses | 30–55% |

| Tax reserve (set aside from NCI) | 25–35% of net income |

The vehicle line consistently appears as the single largest reported expense in NAR surveys. IRS data from real estate sole proprietor returns puts vehicle costs at roughly 8% of revenue on average — a figure that includes mileage reimbursement, car payments or lease costs, insurance, and fuel.

Marketing spend varies more than any other line. An experienced agent with a strong referral network might spend 10% of GCI on marketing. A new agent competing for leads in a digital market may spend 20% or more. Under-investing here is the fastest way to starve the pipeline.

Health insurance deserves a dedicated line. Agents are self-employed with no employer subsidy — $500–$700/month for individual coverage is common, adding $6,000–$8,400/year to fixed costs before generating a dollar of income. Run your numbers through the real estate profit margin calculator to see how much of your GCI actually reaches take-home after all expense layers.

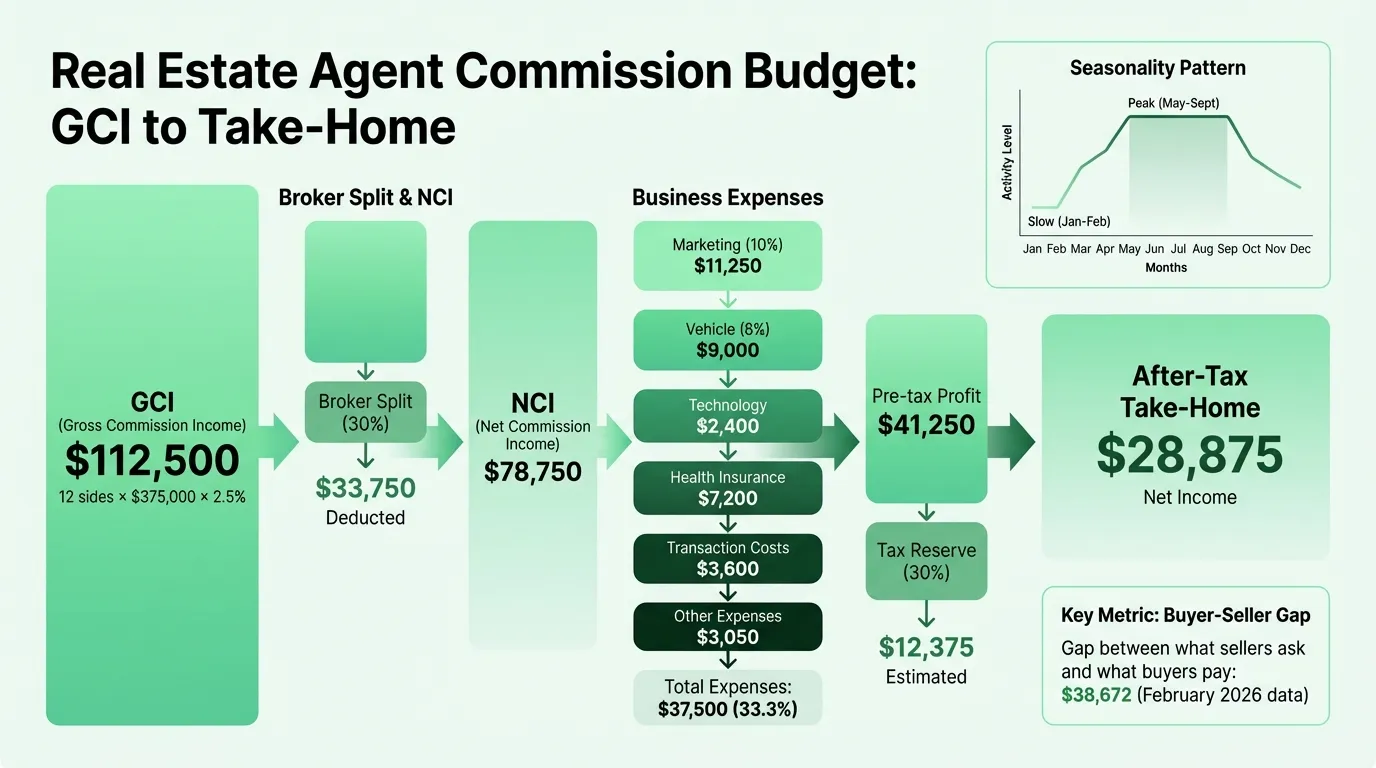

Budget Example: Mid-Level Agent

Here's a realistic annual budget for a licensed agent in year three or four, closing 12 transaction sides at an average sale price of $375,000.

Revenue

| Item | Amount |

|---|---|

| Transaction sides | 12 |

| Average sale price | $375,000 |

| Average commission rate | 2.5% |

| Gross Commission Income (GCI) | $112,500 |

| Broker split (30%) | -$33,750 |

| Net Commission Income (NCI) | $78,750 |

Business Expenses

| Category | Annual Amount | % of GCI |

|---|---|---|

| Marketing and lead generation | $11,250 | 10% |

| Vehicle and transportation | $9,000 | 8% |

| Technology (CRM, IDX, e-signature, MLS) | $2,400 | 2.1% |

| MLS and association dues | $1,500 | 1.3% |

| E&O insurance | $600 | 0.5% |

| Health insurance | $7,200 | 6.4% |

| Professional development and CE | $1,200 | 1.1% |

| Transaction costs (photography, signs, supplies) | $3,600 | 3.2% |

| Office and miscellaneous | $750 | 0.7% |

| Total Business Expenses | $37,500 | 33.3% |

Pre-tax business profit: $78,750 − $37,500 = $41,250

Tax Reserve

Self-employed agents owe self-employment tax (15.3% on net income, adjusted for the deductible half) plus federal and state income tax. A 30% set-aside on pre-tax profit covers most situations:

$41,250 × 30% = $12,375 tax reserve

After-tax take-home: $41,250 − $12,375 = $28,875

This is a realistic outcome for a productive year-three agent. It doesn't look impressive relative to the $112,500 GCI, which is why understanding the full stack matters before projecting income.

Apply the Real Estate Budget Template to adjust these inputs for your commission rate, split structure, and expense profile.

The Tax Reserve — Non-Negotiable

The single most common financial mistake real estate agents make is spending commission checks without reserving for taxes.

Every commission you receive arrives with zero tax withheld. The IRS treats you as a self-employed sole proprietor. You owe:

- Self-employment tax: 15.3% on net self-employment income (you deduct half of this as a business expense, but the cash still goes to the IRS)

- Federal income tax: Based on total taxable income

- State income tax: Varies by state

The practical rule: set aside 25–35% of each commission check the day it arrives, before anything else. Open a separate savings account labeled "Tax Reserve" and transfer to it automatically. This prevents the recurring scenario where agents end up owing $15,000–$25,000 at tax time with nothing available to pay it.

Pay quarterly estimated taxes — April 15, June 15, September 15, and January 15 — to avoid underpayment penalties. For a deeper look at how self-employment taxes interact with real estate deductions, the real estate accounting guide covers Schedule E, passive loss rules, and the $25,000 special allowance.

Need a ready-made budget template for your real estate?

Download a pre-built spreadsheet with industry-specific categories, formulas, and formatting.

Seasonality: Why Monthly Averages Don't Work

NAR data shows daily existing home sales run at roughly 16,500 during peak months (April through June) versus 11,400 during the slow season (December through February) — a swing of about 45% in transaction volume.

For agents, the income impact lands 30–60 days after the contract date, when the closing occurs. A May contract closes in June; a December contract (rare) closes in January. The result: most agents collect 60–70% of their annual income between June and September.

A monthly budget of GCI ÷ 12 is fiction. The budget needs a seasonality adjustment:

- Pull your last two years of closing data by month

- Calculate each month's closings as a percentage of your annual total

- Apply those percentages as monthly revenue weights in your projection

If you have no history to work from, the typical residential agent pattern:

- Strong: May, June, July, August, September

- Moderate: March, April, October

- Slow: January, February, November, December

Budget your slow months conservatively — as low as 30–40% of a strong month's income. The cash reserve funds the gap; it's not a sign something is wrong.

New Agent vs. Established Agent Budget Differences

The expense structure changes as a career develops:

New agent (years 1–2):

- Lead generation costs are higher (no referral network yet)

- No history to project transaction volume

- Often sharing costs with a sponsoring agent or team

- Marketing spend often 15–20% of limited GCI

- Median income $8,100 in first two years (NAR 2025) — many agents have a part-time income source until volume builds

Established agent (years 4+):

- Referral income becomes a meaningful line item

- Marketing ROI improves — less paid lead generation, more repeat and referral

- Vehicle costs grow with transaction volume

- Often considering team-building costs (buyer's agent splits, admin support)

New agents should budget conservatively: project transactions at the low end, assume marketing costs at the high end, and keep a minimum 6-month reserve before going full-time. The Real Estate Expense Tracker Template helps track actual spend against these benchmarks month by month.

Building a Reserve Before You Need One

A real estate income budget doesn't function like a salaried budget. The math:

- January 1: Bank account reflects last year's holiday slow period

- February: No closings scheduled; marketing costs continue

- March: Two contracts signed; closings expected in April and May

- April/May: Two commissions arrive

The two-month gap in February-March has zero income but full expenses. Without a reserve, agents enter each slow period with stress that affects performance.

The target: 3–6 months of total monthly expenses (including personal living costs) held as cash before reducing hours at another job or ramping marketing spend.

For the example agent above, monthly operating expenses run approximately $3,125. A 4-month reserve = $12,500. This number belongs in the budget as a non-negotiable savings target before the year's income gets spent.

If you want to track both business expenses and personal draw in one document, the Real Estate Budget Template separates business operating costs from owner distributions and cash reserves — the same structure used by productive independent agents managing commission income month to month.

One Metric to Track Monthly

Track your NCI-to-expense ratio — the percentage of Net Commission Income consumed by business expenses, excluding the tax reserve.

For the example above: $37,500 ÷ $78,750 = 47.6%. That leaves 52.4% for taxes and take-home.

If your expense ratio creeps above 60% of NCI, you're either underpricing (low commission rates or too many low-commission transactions), overspending on lead generation that isn't converting, or running unnecessary overhead for your transaction volume.

The fix is almost always the same: raise prices, cut underperforming lead sources, or both. Real estate is a simple business model. The budget makes the math visible so you can act on it before the problem compounds.

Last updated: March 23, 2026

Frequently Asked Questions

Related Articles

Coffee Shop Budget Example: Real Numbers and Benchmarks

A practical coffee shop budget example with real cost benchmarks — covering beverage COGS, labor, rent, equipment maintenance, and the line items most operators underestimate.

Church Budget Example: Categories, Percentages, and What to Include

A practical church budget example with real percentages for staff, facilities, missions, and programs — plus the line items most churches overlook.

Construction Budget Example: Line Items, Percentages, and What to Include

A practical construction budget example covering hard costs, soft costs, overhead allocation, and the line items most contractors underestimate.

Daycare Budget Example: Categories, Benchmarks, and What to Watch

A practical daycare budget example covering revenue sources, expense ratios, occupancy thresholds, and the line items that determine whether a center stays financially viable.

Event Planning Budget Example: Real Numbers for Your Business

A practical event planning budget example covering agency overhead, per-event costs, revenue models, and the benchmarks every planner needs to protect margins.

Hotel Budget Example: Departments, Benchmarks, and Real Numbers

A practical hotel budget example covering the USALI department structure, labor benchmarks, GOP targets, and the line items independent hoteliers most often miss.