Hotel Balance Sheet Example: A Line-by-Line Breakdown

A complete hotel balance sheet example with real line items — FF&E, advance deposits, city ledger, and the ratios lenders use when reviewing hotel financials.

Hotels carry balance sheet line items you won't find in most other industries: FF&E reserves, advance deposits from guests who haven't arrived yet, and accounts receivable split between guests currently in-house and corporate clients billed after checkout. Understanding these items — and what's normal versus what signals a problem — matters whether you're managing a property, preparing for a hotel acquisition, or applying for refinancing.

This post walks through a complete hotel balance sheet example, line by line, with the benchmarks lenders use when reviewing hotel financials.

What Makes a Hotel Balance Sheet Different

The same three-section structure applies to every balance sheet — Assets = Liabilities + Equity — but hotels have several categories that are specific to the industry:

FF&E as a major asset. Furniture, Fixtures, and Equipment aren't a footnote in hotel accounting — they're often the second-largest asset category after the building itself. A single hotel room contains $15,000–$40,000 in FF&E depending on the property tier. Across a full-service hotel, FF&E can represent millions of dollars in capitalized assets.

Two types of accounts receivable. Most businesses have one accounts receivable balance. Hotels split it into a guest ledger (current in-house guests) and a city ledger (post-departure corporate and group accounts). The distinction matters: guest ledger balances are paid at checkout; city ledger balances require invoice collection and carry real credit risk.

Advance deposits as liabilities. When a guest books a room and pays a deposit — or when a group block is reserved with a prepayment — that cash sits on the balance sheet as a liability (deferred revenue) until the stay is delivered. Hotels often collect weeks or months before the service is rendered.

Real property as the dominant asset. For hotels that own their building, land and the structure itself typically account for 60–80% of total assets. This shapes every ratio on the balance sheet and explains why hotel leverage looks high compared to asset-light businesses. For a broader overview of how hotels handle these categories under USALI, see the hotel accounting guide.

Furniture, Fixtures, and Equipment (FF&E)

FF&E is the category that trips up people new to hotel accounting. It covers everything movable and non-structural in the property:

- Guestroom furniture: bed frames, headboards, desks, chairs, sofas, nightstands

- Fixtures: lamps, mirrors, curtain rods, bathroom hardware, artwork

- Equipment: televisions, in-room safes, coffee makers, mini-refrigerators, electronic door locks

FF&E is capitalized as a long-term asset (not expensed immediately) and depreciated over its useful life — typically 5 to 7 years under USALI (the Uniform System of Accounts for the Lodging Industry). The building structure depreciates over 39 years (commercial real estate); FF&E turns over much faster because it's subject to heavy daily use and guest-experience expectations.

Reserve for replacement. Because FF&E wears out on a predictable cycle, the industry standard is to set aside a reserve fund each year:

| Property Type | Reserve as % of Gross Revenue |

|---|---|

| Economy/limited service | 3.0% |

| Midscale and upscale | 3.5%–4.0% |

| Luxury/full service | 4.0%–5.0% |

| Technology/IT supplement | 1.0%–2.0% additional |

This reserve appears as a liability on the balance sheet — cash set aside for future capital expenditures. Lenders and investors review it closely when underwriting a hotel purchase or refinance. An under-reserved property carries deferred maintenance that will eventually show up in declining occupancy, lower ADR, or a capital call from the ownership group.

Guest Ledger vs. City Ledger

Hotels extend credit differently than most businesses, and the balance sheet reflects this.

Guest ledger is everything charged by guests currently staying at the property: room rate, tax, restaurant charges, spa, parking, minibar. These charges accumulate during the stay and are settled at checkout — typically via credit card. Collection risk is low because the card is authorized on arrival.

City ledger is accounts receivable for accounts billed after departure: corporate travel accounts, group master bills, travel agency commissions and direct bills, and occasionally government per-diem accounts. These clients receive invoices and pay on 30–60 day terms. Credit risk is real — the hotel has already delivered the service and is waiting to be paid.

For most hotels, city ledger balances are larger than guest ledger balances and require active A/R management. An aging city ledger — balances beyond 60 days — is a warning sign worth investigating. Use our hotel cash flow calculator to model how collection delays affect your liquidity position.

Complete Example: Full-Service Hotel

Here's a representative balance sheet for an 80-room upscale independent hotel doing approximately $3.2M in annual revenue:

Assets

Current Assets

| Line Item | Amount |

|---|---|

| Cash and cash equivalents | $95,000 |

| Accounts receivable — guest ledger | $28,000 |

| Accounts receivable — city ledger | $52,000 |

| Food and beverage inventory | $12,000 |

| Operating supplies (linen, uniforms) | $18,000 |

| Prepaid expenses | $22,000 |

| Total Current Assets | $227,000 |

Long-Term Assets

| Line Item | Amount |

|---|---|

| Land | $820,000 |

| Building | $3,400,000 |

| FF&E (furniture, fixtures, equipment) | $720,000 |

| Less: accumulated depreciation | ($1,310,000) |

| Capital improvements in progress | $95,000 |

| Total Long-Term Assets | $3,725,000 |

Intangible Assets

| Line Item | Amount |

|---|---|

| Franchise fee (net of amortization) | $82,000 |

| Total Intangible Assets | $82,000 |

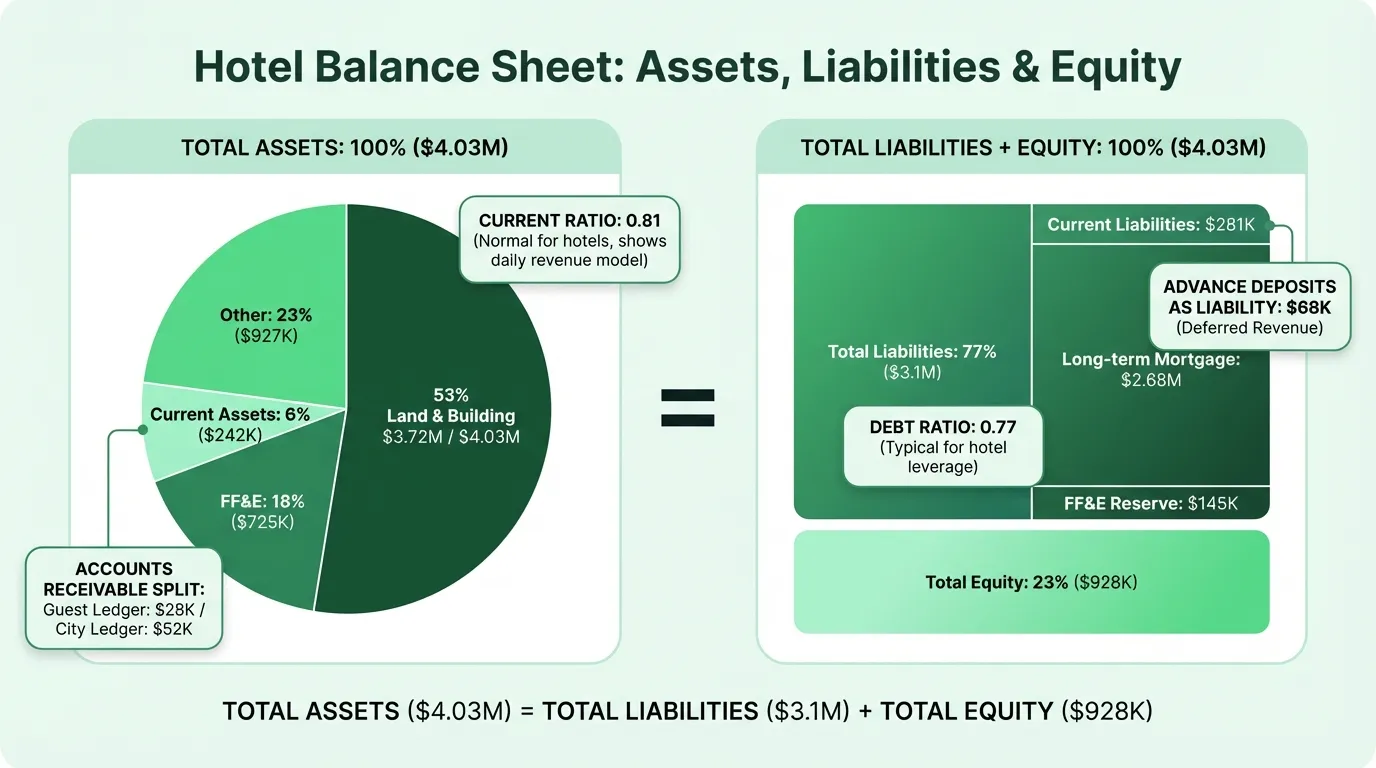

Total Assets: $4,034,000

Liabilities

Current Liabilities

| Line Item | Amount |

|---|---|

| Accounts payable | $55,000 |

| Accrued wages and benefits | $38,000 |

| Advance deposits (deferred revenue) | $68,000 |

| Sales and occupancy tax payable | $22,000 |

| Current portion of mortgage | $98,000 |

| Total Current Liabilities | $281,000 |

Long-Term Liabilities

| Line Item | Amount |

|---|---|

| Mortgage payable (long-term portion) | $2,680,000 |

| FF&E replacement reserve | $145,000 |

| Total Long-Term Liabilities | $2,825,000 |

Total Liabilities: $3,106,000

Equity

| Line Item | Amount |

|---|---|

| Owner's investment | $650,000 |

| Retained earnings | $278,000 |

| Total Equity | $928,000 |

Total Liabilities + Equity: $4,034,000

Need a ready-made balance sheet template for your hotel?

Download a pre-built spreadsheet with industry-specific categories, formulas, and formatting.

Reading the Key Ratios

Current Ratio

Current Ratio = Current Assets / Current Liabilities

In this example: $227,000 / $281,000 = 0.81

This is below 1.0, which typically signals a liquidity problem. For hotels, it's normal. According to ReadyRatios data on SEC-reporting U.S. hotel companies (SIC 7011), the industry average current ratio was 0.85 in 2024. Hotels generate daily revenue — rooms are sold and revenue flows in every night — so they don't need to hold large current asset balances to meet short-term obligations. The building and FF&E are the real assets; current assets are the working capital layer above that.

A current ratio below 0.50, or one declining rapidly alongside falling occupancy, is worth investigating. But 0.75–0.90 is the operating range for a healthy hotel.

Debt Ratio

Debt Ratio = Total Liabilities / Total Assets

In this example: $3,106,000 / $4,034,000 = 0.77

The hotel industry carries high leverage structurally — the property itself requires substantial mortgage financing. ReadyRatios reports a 2024 industry average debt ratio of 0.84 for publicly traded hotel companies, skewed upward by large REITs and full-ownership hotel operators. An independent hotel with strong equity investment in the 0.70–0.80 range is typical.

A debt ratio above 0.90 limits refinancing options and leaves little buffer against a revenue downturn. Many hotel lenders set a maximum debt service coverage ratio (DSCR) requirement — typically 1.25x — which indirectly constrains how much debt a hotel can carry relative to its operating income. The hotel pro forma example shows how DSCR is calculated within a full acquisition model.

Advance Deposits Coverage

Advance Deposits / Monthly Revenue

In this example: $68,000 / ($3,200,000 / 12) = 25.5% of monthly revenue

This isn't a standard ratio, but it's a useful operational check. A high advance deposit balance is a positive sign — it means future bookings are strong. A declining advance deposit balance heading into a busy season can signal booking weakness. Watch it month over month alongside occupancy trends.

Hotel-Specific Balance Sheet Items to Watch

Advance Deposits (Deferred Revenue)

When a guest books and pays in advance, the hotel records the cash immediately but can't recognize it as revenue until the stay occurs. This creates a current liability — you've collected money for a service you haven't yet delivered.

For hotels with group and conference business, advance deposits can represent several months of forward bookings. A property doing significant wedding, corporate, or conference business may carry 4–8 weeks of revenue in advance deposits. This is a strength, not a problem — but it needs to be tracked separately from operating cash.

Franchise Fees

Hotels operating under a brand flag (Marriott, Hilton, IHG, Hyatt, and their sub-brands) pay upfront franchise fees to join the system. These fees cover the right to use the brand name, reservation system, loyalty program, and marketing infrastructure.

The upfront fee is capitalized as an intangible asset and amortized over the expected period of benefit. For IRS purposes, franchise fees are amortized over 15 years under IRC Section 197. A hotel that paid $120,000 for a franchise fee 5 years ago will show approximately $80,000 remaining on the balance sheet — $8,000 per year amortization removes it gradually over time.

FF&E Net Book Value vs. Physical Condition

The net book value of FF&E on the balance sheet (cost minus accumulated depreciation) often diverges from the physical reality. A set of guestroom furniture may be fully depreciated to zero on the books — removed from the balance sheet — while still in reasonable condition. Conversely, newer FF&E may carry a high book value while showing physical wear that will require early replacement.

When reviewing a hotel balance sheet for acquisition or lending, the FF&E schedule matters more than the single line item. A property with heavily depreciated FF&E and an inadequate replacement reserve is carrying a capital expenditure obligation that doesn't show on the balance sheet. Factor these obligations into your annual planning with the Hotel Budget Template.

What Lenders Look At

Hotel financing — whether a first mortgage, refinance, or construction loan — involves a more detailed underwriting process than most commercial real estate because the property's value is inseparable from its operating performance. The balance sheet review focuses on:

| What They Check | What They Want to See |

|---|---|

| DSCR (Debt Service Coverage Ratio) | Above 1.25x; calculated from operating income |

| Loan-to-Value (LTV) | Typically 65%–75% for full-service hotels |

| Equity position | Owner equity at least 25%–35% of appraised value |

| Advance deposit balance | Positive trend; growing bookings |

| City ledger aging | No significant balances over 60 days |

| FF&E reserve adequacy | 3%–5% of revenue funded annually |

| Cash balance | Sufficient for 2–3 months of operating expenses |

| Franchise agreement term | Remaining term relative to loan maturity |

For CMBS loans (commercial mortgage-backed securities) and insurance company lending, the standards are tighter and more standardized. For community bank lending and SBA 504 loans, relationship history and local market knowledge carry more weight.

Building and Reviewing Your Hotel Balance Sheet

A monthly balance sheet is the baseline for managing a hotel's financial position. The annual balance sheet is required for tax filings, lender covenants, and ownership reporting — but monthly review lets you catch trends before they become problems: city ledger balances aging past 60 days, advance deposits declining before a slow season, equity eroding through distributions without retained earnings to offset them.

The Hotel Balance Sheet Template is structured for hotel operations — with FF&E tracking, the guest/city ledger split, advance deposits, and the replacement reserve already categorized.

For a complete financial picture, it pairs with the Hotel Income Statement Template (which tracks RevPAR, departmental margins, and GOPPAR) and the Hotel Cash Flow Template (which shows whether strong occupancy is actually generating cash available for debt service and capital reinvestment).

The balance sheet answers what the hotel owns and owes at a point in time. The income statement answers whether it's operating profitably. The cash flow statement answers whether profits are translating into cash available for reinvestment, debt paydown, and distributions. In hotel finance, all three tell different parts of the same story.

Last updated: March 24, 2026

Frequently Asked Questions

Related Articles

Church Accounting Best Practices: A Practical Guide

How church accounting works — fund accounting, restricted funds, internal controls, financial reports, and the tax rules that catch churches off guard.

Church Balance Sheet Example: A Line-by-Line Breakdown

A complete church balance sheet example with real line items, fund accounting explained, and the benchmarks church boards use to assess financial health.

Construction Accounting: A Practical Guide for Contractors

Construction accounting is different from standard accounting. This guide covers job costing, WIP schedules, retainage, revenue recognition methods, and common mistakes.

Construction Balance Sheet Example: A Line-by-Line Breakdown

A complete construction company balance sheet example with real line items, WIP accounting, retainage, overbilling, and what sureties and lenders look for.

Daycare Balance Sheet Example: Line by Line

A complete daycare balance sheet example with real line items — enrollment deposits, playground equipment, subsidy receivables, and what the numbers mean.

Food Truck Balance Sheet Example: A Line-by-Line Breakdown

A complete food truck balance sheet example with real line items, truck depreciation rules, and what makes a food truck's financials different from a restaurant.