Law Firm Accounting: A Practical Guide for Managing Partners

How law firm accounting works — covering trust accounts, cash vs. accrual, realization rates, and the reports that actually tell you how the firm is performing.

Law firm accounting follows the same double-entry principles as any other business, but it has three layers of complexity that don't exist elsewhere: mandatory trust accounting for client funds, billable time as the primary unit of production, and a revenue cycle that converts slowly from hours worked into cash collected.

Get these three things right and your financial reports accurately reflect how the firm is performing. Miss any one of them and you're managing the business with incomplete — or potentially misleading — information.

Cash vs. Accrual: The Decision That Shapes Everything

Most law firms start on cash basis and stay there. Revenue is recorded when fees are collected; expenses are recorded when paid. The books reflect actual cash, which makes draw planning straightforward and tax reporting simple.

The IRS permits cash basis accounting for firms with average annual gross receipts under $25 million, which covers the vast majority of small and mid-size firms. If you're under that threshold, cash basis is almost always the right default.

Accrual accounting records revenue when earned (work performed) and expenses when incurred. The advantage is that the income statement more accurately reflects economic activity in a given period. The disadvantage is that you can show strong accrual revenue while the bank account is thin — because collection hasn't caught up with billing. Accrual is required by GAAP and typically expected by lenders and investors evaluating firm acquisitions.

The practical middle ground: many mid-size firms keep cash basis books for tax purposes and run parallel accrual-style management reports (including work-in-progress and accounts receivable) to give partners a complete operational view. This is more work, but it keeps tax compliance simple while providing the management visibility that cash basis alone doesn't offer.

Whichever method you use, the trust account operates under its own rules that override both — more on that below.

Trust Accounting: The Non-Negotiable

Trust accounting is what separates law firm accounting from every other professional services context. Client funds — retainers, settlement proceeds, filing fees held in advance — legally belong to clients until earned or disbursed. They cannot be commingled with firm operating funds, and the rules governing how they're handled are set by state bar authorities, not by accounting standards.

The IOLTA Account

Client funds that are too small or held too briefly to earn meaningful interest for the individual client go into a pooled IOLTA (Interest on Lawyers Trust Accounts) account. The bank pays interest on the aggregate balance to a state bar foundation for legal aid funding. Attorneys receive no interest on IOLTA funds — they are not permitted to.

For larger retainers or settlement proceeds that can earn meaningful interest for the client, a separate interest-bearing trust account is required, with interest payable to the client directly.

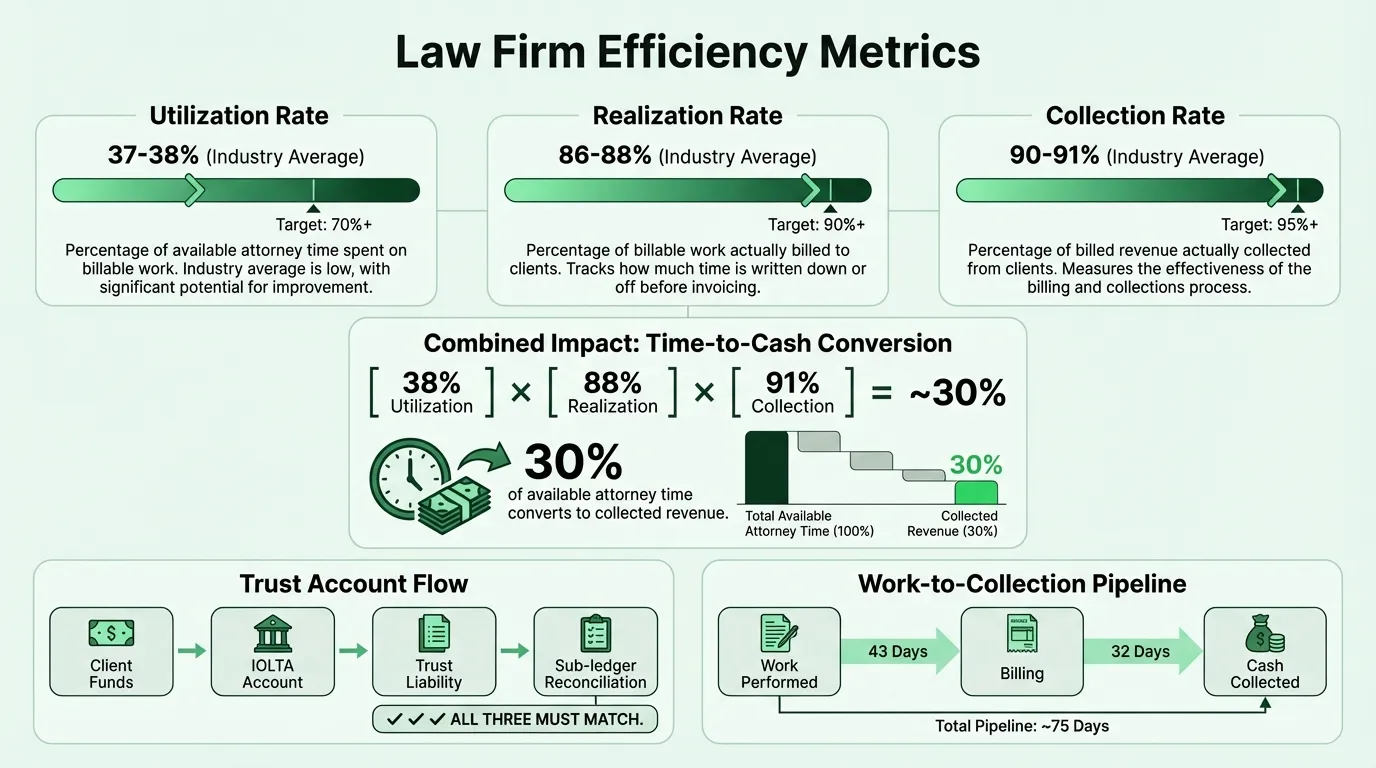

Every client whose funds are in trust requires its own sub-ledger tracking every deposit and withdrawal. The aggregate of all client sub-ledgers must match the trust bank balance at all times.

The Three-Way Reconciliation

Most state bars require monthly reconciliation of three records that must match:

- Trust bank statement balance — what the bank shows

- Firm trust book balance — what your accounting records show

- Sum of individual client sub-ledgers — the aggregate of all client-level records

All three must agree. A discrepancy between any two indicates an error — a missed transaction, a posting error, or something more serious. Monthly reconciliation catches these when they're still findable. Quarterly or annual reconciliation lets errors compound in ways that can take months to untangle.

What Counts as Commingling

The commingling prohibition is stricter than most attorneys expect. Common violations:

- Depositing a client retainer directly into the operating account, even temporarily before transferring to trust

- Using trust funds to cover operating expenses when the operating account is short

- Holding earned fees in trust after they've been earned (they must be transferred to operating promptly)

- Paying firm expenses from a trust account that holds only one client's settlement proceeds

Trust account violations account for a disproportionate share of state bar disciplinary complaints. The consequences scale from mandatory training for isolated errors caught early, up to suspension or disbarment for patterns of misappropriation. For a complete worked example showing how trust accounts appear on both sides of the ledger, see the law firm balance sheet example.

The Three Efficiency Metrics That Drive Profitability

Law firm profitability depends on three ratios working in sequence. According to Clio's Legal Trends data, most firms have significant room for improvement in all three.

Utilization rate — billable hours worked divided by total available hours. The industry average is around 37–38% of available time. That means the average attorney captures roughly 2.9–3.0 billable hours in an eight-hour workday. A utilization rate of 70%+ is considered the threshold for effective firms; top performers exceed 75%.

Realization rate — what is actually billed divided by what could have been billed (worked hours at standard rates). Industry average is 86–88%. Gaps between worked hours and billed hours come from write-downs, courtesy discounts, and unbilled time that falls through the cracks.

Collection rate — what is actually collected divided by what was billed. Industry average is 90–91%. A 10% collection gap on $2 million in billings is $200,000 left on the table annually.

Combined: at industry averages (38% utilization × 88% realization × 91% collection), roughly 30% of available attorney time converts to collected revenue. Improving any one of the three — even incrementally — has a significant impact on realized income. Check your own firm's numbers with the law firm profit margin calculator.

| Metric | Industry Average | What It Measures |

|---|---|---|

| Utilization rate | 37–38% | Billable hours worked vs. available |

| Realization rate | 86–88% | Billed vs. worked at standard rates |

| Collection rate | 90–91% | Collected vs. billed |

Track these monthly, not annually. A realization rate trending downward over three months — even within the "normal" range — is a signal worth investigating before it becomes a structural problem.

Chart of Accounts for Law Firms

A law firm's chart of accounts has the standard five categories, but the sub-accounts reflect legal practice realities.

Assets — Operating cash, trust bank account (IOLTA), accounts receivable (accrual basis only), work-in-progress (unbilled time, accrual basis), advanced client costs, prepaid expenses, fixed assets.

Liabilities — Client trust liability (equal to the trust bank balance at all times), unearned retainer liability (flat fees received but not yet earned), accounts payable, accrued payroll, lease liability.

Equity — Partner capital accounts, retained earnings (for incorporated entities).

Revenue — Separate accounts by revenue type matter: hourly fees, flat fees, contingency income, and disbursement reimbursements are structurally different and should be tracked separately. If your revenue accounts pool all of these together, you can't identify which fee structures are driving margin and which aren't.

Expenses — Attorney compensation, staff payroll, malpractice insurance, bar dues and CLE, legal research subscriptions, rent, marketing, court costs (non-reimbursable). For benchmark ranges on each of these categories, see our law firm budget example.

One critical distinction on client costs: filing fees, deposition costs, and expert witness fees paid on clients' behalf that are expected to be reimbursed are not firm expenses. They're an asset — advanced client costs — until they're either reimbursed or written off. Expensing them incorrectly understates profitability and misstates the balance sheet.

Need a ready-made p&l template for your law firm?

Download a pre-built spreadsheet with industry-specific categories, formulas, and formatting.

The Financial Reports You Actually Need

Standard financial statements — P&L, balance sheet, cash flow — are necessary but not sufficient for managing a law firm. You need four additional reports.

Accounts receivable aging. Billed but uncollected fees by aging bucket (current, 30, 60, 90, 90+ days). A healthy AR profile has minimal balance over 90 days. On a cash-basis balance sheet, AR doesn't appear at all — so an aging report is the only way to see what's outstanding. For a firm doing $2M in revenue, carrying 90-120 days of uncollected AR is the equivalent of having $500,000–$700,000 sitting idle.

Work-in-progress (WIP) report. Unbilled time by client and matter. WIP represents future billing capacity — work done but not yet invoiced. A growing WIP balance can mean partners are working but not billing, or that billing cycles have slipped. Either is a problem. The median time from work performed to billing is around 43 days; firms with consistent billing practices run this significantly lower.

Trust account reconciliation. Required by most state bars, not optional. Reviewed by partners monthly, not delegated entirely to staff.

Realization and collection rate report. By timekeeper, by practice group, by matter. Firm-level averages hide the variation. A partner with a 95% realization rate and a partner with a 70% rate look the same in aggregate reporting. Breaking it out shows you where the write-downs are happening and why — insight that belongs in every partner compensation meeting. Build those presentations with Deckary.

The Law Firm Balance Sheet Template is structured with the balance sheet, trust reconciliation, and AR summary in one place — the combination that gives a complete financial position, not just the cash-basis view alone.

Common Accounting Mistakes Law Firms Make

Booking retainers as immediate income. When a client pays a $10,000 flat fee and the firm deposits it into the operating account, that $10,000 is not yet revenue. The firm owes that client legal services — it's a liability (unearned retainer) until work is performed. Recording it as income on receipt inflates reported revenue and misstates the balance sheet. This is both an accounting error and potentially an ethics issue depending on how it affects retainer management.

Neglecting WIP tracking. Attorney time that's worked but never recorded doesn't just disappear — it represents real economic loss. A timekeeper who consistently under-records by one hour per day loses roughly 250 billable hours per year. At $350/hour, that's $87,500 in revenue that was earned but never captured. Firms without consistent daily time entry have this problem at scale and usually underestimate its magnitude.

Improper treatment of client cost advances. Filing fees and other costs paid on behalf of clients should sit in an asset account, not flow through as expenses. Firms that expense them directly understate gross profit and produce margins that look lower than actual performance. When those costs are reimbursed, the recovery then looks like income — distorting both periods.

Skipping the three-way trust reconciliation. A trust discrepancy that's identified in month one is usually a single missing entry that takes 20 minutes to find. The same discrepancy discovered in month six, after 150 more transactions, can take days to untangle — if it can be traced at all.

Treating all revenue as equivalent. Hourly fees, flat fees, and contingency income have different margin profiles and different timing characteristics. A firm that pools them all into one revenue line can't evaluate the profitability of each fee structure or make informed decisions about practice mix.

Partner Compensation and Capital Accounts

Partner compensation in law firms works differently than employee compensation, and this difference has real accounting implications.

Partner draws — the regular advances equity partners take against expected annual distributions — are not operating expenses. They reduce partner capital accounts, not firm profit. This means a law firm's reported "profit" before partner distributions is not comparable to net income in a business where all workers are employees. A firm showing $800,000 in net income might have two equity partners who each took $300,000 in draws — meaning the actual distributable surplus above those draws is $200,000, not $800,000.

For management purposes, calculate profit per equity partner (PPP) — total distributable income divided by the number of equity partners. This is the number that actually benchmarks partner compensation against industry standards.

Partner capital accounts should grow over time, reflecting retained earnings rather than full distribution of every dollar. The standard expectation is that partners maintain capital balances in the range of 25–35% of annual compensation. Partners who consistently overdraw their capital accounts — taking more than they've earned — weaken the firm's financial position for everyone, and it becomes visible quickly when the firm seeks credit or a partner exits.

The Cash Flow Timing Problem

Law firms regularly run profitable on paper while being cash-constrained in practice. The reason is the gap between work performed and cash collected.

From the data: median realization lockup (work to billing) is around 43 days. Median collection lockup (billing to payment) is around 32 days. Combined, that's approximately 75 days from doing the work to having the cash. Some firms run longer — practices with slow billing cycles or clients who pay on 60–90 day terms can see combined lockup exceeding 120 days.

During growth periods, this timing gap compounds. A firm that doubles its hourly billings from one quarter to the next doesn't double its cash in the same quarter — the additional receivables sit in the pipeline for 75+ days. This is why growing firms often feel cash-constrained even when the income statement shows strong performance. Model the timing explicitly with the law firm cash flow calculator.

Managing this requires a cash flow projection that models the timing difference explicitly — not just revenue and expenses, but when cash actually arrives. The Law Firm Balance Sheet Template pairs with AR aging and WIP reporting to give visibility into the pipeline that feeds future cash.

Building Accounting Infrastructure That Works

A law firm's accounting infrastructure needs to do four things well:

- Track trust accounts with client-level sub-ledgers and monthly three-way reconciliation

- Capture billable time consistently across all timekeepers, close to when work is performed

- Bill and collect on a defined cycle with AR aging monitored weekly

- Report on realization and collection rates by timekeeper and practice group, not just firm-wide averages

Most small and mid-size firms don't need complex legal billing software to get this right. The critical pieces are the discipline to close time daily, bill on a predictable cycle, and run the reconciliation monthly — not the sophistication of the tools.

What matters is that the accounting system tells you what's actually happening: how much work is in the pipeline, how much is billed and waiting, what's been collected, and where write-downs are occurring. A system that gives you that visibility — consistently and accurately — is worth more than any feature set in legal practice management software.

Last updated: March 24, 2026

Frequently Asked Questions

Related Articles

Church Accounting Best Practices: A Practical Guide

How church accounting works — fund accounting, restricted funds, internal controls, financial reports, and the tax rules that catch churches off guard.

Church Balance Sheet Example: A Line-by-Line Breakdown

A complete church balance sheet example with real line items, fund accounting explained, and the benchmarks church boards use to assess financial health.

Construction Accounting: A Practical Guide for Contractors

Construction accounting is different from standard accounting. This guide covers job costing, WIP schedules, retainage, revenue recognition methods, and common mistakes.

Construction Balance Sheet Example: A Line-by-Line Breakdown

A complete construction company balance sheet example with real line items, WIP accounting, retainage, overbilling, and what sureties and lenders look for.

Daycare Balance Sheet Example: Line by Line

A complete daycare balance sheet example with real line items — enrollment deposits, playground equipment, subsidy receivables, and what the numbers mean.

Food Truck Balance Sheet Example: A Line-by-Line Breakdown

A complete food truck balance sheet example with real line items, truck depreciation rules, and what makes a food truck's financials different from a restaurant.