Food Truck Balance Sheet Example: A Line-by-Line Breakdown

A complete food truck balance sheet example with real line items, truck depreciation rules, and what makes a food truck's financials different from a restaurant.

The food truck balance sheet is one of the simplest in the food service industry — and also one of the most misunderstood. The truck isn't just your workplace. It's your primary asset, your primary collateral, and often your primary liability.

Understanding how that asset is valued, how debt against it is tracked, and how equity builds over time is what separates operators who know their financial position from those who are guessing.

Why a Food Truck Balance Sheet Looks Different

Every balance sheet follows the same equation: Assets = Liabilities + Equity. But what goes inside those categories differs significantly between a food truck and a brick-and-mortar restaurant.

No lease on the balance sheet. A full-service restaurant with a 10-year lease now carries that lease as both an asset (Right-of-Use asset) and a liability (lease obligation) under ASC 842. This can represent hundreds of thousands of dollars on each side of the balance sheet. Food trucks typically don't have fixed-location leases, so this complexity doesn't apply. Commissary kitchen fees are an operating expense, not a capitalized lease obligation.

The truck dominates long-term assets. In a restaurant, the kitchen equipment is spread across dozens of line items — commercial range, refrigeration, dishwasher, fryer, walk-in cooler. In a food truck, most of that equipment is inside the vehicle and often depreciated as part of the truck or as a closely related equipment category. The truck and its installed equipment can represent 70–85% of total assets.

Simpler inventory. Food trucks typically carry a day or two of inventory at most — limited storage space forces tight purchasing cycles. Where a restaurant might carry $15,000–$25,000 in inventory, a well-run food truck carries $2,000–$5,000.

Multi-jurisdiction tax complexity. A restaurant has one local sales tax rate. A food truck that operates in three cities on three different days has three different rates to track and remit separately. This shows up in the sales tax payable balance on the balance sheet and creates more bookkeeping complexity than the simpler asset structure would suggest.

The Three Sections of a Food Truck Balance Sheet

Assets

Current assets — convertible to cash within 12 months:

- Cash and cash equivalents — your business checking account and any short-term savings. The lifeline of any food service operation

- Inventory — food ingredients, packaging, condiments, and supplies on hand. Given limited truck storage, this turns over quickly — typically daily or every few days

- Accounts receivable — primarily relevant for catering contracts and event bookings where the client pays after service

- Prepaid expenses — insurance premiums paid in advance, commissary deposits, prepaid permits and licenses

Long-term assets — owned assets that won't convert to cash within 12 months:

- Food truck (vehicle) — the core asset of the business, carried at purchase price and reduced annually by accumulated depreciation. A used truck purchased for $65,000 doesn't stay at $65,000 on the balance sheet; it reduces each year as depreciation is recorded

- Kitchen equipment — fryers, griddles, refrigeration units, steam tables, and generators. Often tracked separately from the vehicle for depreciation purposes. This equipment has a 5–7 year useful life

- POS and technology systems — card readers, tablets, receipt printers, and any inventory management hardware

Liabilities

Current liabilities — due within 12 months:

- Accounts payable — outstanding invoices to food suppliers and vendors

- Sales tax payable — collected from customers at each point of sale, held until remittance. Multi-location operators track this by jurisdiction

- Payroll liabilities — wages earned but not yet paid, plus any payroll taxes owed

- Current portion of truck loan — the principal due on the truck financing in the next 12 months

- Current portion of equipment financing — if kitchen equipment was financed separately

Long-term liabilities:

- Truck loan (long-term portion) — remaining principal beyond 12 months on the vehicle loan. Typically the largest liability on the balance sheet

- Equipment financing (long-term portion) — remaining balance on any equipment loans beyond 12 months

Equity

For most food truck operators — sole proprietors and single-member LLCs — equity is:

- Owner's initial investment — cash contributed to start the business, or the personal down payment on the truck

- Retained earnings — cumulative net income kept in the business rather than withdrawn as owner draws

Equity grows when the business is profitable and the owner doesn't withdraw all profits. It shrinks when owner draws exceed net income or when the business operates at a loss. Food truck net margins typically run 7–15% for owner-operated trucks, so retained earnings can build meaningfully if the operator is disciplined about draws. For a detailed look at how those margins are built, see our food truck income statement example.

Complete Example: Owner-Operated Food Truck

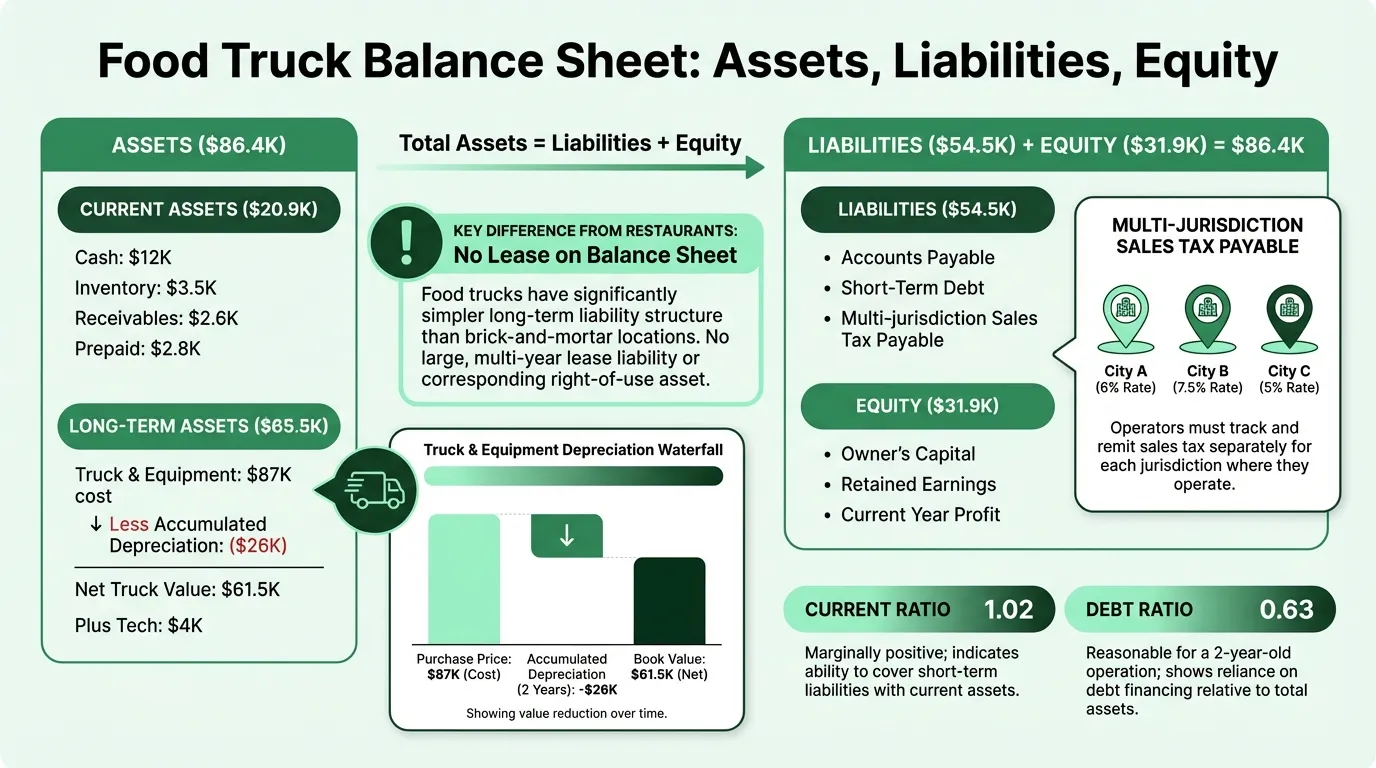

Here's a representative balance sheet for a food truck two years into operation, generating approximately $300,000 in annual revenue. The owner purchased a used truck for $65,000 and has been building the business with one part-time employee:

Assets

Current Assets

| Line Item | Amount |

|---|---|

| Cash and cash equivalents | $12,000 |

| Inventory (food and supplies) | $3,500 |

| Accounts receivable (catering) | $2,600 |

| Prepaid expenses (insurance, commissary deposit) | $2,800 |

| Total Current Assets | $20,900 |

Long-Term Assets

| Line Item | Amount |

|---|---|

| Food truck (vehicle) | $65,000 |

| Kitchen equipment | $22,000 |

| POS and technology systems | $4,500 |

| Less: accumulated depreciation | ($26,000) |

| Total Long-Term Assets | $65,500 |

Total Assets: $86,400

Liabilities

Current Liabilities

| Line Item | Amount |

|---|---|

| Accounts payable (food suppliers) | $4,200 |

| Sales tax payable (multi-jurisdiction) | $2,900 |

| Payroll liabilities | $2,400 |

| Current portion of truck loan | $11,000 |

| Total Current Liabilities | $20,500 |

Long-Term Liabilities

| Line Item | Amount |

|---|---|

| Truck loan (long-term portion) | $34,000 |

| Total Long-Term Liabilities | $34,000 |

Total Liabilities: $54,500

Equity

| Line Item | Amount |

|---|---|

| Owner's initial investment | $18,500 |

| Retained earnings | $13,400 |

| Total Equity | $31,900 |

Total Liabilities + Equity: $86,400

How the Truck Depreciation Actually Works

This is the piece most food truck operators get wrong — or skip entirely.

The IRS classifies food trucks as listed property, meaning the vehicle can be used for both personal and business purposes. To claim accelerated depreciation, you must document that business use exceeds 50% of total use. If it falls below 50%, you're required to switch to the Alternative Depreciation System, which spreads the deduction over a longer period.

Assuming the truck is used entirely for business:

MACRS 5-year recovery period. The IRS assigns food trucks a 5-year depreciation schedule. With the half-year convention, a truck placed in service anytime during Year 1 is treated as if it was placed in service halfway through the year, regardless of the actual purchase date.

Section 179 deduction. Instead of spreading the cost over 5 years, operators can elect to deduct the full purchase price in Year 1 (up to the Section 179 limit, which was $1,160,000 for 2024). The catch: the deduction cannot exceed your taxable business income for the year. This election is useful when the business has strong first-year profit.

Bonus depreciation. Until 2024, bonus depreciation allowed a 100% immediate deduction for qualifying assets. This provision phases down starting in 2025. If you're buying a truck in 2025 or later, check the current phase-out percentage.

Kitchen equipment is separate. The fryer, griddle, and refrigeration unit inside the truck are depreciated on their own schedule — typically 5–7 years under MACRS — not bundled with the vehicle. Tracking equipment separately from the truck matters for resale, insurance, and financing purposes.

What this means on the balance sheet: In the example above, the truck and equipment were purchased for a combined $87,000 two years ago. With approximately $13,000 in annual depreciation, the accumulated depreciation balance is $26,000, leaving a net book value of $65,500. The truck's book value is not the same as its market value — a 2-year-old truck on the road may be worth more or less than what the balance sheet shows.

Need a ready-made balance sheet template for your food truck?

Download a pre-built spreadsheet with industry-specific categories, formulas, and formatting.

Multi-Jurisdiction Sales Tax: The Hidden Complexity

The sales tax payable balance on a food truck balance sheet looks simple — a few thousand dollars. But calculating it correctly is significantly more complex than for a fixed restaurant.

A food truck that parks in three different cities on three different days may face three different sales tax rates. Some cities have additional local taxes layered on top of state rates. Some states tax prepared food differently than packaged food. And when you operate across city or county lines, the rates change.

This means:

- Every sale needs to be tagged by location in your POS system

- Sales tax remittance goes to separate jurisdictions, often on different schedules

- Month-end reconciliation requires breaking out sales by location, not just by day

A food truck generating $300,000 in annual revenue might carry $2,000–$4,000 in sales tax payable at any month-end, spread across multiple taxing authorities. If you're not tracking by location, you risk underremitting to one jurisdiction and overremitting to another — both of which create problems.

Commissary Costs: Operating Expense, Not Balance Sheet Item

Many cities require food trucks to use a licensed commissary for food prep, storage, and cleaning. This is commonly misunderstood from an accounting perspective.

A commissary kitchen fee of $400–$800 per month is an operating expense, not a capital expenditure. It appears on your income statement, not your balance sheet. Only if your commissary agreement is structured as a long-term lease (over 12 months) with specific criteria might it trigger ROU asset treatment under ASC 842 — and most commissary arrangements are month-to-month or short-term.

If you pay a security deposit to secure your commissary spot, that deposit goes on the balance sheet as a current asset under prepaid expenses until it's returned or applied.

What the Numbers Tell You

Current Ratio

Current Ratio = Current Assets / Current Liabilities

In this example: $20,900 / $20,500 = 1.02

A current ratio above 1.0 means current assets slightly exceed current liabilities — marginally positive working capital. Food trucks tend to have healthier current ratios than brick-and-mortar restaurants because they don't carry the large accounts payable balances that pile up from daily food deliveries. With a minimal inventory model and direct customer payment, the daily cash cycle is simpler.

A current ratio below 0.80 for a food truck — especially one without a credit line — warrants attention. It typically means the truck loan payments or vendor payables are outpacing cash generation. The food truck break-even calculator shows how many daily covers you need to stay above that threshold.

Debt Ratio

Debt Ratio = Total Liabilities / Total Assets

In this example: $54,500 / $86,400 = 0.63

A 0.63 debt ratio means 63 cents of every asset dollar is financed by liabilities. This is reasonable for a food truck two years in — most of the remaining debt is the truck loan, which has a defined payoff date. Compare this to a restaurant with a 10-year lease: once ASC 842 brings that lease onto the balance sheet, restaurant debt ratios commonly run 0.73–0.85.

As the truck loan is paid down, this ratio improves — and the equity section grows accordingly.

Net Book Value vs. Market Value

The balance sheet shows the truck at book value (cost minus accumulated depreciation). A 2-year-old truck may have a higher market value than its $39,000 book value in this example — especially if the market for used trucks in your area is competitive.

This gap matters for two reasons:

- Refinancing or resale — a lender or buyer will use market value, not book value

- Insurance — insure for replacement value, not book value

What Lenders Look At

When you apply for a second truck, equipment financing, or an SBA microloan, lenders review your balance sheet alongside income statements and bank statements.

| What They Check | What They Want to See |

|---|---|

| Current ratio | Above 0.90, not declining |

| Truck loan remaining balance | Manageable relative to revenue |

| Equity trend | Retained earnings growing |

| Cash balance | Enough to cover 2–4 weeks of operating expenses |

| Collateral | The truck — what's it worth and is it clear of liens? |

| Debt ratio | Below 0.80 for new credit |

The single most important piece: the truck is your primary collateral. Lenders want to know its current market value, whether it's fully insured, and whether any existing lender has a first lien on it. Before applying for any financing, confirm with your current lender what a payoff amount would be. The Food Truck Budget Template helps you organize the revenue projections and expense structure lenders want to see alongside your balance sheet.

Building a Food Truck Balance Sheet

Most food truck operators track daily sales and expenses but never compile a full balance sheet. That's a gap that becomes expensive when you need financing, want to sell the business, or are trying to understand whether you're actually building equity.

The Food Truck Balance Sheet Template is structured for the specific line items in this post — truck and equipment depreciation, multi-jurisdiction tax payable, commissary deposits, and the loan tracking that most generic templates miss.

For a complete financial picture, it pairs with the Food Truck P&L Template, which tracks revenue and profitability by location and event type, and the Food Truck Cash Flow Template, which maps when money actually moves given the variable nature of daily location revenue.

Three documents, three questions: the balance sheet asks what you own and owe, the P&L asks whether you're profitable, and the cash flow statement asks whether you can make the truck payment next month. None answers the others — but together, they give you a complete picture of whether the business is actually working.

Last updated: March 24, 2026

Frequently Asked Questions

Related Articles

Church Accounting Best Practices: A Practical Guide

How church accounting works — fund accounting, restricted funds, internal controls, financial reports, and the tax rules that catch churches off guard.

Church Balance Sheet Example: A Line-by-Line Breakdown

A complete church balance sheet example with real line items, fund accounting explained, and the benchmarks church boards use to assess financial health.

Construction Accounting: A Practical Guide for Contractors

Construction accounting is different from standard accounting. This guide covers job costing, WIP schedules, retainage, revenue recognition methods, and common mistakes.

Construction Balance Sheet Example: A Line-by-Line Breakdown

A complete construction company balance sheet example with real line items, WIP accounting, retainage, overbilling, and what sureties and lenders look for.

Daycare Balance Sheet Example: Line by Line

A complete daycare balance sheet example with real line items — enrollment deposits, playground equipment, subsidy receivables, and what the numbers mean.

Healthcare Balance Sheet Example: A Line-by-Line Breakdown

A complete healthcare balance sheet example for a medical practice — covers contractual adjustments, days in AR, malpractice reserves, and key financial ratios.