Law Firm Balance Sheet Example: A Line-by-Line Breakdown

A complete law firm balance sheet example with real line items, trust account treatment, partner capital accounts, and what lenders review.

Your balance sheet is a snapshot of what the firm owns, what it owes, and what partners have built. For law firms, it's also where the trust account appears — and where most bookkeeping mistakes have the highest consequences.

A law firm balance sheet has the same three-part structure as any other business: assets, liabilities, and equity. But the specific line items reflect the realities of legal practice — client funds held in trust, unbilled work sitting in the pipeline, and partner capital accounts instead of simple retained earnings.

This post walks through a complete law firm balance sheet example, line by line, with the context that makes those numbers meaningful.

The Three Sections of a Law Firm Balance Sheet

Every balance sheet follows the same equation: Assets = Liabilities + Equity. For a law firm, the most important thing to understand upfront is that many of the most significant financial items — accounts receivable, work in progress, client disbursements — may not appear on the balance sheet at all if the firm uses cash basis accounting.

Most small-to-mid-size law firms run on cash basis. This means revenue is recorded when collected and expenses when paid. The balance sheet shows what the firm actually has in cash today, not what clients owe or what work is sitting unbilled. For management purposes, you need AR aging reports and WIP schedules alongside the balance sheet to get the full picture.

Assets

Current Assets

Cash and cash equivalents — the firm's operating account. For a cash-basis firm, this is the primary asset. It should be large enough to cover payroll, overhead, and any gaps between billing and collection.

Client trust account (IOLTA) — the pooled trust account holding client retainers and settlement funds. This is a firm-controlled bank account, so it appears as a cash asset. But see the offsetting liability below — the net effect on firm equity is zero.

Accounts receivable — billed but uncollected fees. This line only appears on accrual-basis balance sheets. Cash-basis firms track this separately in AR aging reports.

Advanced client costs — out-of-pocket expenses paid on clients' behalf (filing fees, expert witness fees, deposition costs) that clients are expected to reimburse. These are real assets, often carried for months or years in contingency practices.

Prepaid expenses — rent deposits, insurance premiums, software subscriptions paid in advance.

Long-Term Assets

Furniture, equipment, and technology — desks, computers, phone systems, office build-out costs. Depreciated over useful life. For most law firms, this is a small line relative to total assets — the real assets are the people and the receivables, not the furniture.

Leasehold improvements — build-out costs for leased office space. Depreciated over the shorter of asset life or remaining lease term.

Right-of-use asset (ASC 842) — firms that adopted ASC 842 (required for private companies) now bring operating lease obligations onto the balance sheet. For a firm with a multi-year office lease, the ROU asset and corresponding liability can be the largest items on the balance sheet.

Liabilities

Current Liabilities

Client trust liability — the amount owed back to clients whose funds are held in the trust account. This must equal the trust bank balance at all times. The three-way reconciliation — bank statement, firm trust ledger, and sum of all individual client sub-ledgers — must balance monthly. Failure here is not an accounting error; it's an ethics violation subject to bar discipline.

Accounts payable — outstanding vendor invoices (office supplies, IT services, court reporters, outside counsel).

Deferred revenue (unearned retainers) — when a client pays an advance retainer and the funds are deposited into the operating account (not trust), the amount is a liability until fees are actually earned. This is a common mistake: many firms book retainers directly as income upon receipt, which misstates both revenue and the balance sheet. For the full treatment of trust accounting rules and commingling risks, see our law firm accounting guide.

Accrued expenses — payroll, benefits, and operating costs that have been incurred but not yet paid.

Current portion of any term loans — principal due in the next 12 months.

Long-Term Liabilities

Operating lease liability (long-term) — the present value of remaining lease payments beyond 12 months, brought onto the balance sheet under ASC 842.

Term loans (long-term portion) — principal balance on any business loans beyond 12 months.

Equity

This is where law firms differ most from other businesses.

For a sole proprietorship or single-member LLC: a single owner's equity account.

For a partnership or LLP: individual partner capital accounts, one per equity partner. Each capital account follows this formula:

Beginning balance + Contributions + Profit allocations – Draws – Loss allocations = Ending balance

Partner draws — the regular advances equity partners take against expected profits — are deducted directly from each partner's capital account. They do not appear as expenses on the income statement. This is categorically different from associate salaries, which are operating expenses that reduce reported net income.

The practical implication: when reading a law firm income statement, reported "profit" doesn't represent what partners actually take home. It's profit before partner distributions.

Industry standards suggest equity partners contribute roughly 25–35% of their annual compensation as firm capital. For a partner earning $400,000 per year, that means a capital balance in the $100,000–$140,000 range is expected.

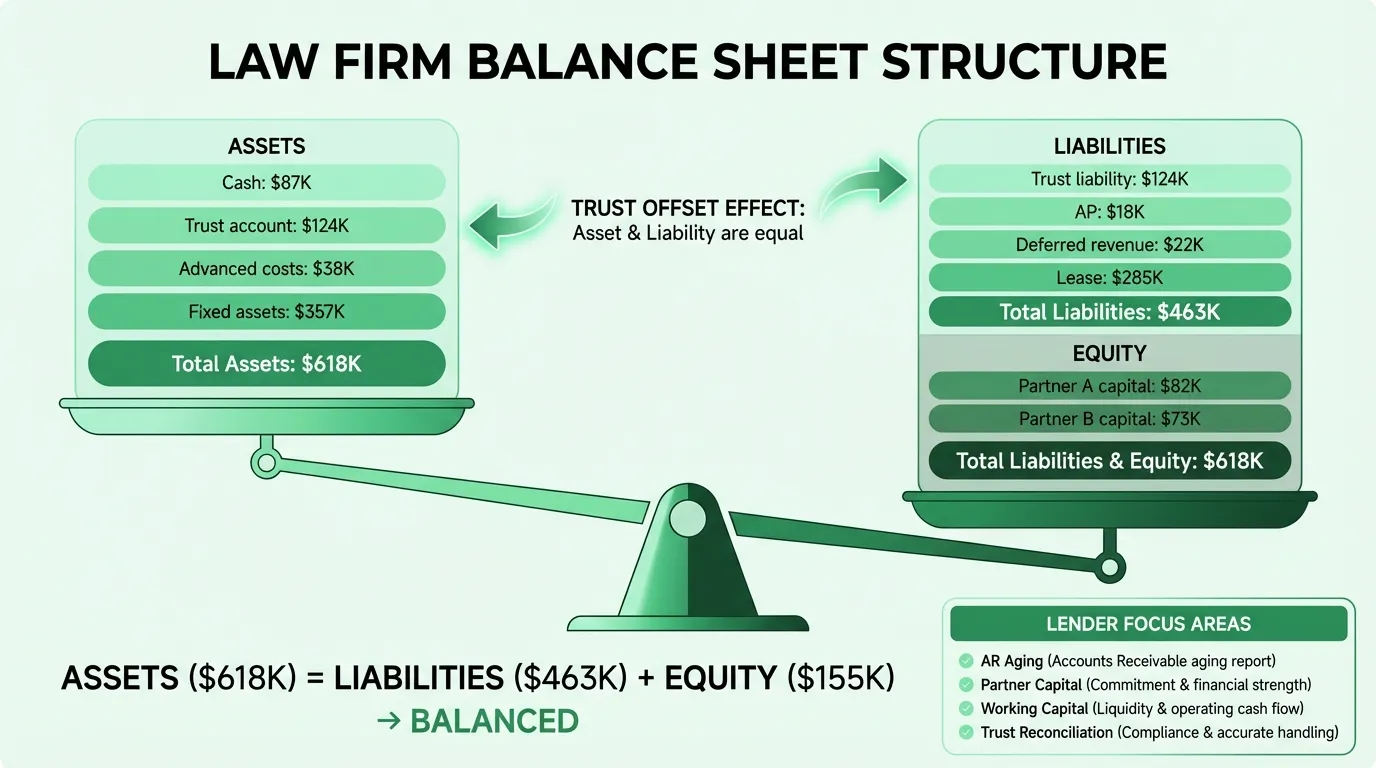

Complete Example: Small Litigation Firm

Here's a representative balance sheet for a four-attorney litigation firm doing approximately $1.5M in annual revenue, with two equity partners.

Assets

Current Assets

| Line Item | Amount |

|---|---|

| Cash — operating account | $87,000 |

| Cash — client trust account (IOLTA) | $124,000 |

| Advanced client costs (disbursements receivable) | $38,000 |

| Prepaid expenses | $12,000 |

| Total Current Assets | $261,000 |

Long-Term Assets

| Line Item | Amount |

|---|---|

| Furniture and equipment | $68,000 |

| Leasehold improvements | $45,000 |

| Less: accumulated depreciation | ($41,000) |

| Right-of-use asset (operating lease) | $285,000 |

| Total Long-Term Assets | $357,000 |

Total Assets: $618,000

Liabilities

Current Liabilities

| Line Item | Amount |

|---|---|

| Client trust liability (funds held in trust) | $124,000 |

| Accounts payable | $18,000 |

| Deferred revenue (unearned retainers) | $22,000 |

| Accrued payroll and benefits | $14,000 |

| Current portion of operating lease | $38,000 |

| Total Current Liabilities | $216,000 |

Long-Term Liabilities

| Line Item | Amount |

|---|---|

| Operating lease liability (long-term) | $247,000 |

| Total Long-Term Liabilities | $247,000 |

Total Liabilities: $463,000

Equity

| Line Item | Amount |

|---|---|

| Partner A — capital account | $82,000 |

| Partner B — capital account | $73,000 |

| Total Equity | $155,000 |

Total Liabilities + Equity: $618,000

Need a ready-made balance sheet template for your law firm?

Download a pre-built spreadsheet with industry-specific categories, formulas, and formatting.

What the Numbers Mean

The Trust Account Is Self-Canceling

Notice that the $124,000 client trust asset is exactly offset by the $124,000 client trust liability. The net contribution to firm equity is zero. This is correct — those are client funds, not firm funds. But both lines must be on the balance sheet. The asset confirms the money exists; the liability confirms it's owed back.

Every month, those two numbers must match each other — and both must match the trust bank statement and the sum of individual client sub-ledgers. If they don't, something has gone wrong.

The Balance Sheet Doesn't Show the Full Picture

In this example, the operating account shows $87,000 in cash. But the firm likely has additional activity that doesn't appear here at all:

- AR aging: Billed but uncollected invoices sitting with clients. A firm doing $1.5M in annual revenue might have $150,000–$250,000 in outstanding AR that won't show on a cash-basis balance sheet.

- WIP schedule: Attorney time worked on active matters but not yet billed. If realization lockup runs 30–45 days at this revenue level, there's $120,000–$190,000 in work in progress off the balance sheet.

The Law Firm Balance Sheet Template is built to track all three: the balance sheet, an AR aging summary, and a WIP schedule — so you have a complete picture of the firm's financial position, not just what cash-basis accounting shows.

Partner Capital vs. Retained Earnings

Total equity here is $155,000 across two partner capital accounts. This represents cumulative contributions and profit allocations, net of draws taken over time. In a healthy firm, partner capital accounts should be growing — reflecting retained profits rather than full distribution of every dollar earned.

A firm where partners have systematically withdrawn capital below the expected 25–35% of compensation threshold is a yellow flag for lenders and a risk factor if a partner departs or the firm needs to borrow.

The Deferred Revenue Problem

The $22,000 in deferred revenue (unearned retainers) is a line many law firms don't track correctly.

When a client pays a $10,000 flat-fee retainer and the firm deposits it into the operating account, that $10,000 is not yet income. The firm hasn't earned it. It's a liability — the firm owes that client legal services. Booking it as revenue on receipt is incorrect and inflates reported income.

As the firm delivers services against that retainer, it transfers earned amounts from deferred revenue to income. If the matter ends before the retainer is exhausted, any unearned balance must be returned to the client.

For retainers held in trust (the client's funds stay in the IOLTA account until earned), the accounting is different: trust asset and trust liability increase by the deposit, and the transfer to earned income only happens when the firm properly withdraws earned fees from trust to the operating account.

What Lenders Look At

Law firm lenders evaluate different things than lenders in other industries. There are few hard assets to collateralize — the real value is in the AR and the pipeline.

| What They Check | What They Want to See |

|---|---|

| AR aging report | Minimal balance over 90 days; high collection realization rate (85%+) |

| Client concentration | No single client over 15–20% of revenue |

| Partner capital | Adequate balances; not over-drawn |

| Working capital | 10–30% of annualized revenue in cash + credit |

| Trust account | Clean three-way reconciliation; no bar investigations |

| WIP schedule | Active matters as evidence of future billing capacity |

| Personal guarantees | Required for partners owning 20%+ of the firm |

Unlike a manufacturer seeking equipment financing, a law firm's borrowing base is almost entirely the quality and collectibility of its receivables. A firm with clean, current AR and growing partner capital is a fundamentally different credit than one with 60% of AR aged beyond 90 days. Use our law firm profit margin calculator to benchmark collection performance against industry averages.

Balance Sheet Mistakes Law Firms Make

Commingling trust and operating funds. The most serious. Depositing client retainers into the operating account when they should be in trust — or covering operating expenses from trust — is a bar discipline matter, not just an accounting error. Many firms do it by accident in the early years.

Not reconciling trust accounts monthly. The three-way reconciliation is required under most state bar rules, but many firms run it quarterly or skip it altogether. A trust account discrepancy that compounds for 6–12 months before discovery is much harder to untangle than one caught monthly.

Booking retainers as immediate income. Advance fees held in the operating account are deferred revenue until earned. Recording them as income upon receipt overstates revenue and misstates the balance sheet.

Ignoring the off-balance-sheet gap. A cash-basis balance sheet that looks healthy may be hiding $200,000 in uncollected AR and a stalled WIP pipeline. Running the balance sheet without AR aging and WIP schedules is managing by partial information. For a complete look at how revenue, expenses, and overhead ratios interact, see our law firm budget example.

Under-funding partner capital. Partners who take out more than they've earned, or who contribute less than expected, are weakening the firm's balance sheet for everyone. This matters most when a partner exits, the firm seeks credit, or a partner needs to demonstrate financial health to lenders for a personal transaction.

Using the Balance Sheet Month to Month

For most firms, the balance sheet is reviewed annually — by the accountant, when taxes are due. That's too infrequent to catch problems early.

A monthly review should check:

- Trust account balance vs. trust liability — they should match exactly

- Advanced client costs — are they growing? That may signal slow billing or collection on disbursements

- Deferred revenue — is it decreasing as the firm earns fees, or accumulating? Track all of these items with the law firm KPI dashboard template.

- Partner capital accounts — growing over time (healthy) or declining (partners drawing down equity)?

- AR aging (supplementary) — what percentage is over 90 days?

The Law Firm Balance Sheet Template structures this monthly review with the balance sheet, trust reconciliation, and AR summary in one place. For the full financial picture, it pairs with an income statement tracking revenue and expenses by matter type and a cash flow projection to manage timing between billing and collection.

The balance sheet doesn't run the firm. But the firms that review it monthly — not just annually — catch problems when they're still manageable.

Last updated: March 24, 2026

Frequently Asked Questions

Related Articles

Church Accounting Best Practices: A Practical Guide

How church accounting works — fund accounting, restricted funds, internal controls, financial reports, and the tax rules that catch churches off guard.

Church Balance Sheet Example: A Line-by-Line Breakdown

A complete church balance sheet example with real line items, fund accounting explained, and the benchmarks church boards use to assess financial health.

Construction Accounting: A Practical Guide for Contractors

Construction accounting is different from standard accounting. This guide covers job costing, WIP schedules, retainage, revenue recognition methods, and common mistakes.

Construction Balance Sheet Example: A Line-by-Line Breakdown

A complete construction company balance sheet example with real line items, WIP accounting, retainage, overbilling, and what sureties and lenders look for.

Daycare Balance Sheet Example: Line by Line

A complete daycare balance sheet example with real line items — enrollment deposits, playground equipment, subsidy receivables, and what the numbers mean.

Food Truck Balance Sheet Example: A Line-by-Line Breakdown

A complete food truck balance sheet example with real line items, truck depreciation rules, and what makes a food truck's financials different from a restaurant.