Hotel Cash Flow Example: Why Occupancy Doesn't Equal Cash

A real hotel cash flow example covering OTA commission timing, advance deposits, RevPAR gaps, and how to build a projection that prevents off-season surprises.

A hotel that runs 70% occupancy in August and 35% occupancy in January faces the same payroll run every two weeks. The debt service doesn't flex. Insurance renews on schedule. Property taxes come due regardless of RevPAR.

High RevPAR is not the same as healthy cash flow — and in hotels, the gap between the two is larger than in almost any other industry. Here's what that gap looks like in practice, and how to manage it.

A Real Hotel Cash Flow Example

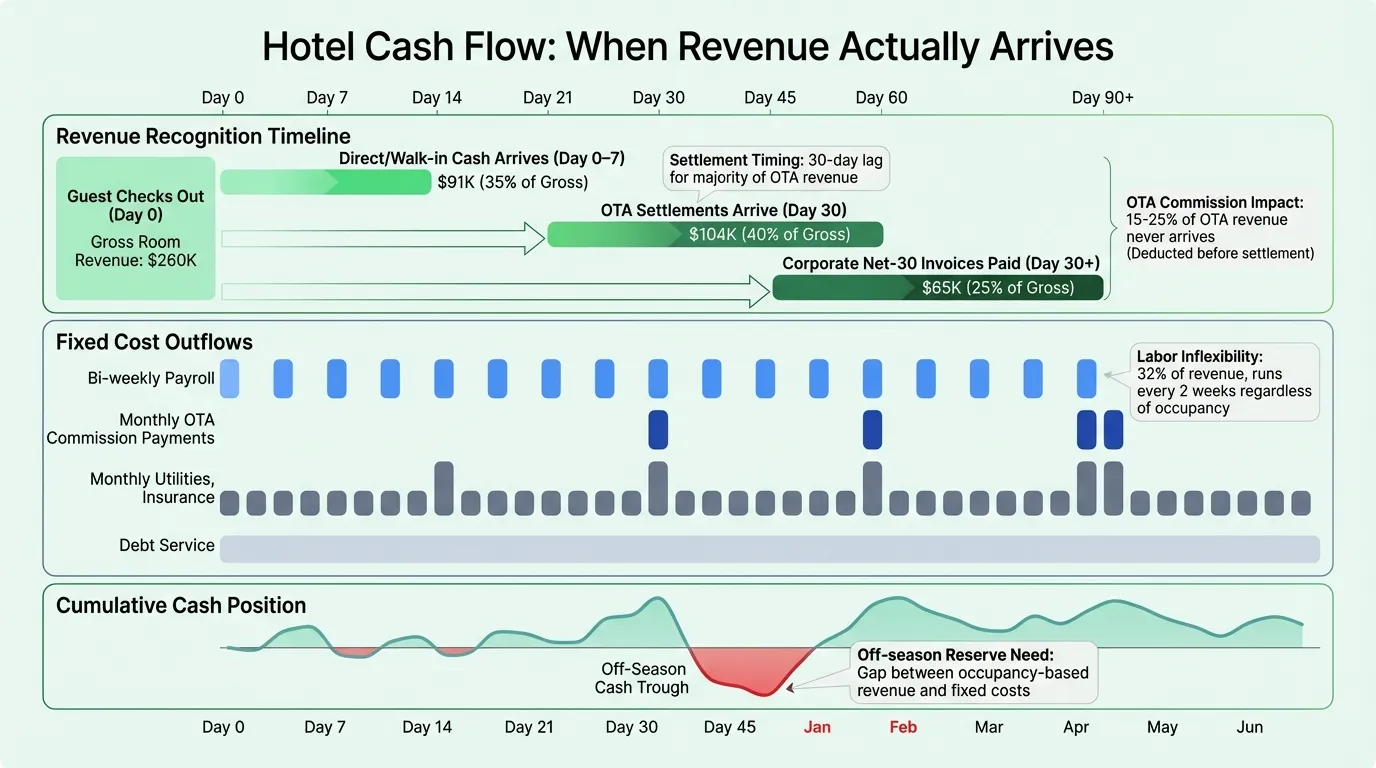

Take a 100-room midscale hotel with an ADR of $140 and average monthly occupancy of 62%. Gross room revenue comes to roughly $260,000 per month.

The problem is how that $260,000 actually reaches the bank account:

| Revenue Source | % of Bookings | Monthly Revenue | When Cash Arrives |

|---|---|---|---|

| OTA bookings (agency model) | 40% | $104,000 | 30 days after month end |

| Corporate accounts (net-30) | 25% | $65,000 | 30 days after checkout |

| Direct bookings / walk-in | 35% | $91,000 | At checkout |

Only $91,000 — about 35% of gross room revenue — lands in the account during the month it's earned. The remaining $169,000 arrives the following month. Meanwhile, payroll runs every two weeks without waiting for OTA settlements to clear.

This timing mismatch is the defining cash flow challenge for hotel operations.

What Makes Hotel Cash Flow Different

OTA Commissions and Settlement Timing

OTAs charge 15–25% commission per booking, with some platforms reaching 30% for premium placement. On $104,000 in OTA-booked revenue, a 20% commission rate means $20,800 that never arrives — and that amount is only settled monthly, not daily or weekly.

According to HotStats data, global RevPAR grew 19% from 2019 to recent years, but distribution costs per available room surged by 25% over the same period. In 2024, agency commissions in the Rooms Department grew 6.0% (CBRE). The practical result: revenue metrics improve while the cash cost of that revenue grows faster.

The settlement model matters. Under the merchant model (where OTAs like Expedia collect from guests upfront and remit the net to the hotel), the hotel may wait 7–30 days after checkout for funds — and receives only the net amount, not the gross. Under the agency model (where the hotel collects from the guest and then pays the OTA commission), the hotel carries the full commission as a liability until settlement. Either way, a meaningful share of room revenue is perpetually delayed or reduced.

Advance Deposits: Cash In, Revenue Out

Hotels routinely collect cash before earning it. Group bookings, events, and conference business typically require deposits of 25–50% of the estimated room block and F&B minimum. That cash arrives months before the event — but under ASC 606, it sits on the balance sheet as deferred revenue, not income, until the guests check out.

The cash flow statement benefits from this timing: advance deposits inflate operating cash inflows in the months they're collected. But it creates refund exposure. If a corporate group cancels, the hotel must return the deposit as a cash outflow that never appeared on the income statement as revenue. A refundable $40,000 deposit that needs to be returned in February — when occupancy is at 38% — is a severe cash event.

Non-refundable deposits are recognized as revenue only at the point of cancellation. This means the income shows up in the period the cancellation occurs, not when the cash was originally collected. See the hotel balance sheet example for how advance deposits sit as deferred revenue liabilities alongside guest and city ledger receivables.

Labor: Fixed Costs Against Variable Revenue

Labor is the largest single expense line for hotels — 32.4% of total revenue in 2023, up from 31.4% the prior year, per CBRE's Trends in the Hotel Industry survey. As a share of total operating expenses, labor represents 51.7%.

Unlike a retailer who can trim staffing sharply in slow periods, hotels maintain minimum service levels regardless of occupancy. A 100-room property with 38% occupancy in January still needs front desk coverage around the clock, housekeeping for the occupied rooms, maintenance staff, and management. Payroll runs every two weeks, hitting the bank account on a fixed schedule.

In 2024, labor cost per available room increased 11% year-over-year (STR). Combined with a 17.4% spike in insurance premiums and a 4%+ rise in property taxes (CBRE), the fixed cost floor for hotels rose substantially while RevPAR growth slowed to approximately 2.2% in Q1 2025 from 4.5% in January (TakeUp AI, mmcginvest). Use our hotel break-even calculator to find the occupancy level where revenue covers these fixed obligations.

The USALI Cash Flow Framework

Hotels use the Uniform System of Accounts for the Lodging Industry (USALI) — a standardized reporting format that structures the P&L differently from other industries. Understanding this structure is essential for reading hotel cash flow statements.

The P&L waterfall flows downward:

- Departmental Revenues — Rooms, Food & Beverage, Spa, Parking, Other

- Less Departmental Expenses — direct costs per revenue center

- = Departmental Profit

- Less Undistributed Expenses — G&A, Sales & Marketing, IT, Maintenance, Utilities

- = Gross Operating Profit (GOP)

- Less Management and Franchise Fees

- = Net Operating Income (NOI)

- Less Capital Expenditures and Reserves

- = Cash Flow from Operations

GOP margins averaged 35.4% across U.S. hotels in 2024 (STR/CoStar data via Cloudbeds), with net profit margins considerably thinner — approximately 4.86% in Q3 2024. The gap between a healthy GOP and thin net margins reflects debt service, capex reserves, and management/franchise fees that don't appear in operating expenses.

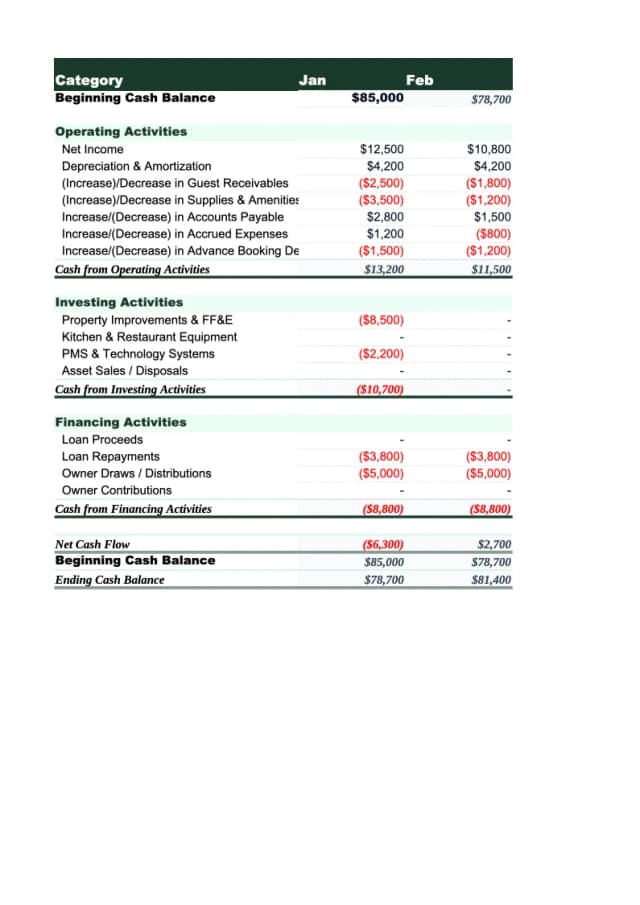

When a hotel cash flow statement starts with net income and adjusts back to cash, the key movements are:

- Adding back depreciation (non-cash charge that reduces net income)

- Changes in accounts receivable (OTA settlements outstanding, corporate billing)

- Changes in deferred revenue (advance deposits collected but not yet earned)

- Changes in accrued payroll (wages earned but not yet paid at period end)

Need a ready-made cash flow template for your hotel?

Download a pre-built spreadsheet with industry-specific categories, formulas, and formatting.

Building a 13-Week Hotel Cash Flow Projection

The 13-week rolling forecast is the right planning tool for hotel operations. It shows enough lead time to see an off-season cash crunch developing — and to take action before it becomes an emergency.

Weekly cash inflows to project:

- Room revenue by channel (direct, OTA, corporate, groups) — adjusted for settlement timing

- OTA remittances from the prior period (arriving on 30-day lag)

- Corporate account collections (net-30 from prior month billings)

- F&B and event revenue (settled at point of service or shortly after)

- Advance deposits received (flag separately as deferred revenue, not earned revenue)

Weekly cash outflows to project:

- Payroll (bi-weekly — the largest and most predictable outflow)

- OTA commission payments (monthly, on settlement date)

- Food and beverage purchasing (weekly, closely tied to occupancy)

- Utilities (monthly, with seasonal variation)

- Property taxes and insurance (quarterly, semi-annual, or annual — calendar these in advance)

- Debt service (fixed monthly amount — no flexibility)

- FF&E reserve contributions (contractually required by most lenders)

The projection calculates an ending cash balance for each week. When you see a future week where the balance falls below your minimum operating threshold, you have 3–6 weeks to act: draw on a line of credit, accelerate deposit collection for an upcoming group, defer a capital purchase, or arrange a temporary covenant waiver with your lender.

For hotels with significant seasonality — resort properties often see occupancy variation of 30–40 percentage points between peak and off-season — this projection needs to extend through at least one full shoulder or slow period. A September projection needs to account for what January looks like, not just October.

Managing Seasonal Cash Reserves

The most common hotel cash flow failure is spending peak-season cash on peak-season priorities — staff bonuses, deferred maintenance, pre-season renovations — without reserving enough to cover slow-season fixed costs.

The calculation is straightforward:

- Identify your monthly fixed cost floor (minimum payroll, debt service, insurance, property taxes, and utilities at minimum occupancy staffing)

- Project off-season revenue for each slow month

- Calculate the gap between projected revenue and fixed costs for each month

- Total those gaps — that's the reserve to accumulate before slow season arrives

Most hotel lenders require a seasonality reserve account precisely because they've seen this failure pattern. Hotels in covenant breach often end up in cash sweep arrangements where all revenue flows into lender-controlled accounts — making the liquidity situation worse, not better (Goodwin Law, 2024).

Building the reserve before you need it is cheaper and easier than negotiating a waiver after you've already spent the peak-season cash. A structured hotel budget with monthly distribution helps you size these reserves accurately against your seasonal revenue pattern.

Tools for Hotel Cash Flow Management

A purpose-built spreadsheet remains the most practical tool for independent hotels, boutique properties, and smaller chains. The key requirements for a hotel cash flow template:

- 13-week rolling view with hotel-specific inflow categories (by booking channel) and outflow categories (payroll, debt service, OTA commissions, F&B)

- Settlement timing adjustments so OTA and corporate collections are reflected when they actually arrive, not when the guest checks out

- Monthly view in a format that lenders and investors recognize (operating/investing/financing activities)

- Seasonality planning — the ability to model the full year to see when reserves are needed

The Hotel Cash Flow Template is built with these categories and timing adjustments already configured. If you're also tracking profitability by department, the Hotel Budget Template handles the USALI-format expense structure that hotel P&Ls follow.

What Lenders Want to See

Hotel financing — whether a working capital line, SBA loan, or commercial real estate mortgage — typically requires a 12-month historical cash flow statement and a 12-month forward projection. The format should mirror the USALI structure so the lender's underwriting team can map it against the benchmarks they use.

CBRE's Trends data and STR benchmarks are the reference points most hotel lenders use when reviewing GOP margins, labor ratios, and RevPAR performance. Presenting your cash flow in a format aligned with those benchmarks — rather than a generic business template — signals operational sophistication.

A hotel that can produce a clean, organized cash flow statement on request is easier to lend to, easier to refinance, and easier to sell. Generating it only when the bank asks is a missed opportunity to negotiate from strength. For acquisition-stage modeling, the hotel pro forma example shows how to project cash flow over a multi-year hold with DSCR and return metrics included.

The timing mismatch between RevPAR and actual bank deposits, between deposits collected and revenue earned, between peak occupancy and off-season fixed costs — these are structural features of hotel operations. Managing them requires visibility that occupancy reports and room revenue dashboards don't provide. That's what a cash flow projection is for.

Last updated: March 23, 2026

Frequently Asked Questions

Related Articles

Construction Cash Flow Example: How It Actually Works

A real-world construction cash flow example showing how retainage, draw schedules, and payment delays create cash gaps — and how to plan around them.

Restaurant Cash Flow Example: Real Numbers, Real Format

A complete restaurant cash flow example with real benchmark numbers — monthly statement, weekly view, and what each line actually means for your operation.

How to Manage Restaurant Cash Flow (Without Losing Sleep)

A practical guide to restaurant cash flow management — covering the timing mismatches, seasonal swings, and vendor payment cycles that catch operators off guard.