Church Accounting Best Practices: A Practical Guide

How church accounting works — fund accounting, restricted funds, internal controls, financial reports, and the tax rules that catch churches off guard.

Church accounting follows the same double-entry principles as any other organization, but the purpose is different. A business tracks profit. A church tracks accountability — to donors, to the congregation, and to the purpose behind every dollar given.

That distinction shapes everything: how funds are classified, how financial statements are structured, and why internal controls matter more than most church leaders realize.

Fund Accounting: The Layer Beneath the Balance Sheet

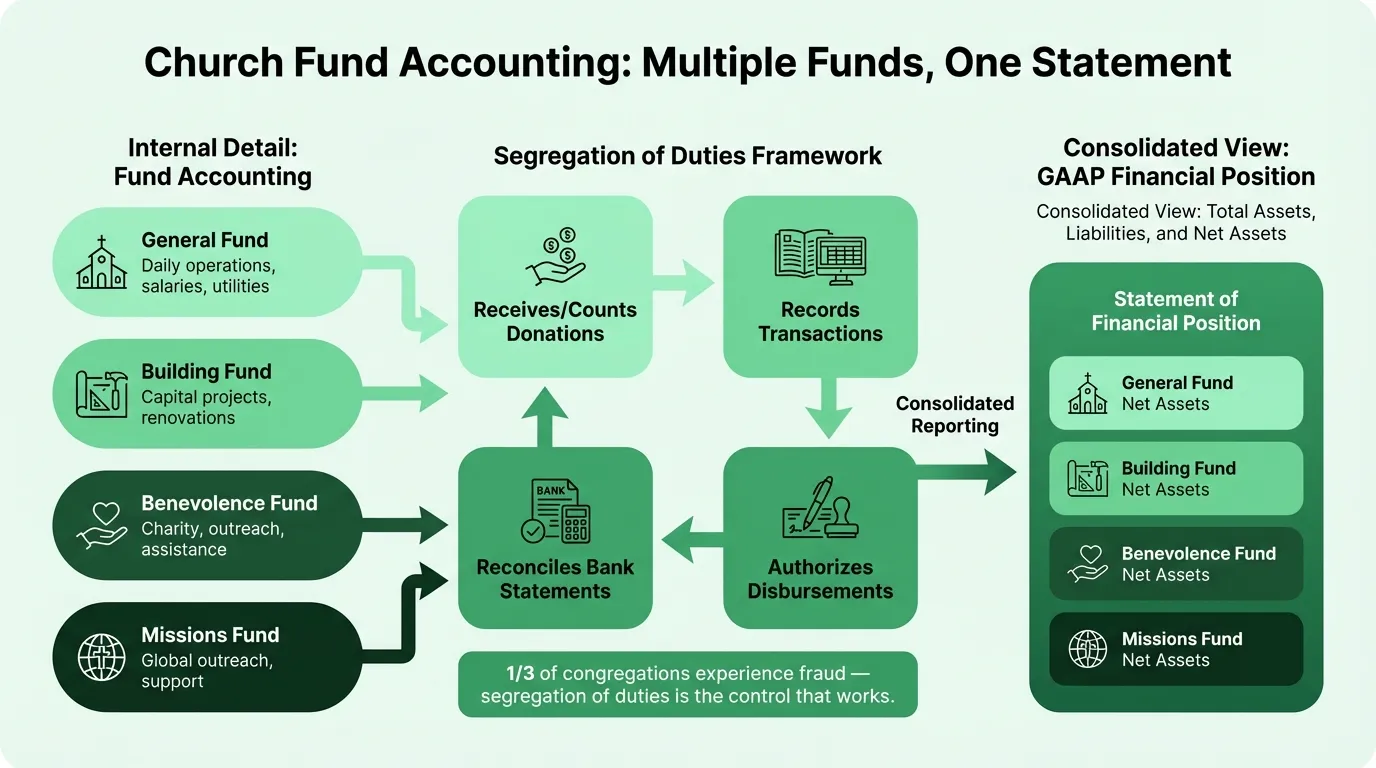

Most businesses track one pool of money. Churches track many.

Fund accounting organizes the books by purpose. A church typically maintains several funds running simultaneously:

- General Fund — unrestricted giving, tithes, and weekly offerings that leadership can spend as needed

- Building Fund — designated for construction, renovation, or facility debt

- Benevolence Fund — for members or community members in need

- Missions Fund — for local or international mission partnerships

- Special Purpose Funds — youth retreats, capital campaigns, equipment purchases

Each fund has its own income and expense tracking. The general ledger consolidates all of them — but the fund-level detail is what tells you whether donor-restricted money is being handled correctly.

Under FASB ASC 958 (the U.S. GAAP standard for nonprofits, which applies to churches), net assets fall into two classes:

Net Assets Without Donor Restrictions — general offerings and tithes that the board can allocate freely, including board-designated reserves.

Net Assets With Donor Restrictions — gifts earmarked by the donor for a specific purpose. These can only be spent on that purpose. When the purpose is fulfilled, the restriction is formally "released" via journal entry and the funds transfer to unrestricted.

Spending restricted funds on operations — even temporarily — violates donor intent and creates both ethical and legal exposure. This is the most common financial error churches make, and it's almost always unintentional: someone sees cash in an account and doesn't realize it's restricted. A properly structured church balance sheet makes restricted versus unrestricted funds visible at a glance.

The Church Balance Sheet Template is structured to keep the two net asset classes visible alongside fund balances — the combination that prevents accidental misallocation.

Segregation of Duties: The Most Important Control

Approximately one-third of all congregations experience some form of theft or fraud, according to Church Law & Tax research. Fraud takes place over an average of seven years — small amounts, taken intermittently, by someone with unchecked access.

The root cause is almost always the same: one person controls too many steps in the financial process.

Effective segregation of duties separates four roles:

| Function | Who Does It |

|---|---|

| Receives/counts donations | Counter A and Counter B |

| Records transactions | Bookkeeper |

| Authorizes disbursements | Pastor/board member |

| Reconciles bank statements | Person independent of all above |

Specific rules that matter most:

- The person who counts offerings should not be the one who records the deposit

- The person who writes checks should not sign them

- Bank reconciliation must be done by someone independent of both deposits and disbursements

- Dual signatures required on checks above a set threshold (typically $500-$1,000)

- No pre-signed blank checks; no signature stamps

- Fidelity bond (employee dishonesty insurance) covering all who handle money

- Track all disbursements against the approved church budget before authorizing payment

GuideStone's segregation of duties checklist adds one more: roles should rotate periodically, and unannounced audits should supplement scheduled annual reviews. The goal isn't distrust — it's removing the opportunity for a problem to develop undetected.

Offering Counting Procedures

Donation counting is the highest-risk moment in church finances because cash moves hands without a paper trail. The standard procedure:

- Two or three counters with no family relationship count together — never alone

- All counters remain present until the deposit is prepared and sealed

- Donations are recorded in donor management software during the counting process

- Deposit is made the same day or next business day

- A counting sheet is signed by all counters and retained

Online giving through platforms like Tithe.ly or Vanco creates its own paper trail automatically — which is one reason approximately 50% of church donations now arrive via card or digital methods. For these gifts, the receipt and reconciliation process is more straightforward, but someone still needs to reconcile digital giving reports against the church's accounting records monthly.

The Financial Reports That Matter

Churches operating under FASB ASC 958 should produce four financial statements:

Statement of Financial Position — the church balance sheet, showing assets, liabilities, and net assets split by restriction class. This replaces the traditional balance sheet for churches and nonprofits.

Statement of Activities — the church income statement, tracking revenue and expenses within each net asset class. Most leadership teams review this monthly.

Statement of Functional Expenses — allocates expenses by both type (salaries, utilities, supplies) and ministry function (worship, children's ministry, administration). Required for audited financial statements; best practice for all churches because it shows what ministry programs actually cost.

Statement of Cash Flows — tracks actual cash movement, independent of accounting timing. Particularly important for churches with restricted funds that may show strong net assets on paper while operating funds are thin.

Beyond these, useful internal reports include:

- Monthly budget-vs-actual variance report — shows leadership where spending is tracking against plan

- Quarterly board report — financials with narrative context for the finance committee

- Annual congregational report — churches that share financial results with their congregation report stronger giving and donor trust. Research from Jitasa found that 57% of churches that saw increased giving attributed part of it to financial transparency.

The Church Income Statement Template and Church Budget Template give you a starting point for both the monthly P&L view and the budget-versus-actual tracking that keeps leadership informed.

Need a ready-made p&l template for your church?

Download a pre-built spreadsheet with industry-specific categories, formulas, and formatting.

Budget Allocation Benchmarks

Knowing what to spend where is easier when you have benchmarks. According to Vanderbloemen's research on church finances:

| Category | Typical Range | Notes |

|---|---|---|

| Staff compensation (salary + benefits) | 46–60% | ~52% average; includes all staff |

| Facilities (mortgage, utilities, maintenance) | 20–30% | |

| Ministry and outreach | 10–15% | |

| Missions and charitable giving | 10–15% | |

| Savings and reserves | 5–10% | Target 3–6 months of operating costs |

One finding worth noting: faster-growing churches tend to operate with budgets approximately 25% smaller than peer churches of the same size. The discipline of constrained budgeting often forces prioritization that benefits growth.

For cash reserves, the 2024 Christian Standard survey of 240 churches found an average of 22 weeks of operating cash — down from 30 weeks the prior year. Financial experts recommend a minimum of 13 weeks. Churches that let reserves fall below one to two months of expenses become vulnerable to seasonal giving dips or unexpected expenses. You can model reserve targets against actual cash using the church cash flow calculator.

Tax Rules That Catch Churches Off Guard

Churches are exempt from filing Form 990 — a significant regulatory advantage. But several tax obligations apply regardless of that exemption.

Form 990-T (Unrelated Business Income Tax) — Any church earning $1,000 or more in gross unrelated business income must file Form 990-T and pay corporate tax on net profits from those activities. Common sources of UBIT: parking fees from non-members, facility rentals for commercial events, advertising revenue. Due the 15th day of the 5th month after fiscal year end.

Payroll obligations — Churches with employees file Form 941 (quarterly payroll returns) or Form 944 (annual). All employees — including clergy — receive W-2s by January 31. Independent contractors paid $600 or more receive 1099-NEC forms. The IRS is clear: employed ministers are employees for income tax purposes and receive W-2s, not 1099s.

Minister's housing allowance — One of the most valuable tax benefits in church employment, and one of the easiest to lose through a procedural error. Ministers can exclude a designated housing allowance from federal income tax — capped at the lesser of the amount designated, the amount actually spent, or the fair rental value of the home including utilities. The board must formally designate the allowance before January 1 of the applicable year via a board resolution recorded in meeting minutes. It cannot be designated retroactively. One catch: the allowance is excluded from income tax but is still subject to self-employment (SECA) tax.

Employee vs. self-employed distinction for ministers — Ministers occupy a unique tax status. For income tax withholding, they are employees. For Social Security and Medicare (FICA/SECA), they are self-employed. This means the church does not withhold FICA taxes for ministers — instead, ministers pay SECA tax on their full ministerial income, including housing allowance. Many churches provide a Social Security offset as part of compensation to help cover this.

Common Accounting Mistakes

Booking restricted gifts as general income. A $5,000 building fund gift is not available for operations. Recording it to general revenue and spending it on payroll is both an accounting error and an ethical breach. Every restricted gift needs its own fund tracking from receipt to expenditure to restriction release.

Missing the housing allowance designation. The designation must be made before the tax year begins. Churches that wait until March to document December's housing allowance have lost the exclusion for that period. The board resolution takes five minutes; schedule it as a December agenda item every year.

Neglecting the bank reconciliation. Monthly reconciliation done by someone independent of deposit and disbursement functions is the single most effective fraud-detection control available to small churches. Skipping it or delegating it to the wrong person eliminates the control entirely.

92% of churches create financial reports, but very few share them with the congregation — according to data from Jitasa. Transparency builds donor trust; keeping financials internal by default undermines it.

Treating all fund balances as available cash. A church with $150,000 in total fund balances may have $90,000 restricted to the building campaign and $40,000 in a benevolence reserve — leaving only $20,000 in genuinely unrestricted operating funds. The fund-level detail is what tells you what's actually available.

Building Accounting Infrastructure That Works

The fundamentals for a church's accounting system:

- Chart of accounts structured by fund — separate equity accounts for each fund, with revenue and expense sub-accounts that allow fund-level reporting

- Monthly bank reconciliation — done by someone independent of all cash handling

- Dual authorization on disbursements — two signatures above a defined threshold

- Offering counting procedures — two-person minimum, documented with a signed count sheet

- Monthly financial reports — Statement of Activities and budget-vs-actual at minimum, reviewed by leadership before the next month closes

Small churches often manage this in QuickBooks or Xero with manual fund tracking via classes or locations. Church-specific software (Aplos, PowerChurch, Realm) has fund accounting built in, which reduces the risk of configuration errors. Either approach works if the underlying procedures are solid.

The procedures matter more than the software. A church with disciplined controls and a basic spreadsheet is better positioned than one with sophisticated software and no segregation of duties.

Last updated: March 25, 2026

Frequently Asked Questions

Related Articles

Church Balance Sheet Example: A Line-by-Line Breakdown

A complete church balance sheet example with real line items, fund accounting explained, and the benchmarks church boards use to assess financial health.

Construction Accounting: A Practical Guide for Contractors

Construction accounting is different from standard accounting. This guide covers job costing, WIP schedules, retainage, revenue recognition methods, and common mistakes.

Construction Balance Sheet Example: A Line-by-Line Breakdown

A complete construction company balance sheet example with real line items, WIP accounting, retainage, overbilling, and what sureties and lenders look for.

Daycare Balance Sheet Example: Line by Line

A complete daycare balance sheet example with real line items — enrollment deposits, playground equipment, subsidy receivables, and what the numbers mean.

Food Truck Balance Sheet Example: A Line-by-Line Breakdown

A complete food truck balance sheet example with real line items, truck depreciation rules, and what makes a food truck's financials different from a restaurant.

Healthcare Balance Sheet Example: A Line-by-Line Breakdown

A complete healthcare balance sheet example for a medical practice — covers contractual adjustments, days in AR, malpractice reserves, and key financial ratios.