Construction Budget Example: Line Items, Percentages, and What to Include

A practical construction budget example covering hard costs, soft costs, overhead allocation, and the line items most contractors underestimate.

Only 31% of construction projects come within 10% of their original budget, according to a KPMG Global Construction Survey. The other 69% overrun — and the causes are almost always predictable: missing line items, underestimated labor burden, unallocated overhead, and contingencies that were too thin for the project type.

A well-structured construction budget doesn't guarantee you'll hit the number. But it gives you a realistic target, a framework for tracking actuals, and a record of where estimates diverged from reality on the next job.

This is what a construction budget actually looks like.

Project Budget vs. Company Budget

Before getting into line items, it helps to distinguish between two types of construction budgets that serve different purposes.

A project budget covers a single job from start to finish. It includes all direct costs — labor, materials, equipment, subcontractors, permits, and project-specific insurance. This is the budget you build during estimating to set your contract price and track profitability job by job.

A company (annual) budget covers the entire business for a fiscal year. It includes revenue projections across all anticipated projects, company overhead (office staff, rent, marketing, software), and the profit target for the year. The company budget determines your overhead rate, which then flows back into every project estimate as a markup.

The link between the two is critical. If you're not allocating company overhead to individual projects, your jobs look more profitable than they are — and you'll underprice work until the company-level financials show the truth.

Hard Costs vs. Soft Costs

Every construction project budget breaks down into two top-level categories:

Hard costs are the direct physical costs of building. They typically make up 70-80% of total project cost:

- Labor (wages + labor burden)

- Materials (concrete, steel, lumber, finishes, fixtures, MEP materials)

- Equipment (owned and rented)

- Subcontractor fees (electrical, plumbing, HVAC, framing, etc.)

Soft costs are indirect costs associated with the project. They typically account for 20-30% of total project cost:

- Design, architecture, and engineering fees (typically 8-15% of total project cost)

- Permit fees and regulatory compliance

- Inspection fees

- Project bonds and insurance

- Legal and title costs

- Financing and loan interest

- Construction management fees (if using a third-party PM)

The most common budget mistake is treating the hard costs as the whole budget. A contractor who estimates $800,000 in hard costs and ignores $150,000 in soft costs is starting the project with a built-in shortfall.

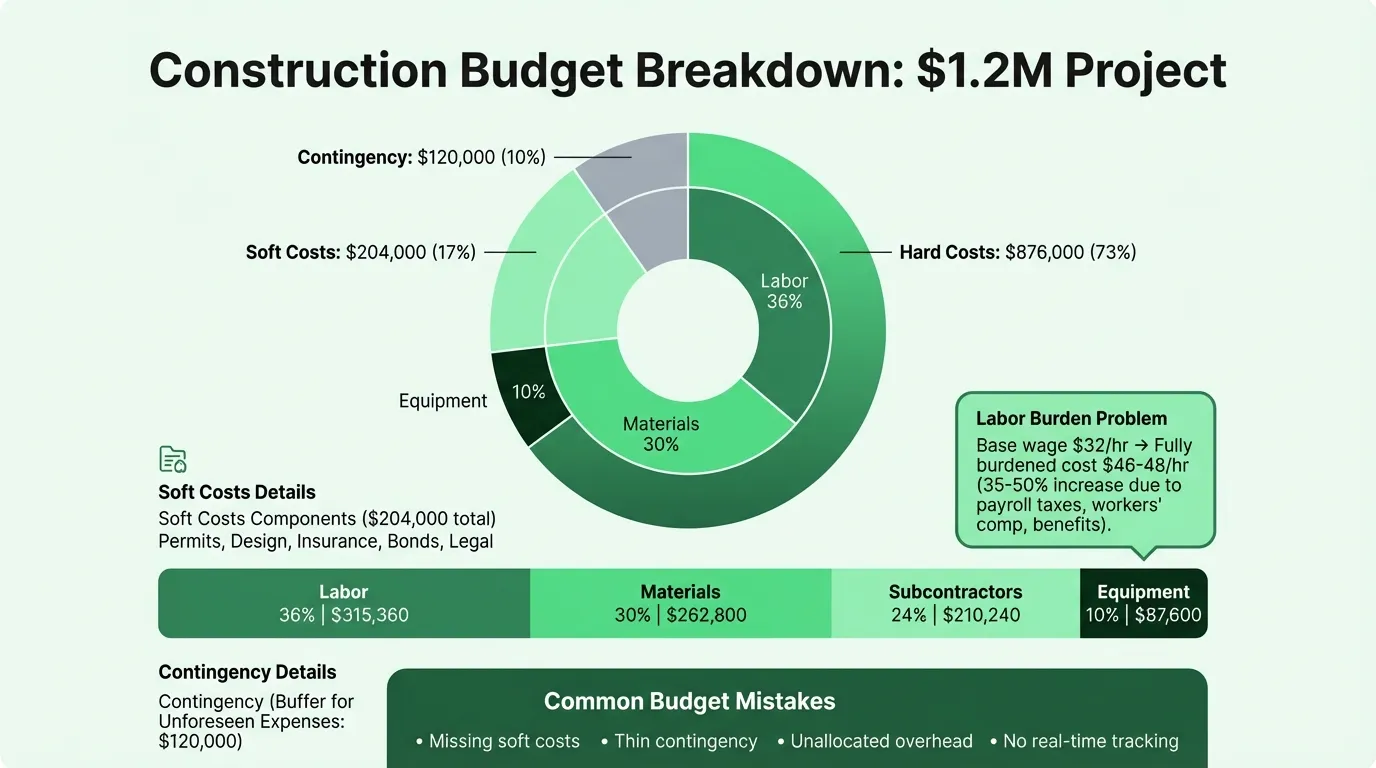

Example: A $1.2M Commercial Construction Budget

Here's a realistic example for a mid-size commercial tenant improvement project:

Summary

| Category | Amount | % of Total |

|---|---|---|

| Hard costs | $876,000 | 73% |

| Soft costs | $204,000 | 17% |

| Contingency (8%) | $120,000 | 10% |

| Total Project Budget | $1,200,000 |

Hard Costs Detail

| Line Item | Amount | % of Hard Costs |

|---|---|---|

| Labor | $315,000 | 36% |

| Materials | $262,800 | 30% |

| Subcontractors | $210,240 | 24% |

| Equipment (rental and owned) | $87,600 | 10% |

| Total Hard Costs | $875,640 |

Soft Costs Detail

| Line Item | Amount |

|---|---|

| Architecture and engineering | $72,000 |

| Permits and inspections | $36,000 |

| General liability insurance | $24,000 |

| Performance and payment bonds | $18,000 |

| Project management fee | $36,000 |

| Legal and contract fees | $18,000 |

| Total Soft Costs | $204,000 |

Contingency

Contingency is not a slush fund — it's a structured reserve for costs that can't be anticipated at the time of estimating. For a commercial tenant improvement with finalized drawings, 8-10% of hard costs is a reasonable starting point. Ground-up projects with less design certainty should run higher.

The Labor Burden Problem

Labor is typically the largest single line item in a construction budget — and the most consistently underestimated.

Most estimators start with base hourly wages and stop there. The actual cost of a worker includes:

- Payroll taxes (Social Security, Medicare, federal and state unemployment)

- Workers' compensation insurance

- General liability (labor component)

- Health benefits

- Paid leave, holidays, and vacation

- Employer retirement contributions (if applicable)

Combined, these burden costs can increase the true cost of labor by 35-50% above the base wage. A carpenter at $32/hour may actually cost $46-48/hour fully burdened. Estimating at $32 and not catching the delta until the job is halfway done is how profitable-looking projects end up with margin problems at closeout.

Calculate your labor burden rate annually and apply it consistently to every estimate. Most contractors use a single company-wide burden rate, though it varies by trade and state. Our construction pricing guide walks through the full billable rate calculation from burdened wages to overhead recovery.

Overhead Allocation

Company overhead must be recovered through project markups — but many contractors track overhead globally without allocating it down to individual jobs. This produces projects that look profitable in isolation while the company loses money overall.

The calculation is straightforward:

Annual company overhead (office rent, admin salaries, marketing, software, vehicles, non-project insurance) ÷ Annual projected revenue = Overhead rate

If your company carries $240,000 in annual overhead and projects $2,000,000 in revenue, your overhead rate is 12%. Every project estimate should include a 12% overhead markup on top of direct costs to ensure jobs contribute their share of fixed expenses.

Overhead rates by revenue band vary considerably. Companies under $1M in revenue often carry overhead rates of 25-35% because fixed costs don't scale down proportionally at smaller volumes. Companies over $10M typically run 8-14%.

Once overhead is marked up, profit is applied on top. The NAHB reported single-family residential builders averaging about 9% net profit margin in 2023. A common construction rule of thumb — 10% overhead + 10% profit — works as a starting benchmark but should be calibrated to your actual overhead rate. Use the construction profit margin calculator to see where each job lands after overhead is applied.

Need a ready-made budget template for your construction?

Download a pre-built spreadsheet with industry-specific categories, formulas, and formatting.

Change Orders: The Budget Killer

Change orders are the most common cause of construction budget overruns, and they're not always the owner's fault.

A change order is a formal modification to the original scope of work — design changes, material substitutions, unforeseen site conditions, or owner-requested additions. They can increase the contract value (adding revenue) or decrease it (dropping scope), but their secondary effects are what catches budgets off guard:

Schedule disruption. A change order that adds two weeks to a project doesn't just cost the direct cost of the changed work. It costs two additional weeks of site supervision, equipment rental, and temporary facilities.

Downstream effects. A late-project change to the electrical layout can require rework of drywall, ceiling tiles, and finished surfaces that were installed to a now-obsolete design.

Concurrent delay claims. Multiple overlapping change orders create schedule float disputes that can spiral into claims far exceeding the underlying change costs.

The budget control discipline is documentation — tracking every change order as it's issued, noting the schedule impact alongside the cost impact, and updating the project budget in real time rather than at closeout. For a broader look at how these costs roll up into company-level financials, see the construction income statement example.

Retainage and Cash Flow

Retainage is the 5-10% of each progress payment that owners withhold until substantial completion. It's standard practice, but its cash flow implications need to be part of the project financial plan from day one.

On a $1,200,000 project with 10% retainage, the contractor is doing $1,200,000 worth of work but receiving $1,080,000 during construction. The remaining $120,000 comes only after punchlist completion, final inspections, and lien waivers — often 30-90 days after the last crew leaves.

During that time, the contractor has already paid workers, materials suppliers, and subcontractors in full. The cash flow gap is structural. A project budget that doesn't account for retainage timing will look solvent on paper while the bank account is short.

Include a retainage line in your project budget to track what's held back, and model the cash flow timing separately. For a Construction Cash Flow Template that handles progress billing and retainage, you need a different tool than the project budget — the budget sets the cost target, cash flow tracks the timing.

Job Costing: The Budget in Real Time

A construction budget is only useful if you compare actuals against it during the project. That process is called job costing.

Job costing tracks actual costs incurred — labor hours worked and paid, materials invoiced, subcontractor billings — against the budgeted amounts for each cost code. When actuals exceed budget in any category, you know before the overrun compounds.

The most common failure mode: building a detailed project budget at the estimating stage and then never updating it during construction. By the time the job closes and you compare final costs to the original estimate, there's nothing left to do with the information except learn from it.

Effective job costing requires:

- Cost codes that match your estimate categories

- Timely entry of labor hours (weekly, not monthly)

- Invoice coding to specific cost codes at the time of approval

- Subcontractor billing tracking against the awarded subcontract amounts

- A weekly or bi-weekly budget-to-actual comparison at the project level

When any cost code runs more than 10% over budget, it warrants an explanation before you continue spending in that category.

Common Construction Budget Mistakes

Missing soft costs in the estimate. Permit fees, design revisions, inspection costs, and financing charges are easy to omit from initial estimates and hard to recover once the contract is signed. Build a soft cost checklist specific to your project type.

Contingency below the risk profile. A 3% contingency is appropriate for a project with locked-down drawings and straightforward site conditions. Applying that same rate to a renovation with unknown existing conditions guarantees an overrun. Match the contingency to the actual uncertainty in the scope.

Labor at base wages, not fully burdened. See the section above. This single error distorts every labor-heavy line item in the estimate.

Overhead not allocated. Projects can't recover overhead they're not charged for. Apply your overhead rate to every job, even if you don't see it on the invoice.

No real-time tracking. A budget compared to actuals at project close is a postmortem. A budget compared to actuals weekly is a management tool. The Construction Expense Tracker Template helps you log costs in real time against your budget categories.

Subcontractor costs at bid price, not contracted price. Bids change. If a sub quotes $45,000 but the contract comes in at $48,000 due to scope clarification, update the project budget. Running the wrong number through the whole project makes variance analysis meaningless.

Building Your Construction Budget

A Construction Budget Template gives you the hard cost, soft cost, overhead, and contingency structure already organized — with cost codes that match standard construction estimating categories and a budget-to-actual tracking column built in.

For the financial picture beyond the project level, the Construction Cash Flow Template handles progress billing schedules and retainage timing, while a construction income statement tracks company profitability across all jobs over a period.

The budget is the plan. Job costing tracks whether the plan is holding. Used together, they give you the information to finish profitable jobs and price future work accurately — rather than discovering margin problems at closeout when there's nothing left to do.

Last updated: March 23, 2026

Frequently Asked Questions

Related Articles

Coffee Shop Budget Example: Real Numbers and Benchmarks

A practical coffee shop budget example with real cost benchmarks — covering beverage COGS, labor, rent, equipment maintenance, and the line items most operators underestimate.

Church Budget Example: Categories, Percentages, and What to Include

A practical church budget example with real percentages for staff, facilities, missions, and programs — plus the line items most churches overlook.

Daycare Budget Example: Categories, Benchmarks, and What to Watch

A practical daycare budget example covering revenue sources, expense ratios, occupancy thresholds, and the line items that determine whether a center stays financially viable.

Event Planning Budget Example: Real Numbers for Your Business

A practical event planning budget example covering agency overhead, per-event costs, revenue models, and the benchmarks every planner needs to protect margins.

Hotel Budget Example: Departments, Benchmarks, and Real Numbers

A practical hotel budget example covering the USALI department structure, labor benchmarks, GOP targets, and the line items independent hoteliers most often miss.

What Is a Good Landscaping Budget? Benchmarks and Examples

A landscaping business budget breakdown covering labor, materials, equipment, overhead benchmarks, and the margin targets that separate profitable companies from struggling ones.