Healthcare Pro Forma Example: What to Include and How to Build One

A practical healthcare pro forma example — covering revenue projections, payer mix, expense benchmarks, and a worked model for a new medical practice or service line.

Building a financial model for a medical practice requires a different structure than most businesses. Revenue isn't a price times volume. What you bill, what you're contractually adjusted, and what you actually collect are three different numbers — and they diverge significantly based on who your patients are and what insurance they carry.

A healthcare pro forma works through that complexity in a structured way. Whether you're opening a new practice, hiring a physician, adding a service line, or applying for an SBA loan, the pro forma answers the same core question: given realistic assumptions about volume, payer mix, and costs, does this generate sustainable revenue?

This post covers what a healthcare pro forma includes, the benchmarks that inform the inputs, and a worked example for a primary care practice startup.

When You Need a Healthcare Pro Forma

Opening a new practice. Every practice startup loan requires one. Banks need to see that projected collections, after the ramp-up period, will cover debt service, operating expenses, and physician compensation. The pro forma also shows how much working capital you need to bridge the gap between opening day and the point where collections stabilize.

Hiring an additional physician or advanced practice provider. The question isn't just compensation — it's whether the new provider's volume will eventually exceed their fully-loaded cost (salary, benefits, malpractice, and overhead allocation). Year 1 typically won't break even. The pro forma shows which year does, and whether you can fund the gap.

Adding a service line or ancillary service. In-house labs, imaging, or procedures carry equipment, staffing, and space costs that precede revenue. Before buying equipment, you need to confirm that local reimbursement rates — not the vendor's national projections — support the investment. A pro forma built on your actual payer mix rather than vendor presentations is what makes that decision reliable.

Practice acquisition. Acquisition financing requires projecting post-transition revenue (accounting for patient attrition when a physician changes ownership) against debt service on the acquisition loan. Practices typically see 10–25% attrition in the 12 months following a physician departure or ownership change.

Applying for a bank or SBA loan. Lenders require a 3–5 year pro forma as part of the loan package. They're primarily looking at whether projected net collections support the debt service coverage ratio their program requires.

What Makes Healthcare Pro Formas Different

Healthcare adds layers that most business pro formas don't have:

Payer mix complexity. A retail business has a price. A medical practice has dozens — one rate per service per payer. Commercial insurance pays approximately 196% of Medicare rates for the same service (Milliman, 2025). Medicaid payments were nearly 30% below Medicare rates in 2019 and have not closed that gap significantly. A practice with 70% Medicare and Medicaid exposure will have fundamentally different unit economics than one with 70% commercial insurance — even at identical patient volume.

Gross charges vs. net collections. You bill the gross charge. Payers have negotiated contractual adjustments that reduce it. After adjustments, some claims are denied outright. What you actually collect — net patient service revenue — might be 55–85% of what you billed. A pro forma built on gross charges without a realistic collection rate is not a financial model; it's an optimistic number. For a detailed look at how these adjustments flow through a real P&L, see our healthcare income statement example.

Revenue cycle timing. Unlike a retail transaction, collections in healthcare follow claim submission by weeks. Medicare typically pays within 14 days of a clean claim; some commercial payers pay at 45 days. A new practice doesn't start collecting until 30–90 days after it starts seeing patients. That gap requires explicit working capital modeling.

Reimbursement rate volatility. The Medicare conversion factor was $33.29/RVU in 2024 and dropped to $32.35/RVU in 2025 — a 2.83% reduction. Payer policies, covered services, and coding requirements change annually. A multi-year pro forma should include sensitivity analysis on reimbursement rates, not just lock in today's rates as permanent.

What a Healthcare Pro Forma Includes

Revenue Projections

Revenue projections start with volume and work down to net collections:

Volume assumptions:

- Clinic days per year (240 is the standard baseline)

- Patients per day (or visits per half-day session)

- Total annual visits

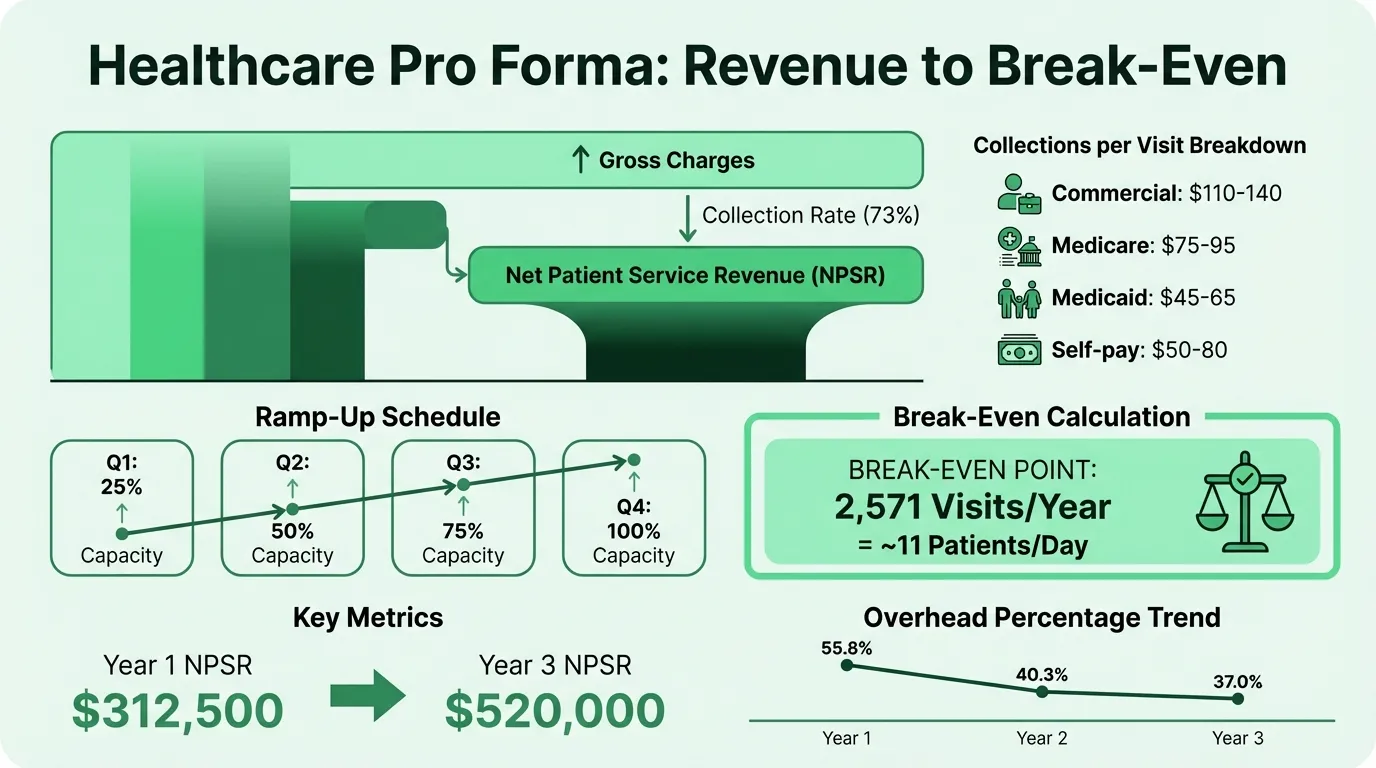

A common MGMA example: 9 half-day sessions per week × 8 patients per half-day × 48 weeks = 3,456 annual visits at full capacity. Year 1 won't reach full capacity — apply a ramp-up schedule.

Ramp-up schedule:

| Quarter | % of Full Capacity |

|---|---|

| Q1 | 25% |

| Q2 | 50% |

| Q3 | 75% |

| Q4 | 100% |

This schedule is standard for new physicians and new practices. Established practices adding a service line may ramp faster if they can redirect existing patients.

Collections per visit:

This is where payer mix matters most. Estimate the average collection per visit by blending your expected payer distribution:

| Payer Type | Typical Payment per Primary Care Visit |

|---|---|

| Commercial insurance | $110–$140 |

| Medicare | $75–$95 |

| Medicaid | $45–$65 |

| Self-pay (collected) | $50–$80 |

A 50/30/15/5 commercial/Medicare/Medicaid/self-pay split produces a very different weighted average than 30/40/25/5.

Net patient service revenue (NPSR): NPSR = Gross charges × Collection rate. A 75% collection rate on $800,000 in gross charges yields $600,000 in NPSR. The pro forma projects NPSR — not gross charges — as the top-line revenue figure.

Expenses

Per MGMA data, total overhead for a typical medical practice runs 60–70% of revenue. Here's how that breaks down:

| Expense Category | Typical Range | % of Revenue |

|---|---|---|

| Staff salaries and benefits | Largest variable | ~25% |

| Rent and occupancy | $2,000–$8,000/month | ~4% |

| Medical supplies and materials | — | ~4% |

| Malpractice insurance | $7,500–$50,000+/year | ~2% |

| EHR / technology | $300–$800/month (cloud) | ~2–3% |

| Billing services (outsourced) | 3–10% of collections | ~3–5% |

| Marketing | — | ~1–2% |

| Legal and professional | — | ~1% |

| Depreciation | — | ~1% |

| Total overhead | — | 60–70% |

Physician compensation sits above this overhead line — it's typically a separate line targeting 40–50% of gross collections for a physician-owned or physician-employed model.

Important: model startup costs separately. One-time costs for a new practice — equipment, tenant improvements ($100–$120/sq ft is a realistic range), licensing, EHR implementation, and initial working capital — don't belong in the ongoing operating expense model. They appear in the startup cost summary and working capital requirement, not in the recurring expense projection.

Break-Even Analysis

The break-even calculation tells you how many patients per day (or per year) the practice must see to cover fixed and variable costs.

Using a simple model:

- Average collected per visit: $150 (primary care)

- Variable cost per visit (supplies, direct materials): $10

- Contribution margin per visit: $140

- Fixed annual costs (staff, rent, technology, insurance): $360,000

Break-even visits = Fixed costs ÷ Contribution margin per visit $360,000 ÷ $140 = 2,571 visits/year = approximately 11 patients per day (on 240 clinic days)

Run your own scenarios with the healthcare break-even calculator.

For a 3-physician primary care practice with $900,000 in fixed overhead, the break-even is approximately 6,429 visits — about 9 patients per day per physician. That's well below the capacity of a fully operational physician, which means the model pencils out once the ramp-up period ends.

Hospital Support / Funding Gap (Where Applicable)

For hospital-employed physician models or joint ventures, the pro forma typically quantifies the annual subsidy:

Annual support = Projected expenses − Projected collections (year 1–3)

This subsidy is expected to decline as patient volume builds. A hospital-employed pro forma typically models the cumulative support through year 3 and the year in which the physician becomes net revenue-positive to the system.

Need a ready-made pro forma template for your healthcare?

Download a pre-built spreadsheet with industry-specific categories, formulas, and formatting.

Worked Example: Solo Primary Care Practice Startup

This is a simplified model for a solo family medicine physician opening a new practice in a suburban market.

Assumptions

- Opening month: Month 1

- Clinic days: 240/year at full capacity

- Full-capacity visits: 4,000/year (average 16–17 per day)

- Average collected per visit: $125 (payer mix: 40% commercial, 35% Medicare, 20% Medicaid, 5% self-pay)

- Collection rate: 73% of gross charges

- Physician compensation target: $220,000 (employed model equivalent)

Revenue Projection (Years 1–3)

| Year 1 | Year 2 | Year 3 | |

|---|---|---|---|

| Capacity utilization | 63% avg | 90% | 100% |

| Annual visits | 2,500 | 3,600 | 4,000 |

| Avg collected/visit | $125 | $128 | $130 |

| Net patient service revenue | $312,500 | $460,800 | $520,000 |

Year 1 applies the ramp-up schedule (Q1 at 25%, Q2 at 50%, Q3 at 75%, Q4 at 100%), averaging to roughly 63% utilization for the year.

Expense Projection (Years 1–3)

| Expense | Year 1 | Year 2 | Year 3 |

|---|---|---|---|

| Staff salaries + benefits (1.5 FTE) | $72,000 | $75,000 | $78,000 |

| Rent ($3,200/month) | $38,400 | $38,400 | $38,400 |

| Medical supplies (4% of NPSR) | $12,500 | $18,432 | $20,800 |

| Malpractice insurance | $12,000 | $12,000 | $12,000 |

| EHR + technology ($500/month) | $6,000 | $6,000 | $6,000 |

| Billing services (5% of collections) | $15,625 | $23,040 | $26,000 |

| Marketing | $8,000 | $5,000 | $4,000 |

| Misc (legal, accounting, admin) | $10,000 | $8,000 | $7,000 |

| Total operating expenses | $174,525 | $185,872 | $192,200 |

| Overhead ratio | 55.8% | 40.3% | 37.0% |

| Operating income before physician comp | $137,975 | $274,928 | $327,800 |

| Physician compensation | $220,000 | $220,000 | $220,000 |

| Net income (loss) | ($82,025) | $54,928 | $107,800 |

Year 1 runs a loss — this is normal and expected for a practice startup. The working capital requirement to fund the year-1 deficit, plus startup costs, is the figure a lender or the physician needs to finance.

Startup Cost Summary

| Item | Estimated Cost |

|---|---|

| Leasehold improvements | $45,000 |

| Medical equipment and furnishings | $35,000 |

| EHR implementation and training | $8,000 |

| Licensing, credentialing, legal | $5,000 |

| Initial marketing and website | $6,000 |

| Working capital reserve (6 months) | $75,000 |

| Total startup requirement | $174,000 |

The working capital reserve covers the gap between opening and the point where monthly collections exceed monthly expenses — typically around months 8–12 for a primary care practice.

Key Benchmarks to Stress-Test Your Model

Days in Accounts Receivable. A well-run practice collects most of what it bills within 35 days. A/R over 45 days suggests billing or collection problems. Over 50 days is a red flag. For a startup pro forma, build in a 45-day assumption for year 1 (collections lagging as credentialing is completed and billing workflows stabilize), tightening to 35–40 days in year 2+.

No single payer over 50%. Per practice finance consultants, concentration risk is significant when any single payer exceeds 50% of revenue. That payer can renegotiate rates or change coverage policy and materially alter the practice's economics. Your pro forma should show a diversified payer mix assumption. To see how payer mix affects what the practice owns and owes, review the healthcare balance sheet example — particularly the net AR presentation.

Denial rates. According to an Experian Health survey, 73% of healthcare respondents report claim denials are increasing. Practices with ineffective revenue cycle management lose meaningful revenue to preventable denials. Build a denial and write-off assumption into the collections rate — a 73% collection rate is more defensible than 85% for a startup that doesn't yet have an optimized billing workflow.

Physician productivity benchmarks. MGMA reports median net patient service revenue per physician FTE at approximately $767,682 for the most recent period. A solo primary care physician generating $500,000 in collections is below median; $600,000–$700,000 is a realistic target by year 3 of a growing practice.

Building Two Scenarios

Every healthcare pro forma should present at least two scenarios:

Conservative scenario: Lower patient volume (15–20% below base case), lower collection rate (5–10 points below base case), higher malpractice insurance (if in a high-risk geography or specialty), and a longer ramp-up period.

Realistic scenario: Base-case assumptions — the numbers you genuinely expect if execution goes reasonably well.

Lenders run their own stress tests. Walking in with a model that only shows the upside signals either optimism or inexperience. A conservative scenario that still covers debt service — or that quantifies exactly how much additional working capital would be needed if collections come in at the low end — is more credible than a single set of projections. Use the healthcare cash flow calculator to stress-test collection timing under both scenarios.

How the Pro Forma Fits the Broader Financial Picture

The pro forma is the planning document. Once the practice is operating, ongoing financial management shifts to tracking actual performance against the projection.

The Healthcare Pro Forma Template is built for lender packages and practice planning decisions — with payer mix inputs, a ramp-up schedule, revenue waterfall from gross charges to NPSR, and a break-even calculation. For ongoing financial reporting once the practice is running, the income statement and balance sheet take over as the primary documents.

A healthcare pro forma built on realistic payer mix assumptions, a credible collection rate, and full-cost expenses won't always show a profitable year 1 — but it will accurately show what year 1 actually costs and whether the practice reaches a sustainable run rate before the working capital runs out. Turn your pro forma into a polished deck — Deckary.

Last updated: March 24, 2026

Frequently Asked Questions

Related Articles

Coffee Shop Income Statement Example: Revenue, Costs, and Margins

A coffee shop income statement example with beverage cost benchmarks, labor targets, prime cost rules, and a worked P&L for an independent café doing $480K/year.

Daycare Income Statement Example: Revenue, Costs, and Margins

A daycare income statement example with tuition revenue, CACFP reimbursements, staff cost benchmarks, and a worked P&L for a 50-child childcare center.

Food Truck Income Statement Example: Line Items and Benchmarks

A food truck income statement example with food cost benchmarks, unique line items like commissary and pitch fees, and a worked P&L for a single-truck operation.

Healthcare Income Statement Example: Revenue, Expenses, and Margins

A healthcare income statement example covering net patient revenue, contractual adjustments, expense benchmarks, and operating margin targets for providers.

Hotel Pro Forma Example: What to Include and How to Build One

A practical hotel pro forma example — covering RevPAR, GOP, undistributed expenses, FF&E reserves, and a worked model for acquisition or development underwriting.

Manufacturing Income Statement Example: Line Items and Benchmarks

A manufacturing income statement example with COGM schedule, gross margin benchmarks by subsector, and a worked P&L for a precision parts manufacturer.