Church Income Statement Example: A Line-by-Line Guide

A practical church income statement example — covering tithes, designated funds, housing allowances, and the budget benchmarks healthy churches use.

A church income statement tells a different story than a business profit-and-loss. There's no revenue target tied to market growth, and there's no profit to distribute. The statement answers one question: did the congregation deploy its resources in ways that advance the mission — and does the financial position support continuing to do that next year?

Understanding how to read one — and how to structure one — matters whether you're on the finance committee, presenting to your elder board, or just trying to understand where the Sunday offering goes.

What Churches Call the Income Statement

Under FASB ASC 958, the accounting standard governing nonprofits, the formal name is Statement of Activities. You'll see that term in audited financials, loan applications, and grant submissions. Internally, many churches call it the income statement, the financial report, or the budget report — all the same document.

The structure differs from a business income statement in three important ways:

| Business Income Statement | Church Statement of Activities | |

|---|---|---|

| Bottom line | Net income / profit | Change in net assets |

| Purpose | Show profit to owners | Demonstrate stewardship to members |

| Fund types | Not applicable | General fund + designated funds |

| Tax filing | Required annually | No Form 990 required |

| Public disclosure | Private | Private (unlike other nonprofits) |

The "no Form 990" point deserves emphasis. Most nonprofits file Form 990 annually, which is public record — searchable by anyone. Churches are exempt. That exemption makes internal reporting practices more important, not less. Members can't look up your finances on ProPublica. The only transparency comes from what your leadership chooses to share.

How Church Revenue Is Organized

Tithes and offerings represent roughly 85% of the average church's total income. The remaining 15% comes from a mix of sources that vary by congregation size and ministry mix.

Tithes and regular giving — recurring contributions from members, typically given weekly or monthly. This is the financial foundation of most churches. Only about 27% of regular churchgoers tithe at the traditional 10% level; the average actual giving rate runs closer to 2.5% of income, according to Barna and Vanco Payments research. Online and recurring digital giving now accounts for approximately half of all church donations.

General offerings — one-time or irregular contributions, including special collections during services.

Designated gifts — donor-restricted contributions earmarked for a specific purpose: building fund, missions fund, youth retreat, benevolence fund. These are legally restricted to the stated purpose and must be tracked separately. Under FASB ASC 958, they're classified as net assets with donor restrictions. See how these restricted balances appear in a church balance sheet example.

Special fundraising — fundraising events average roughly 4% of the typical church's total revenue.

Facility rental income — leasing space to outside groups (preschools, community organizations, other congregations) also averages around 4% for churches that have this arrangement.

Program fees — fees charged for preschool, daycare, camps, or other fee-based programs.

Investment and endowment income — interest, dividends, or distributions from reserve accounts or endowments.

How Church Expenses Are Organized

Church budgets follow recognizable patterns regardless of denomination or size. Finance consultants typically track five categories:

Staff compensation (43–55% of budget) — the single largest line item in almost every church budget. Includes senior pastor salary, associate and ministry staff salaries, administrative staff, payroll taxes, health insurance, and retirement contributions. One line unique to churches: the pastor's housing allowance, which is excluded from the pastor's federal income taxes under IRC Section 107. This must be designated in advance by the governing board and tracked separately from regular salary.

Facilities and operations (20–30%) — mortgage or rent, utilities, building maintenance, insurance, janitorial, landscaping, and capital improvements. For churches carrying a building mortgage, this category often lands at the high end of the range.

Missions and outreach (5–15%) — local benevolence, community outreach programs, national and international missions support, and missionary partnerships. Churches with strong missions commitments often target 10–15% of their budget here.

Ministry programs (8–15%) — worship and music, children's and youth ministry, small groups, discipleship programs, curriculum, and event costs.

Administration (5–10%) — office supplies, church management software, accounting and audit fees, communications, and website.

Worked Example: Mid-Sized Community Church

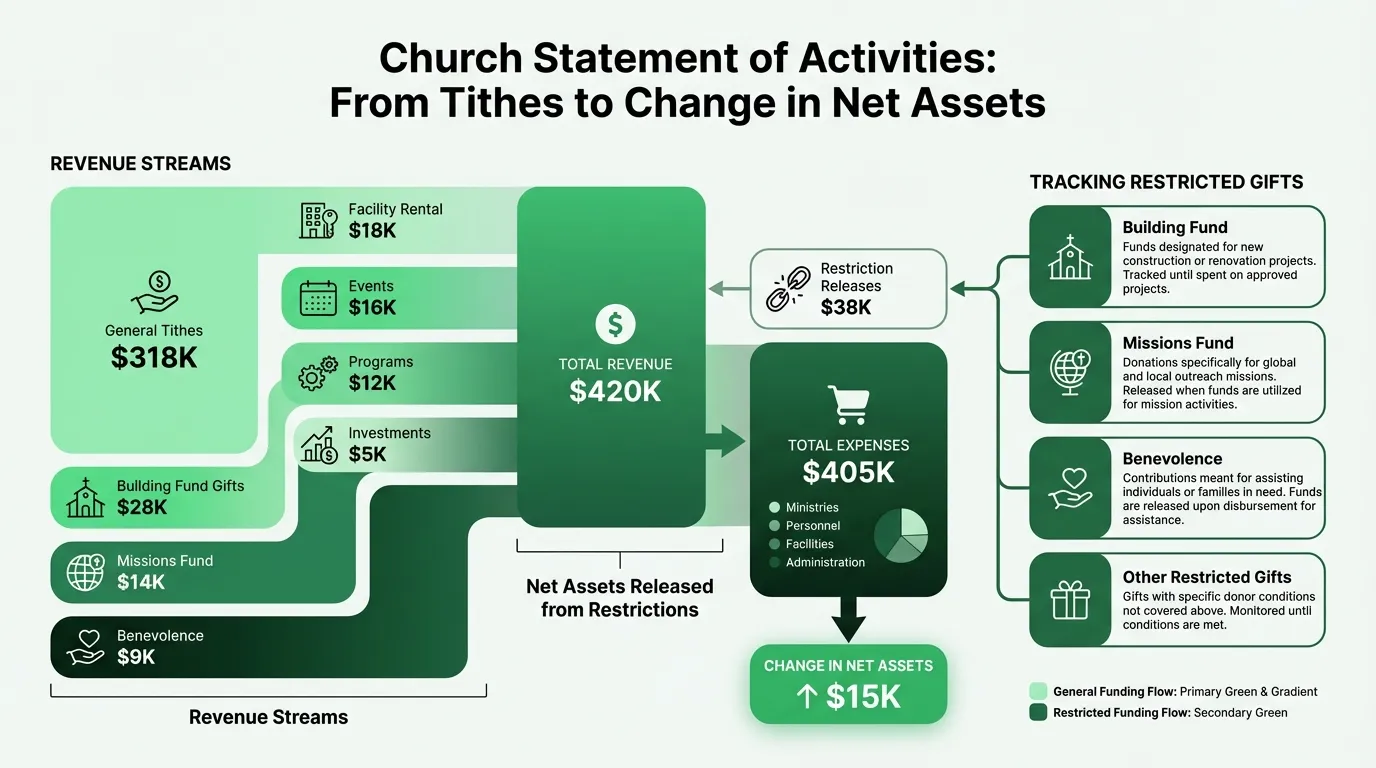

Here's a realistic annual statement of activities for a church with 180 regular attenders and $420,000 in annual income:

Revenue

| Revenue Category | Without Restrictions | With Restrictions | Total |

|---|---|---|---|

| Tithes and regular offerings | $318,000 | — | $318,000 |

| Designated gifts (building fund) | — | $28,000 | $28,000 |

| Designated gifts (missions fund) | — | $14,000 | $14,000 |

| Designated gifts (benevolence) | — | $9,000 | $9,000 |

| Facility rental income | $18,000 | — | $18,000 |

| Special fundraising events | $16,000 | — | $16,000 |

| Program fees (preschool) | $12,000 | — | $12,000 |

| Investment income | $5,000 | — | $5,000 |

| Net assets released from restrictions | $38,000 | ($38,000) | — |

| Total Revenue | $407,000 | $13,000 | $420,000 |

The release line moves $38,000 from restricted to unrestricted as designated funds are spent on their stated purposes during the year (building repairs, missions trips, benevolence assistance).

Expenses

| Expense Category | Amount | % of Budget |

|---|---|---|

| Senior pastor salary | $78,000 | 18.6% |

| Pastor housing allowance | $24,000 | 5.7% |

| Ministry staff (worship, youth, children) | $72,000 | 17.1% |

| Administrative staff | $28,000 | 6.7% |

| Payroll taxes and benefits | $26,000 | 6.2% |

| Total Staff Compensation | $228,000 | 54.3% |

| Mortgage payment | $42,000 | 10.0% |

| Utilities | $22,000 | 5.2% |

| Building maintenance and repairs | $18,000 | 4.3% |

| Insurance | $8,000 | 1.9% |

| Total Facilities | $90,000 | 21.4% |

| Local missions and benevolence | $22,000 | 5.2% |

| International missions support | $18,000 | 4.3% |

| Total Missions and Outreach | $40,000 | 9.5% |

| Worship and music | $12,000 | 2.9% |

| Children's and youth ministry | $14,000 | 3.3% |

| Small groups and discipleship | $6,000 | 1.4% |

| Total Ministry Programs | $32,000 | 7.6% |

| Office and technology | $8,000 | 1.9% |

| Communications and marketing | $4,000 | 1.0% |

| Other administration | $3,000 | 0.7% |

| Total Administration | $15,000 | 3.6% |

| Total Expenses | $405,000 | 100% |

Change in Net Assets

| Amount | |

|---|---|

| Total revenue | $420,000 |

| Total expenses | $405,000 |

| Change in net assets | $15,000 |

| Net assets, beginning of year | $68,000 |

| Net assets, end of year | $83,000 |

This church is building reserves — net assets grew by $15,000, giving them roughly two months of operating expenses in unrestricted reserves. For a structured approach to building that reserve, see our church budget example with percentage benchmarks.

Need a ready-made income statement template for your church?

Download a pre-built spreadsheet with industry-specific categories, formulas, and formatting.

What Healthy Budget Percentages Look Like

Two allocation models are commonly used as targets in church finance:

The 50/30/20 model: 50% staff, 30% facilities, 20% ministry and missions. Practical for churches carrying building debt or in early growth stages where facility costs are high.

The 33/33/33 model: One-third each to staff, facilities, and ministry/missions. This is a more generous ministry allocation and is often a goal for established churches with paid-off facilities or shared space.

The example above runs 54% staff, 21% facilities, and 25% ministry/missions/admin — close to the 50/30/20 model, appropriate for a church of this size still carrying mortgage debt.

By attendance size, Lifeway Research reports these median annual income figures for churches:

| Attendance | Median Annual Income |

|---|---|

| 50 or fewer | $66,000 |

| 51–100 | $177,000 |

| 101–250 | $300,000 |

| 251–400 | ~$700,000 |

| Over 400 | $2.5M+ |

A 180-attendee church at $420,000 is above the median for its size range — a sign of a congregation with above-average per-capita giving or additional non-offering revenue streams.

Fund Accounting: What Makes Church Financials Different

Most churches use fund accounting — a system where each designated purpose has its own sub-ledger tracking balance and activity independently, even though the organization reports as a single entity.

Your church might maintain:

- General Fund (unrestricted operating)

- Building Fund (designated for facilities)

- Missions Fund (designated for missions)

- Youth Ministry Fund (designated for youth)

- Benevolence Fund (for member assistance)

Each fund tracks its own contributions received, expenses charged, and ending balance. A donation to the building fund cannot pay the electric bill — even if the general fund is tight — unless the donor releases the restriction in writing or the funds are designated for that purpose.

This is why a church can show a positive change in net assets overall while struggling to cover operations: the net assets might be predominantly restricted funds you can't touch for day-to-day expenses.

The Church Income Statement Template is built to handle fund accounting — tracking each fund's balance, restricted vs. unrestricted amounts, and year-over-year changes alongside the consolidated statement.

The Housing Allowance Line

One expense line unique to churches: the pastor's housing allowance under IRC Section 107. This portion of a pastor's compensation is excluded from federal income tax (though not from self-employment tax) when designated in advance by the governing board.

On the income statement, housing allowance typically appears as a separate line from salary — either as a sub-line under pastoral compensation or as a distinct expense entry. It must be:

- Designated before the year begins by official board action

- Used for actual housing expenses (rent/mortgage, utilities, furnishings)

- Not exceed the fair rental value of the home furnished and equipped

Tracking this separately matters for both accurate financial reporting and IRS compliance. If your income statement lumps housing allowance into a single "pastor compensation" line without distinguishing the two, you're losing visibility into the actual structure of your largest expense category.

What to Review Each Quarter

A church statement of activities reviewed once a year is a compliance document. Reviewed quarterly by the finance committee, it becomes a stewardship tool.

Four checks that matter most:

1. Designated fund balances. Are restricted funds growing faster than you can deploy them? Sitting on $80,000 in a building fund with no building project in sight creates donor questions and accounting complexity. Having a plan for designated balances is part of responsible stewardship.

2. Staff cost percentage trend. If staff compensation as a percentage of total budget is creeping up year over year — approaching 60%+ — that's a signal. Either programs and missions are being crowded out, or revenue growth isn't keeping pace with staffing decisions.

3. Operating reserve. The change in net assets line tells you whether unrestricted reserves grew or shrank. Most church finance consultants recommend maintaining 2–3 months of operating expenses in unrestricted reserves. Under one month is financially vulnerable, especially given how quickly attendance (and giving) can shift. Check your position against the reserve benchmarks in our church accounting best practices guide.

4. Missions giving percentage. This line often reflects the congregation's sense of outward focus. A church that has slid from 12% to 7% missions giving over three years, with the difference absorbed by staff costs, has a different character than one holding steady. Leadership should track it intentionally.

If you're also managing the planning side — building the annual budget, tracking actuals against plan — the Church Budget Template pairs with the income statement for budget-vs-actual reporting across the same expense categories.

Presenting Financials to Your Congregation

Because churches don't file Form 990, financial transparency is entirely self-governed. Members cannot look up your finances externally. Many congregations present financial updates quarterly from the pulpit and make full statements available to members on request or annually at a business meeting.

A clear, well-structured statement of activities — showing where tithes and offerings were spent, how designated funds were deployed, and whether the church is building or drawing down reserves — is one of the most direct demonstrations of financial stewardship available to church leadership. It turns a compliance document into a trust-building communication. Use the Church Expense Tracker Template to keep line-item detail organized throughout the year so year-end reporting is straightforward.

Last updated: March 23, 2026

Frequently Asked Questions

Related Articles

Coffee Shop Income Statement Example: Revenue, Costs, and Margins

A coffee shop income statement example with beverage cost benchmarks, labor targets, prime cost rules, and a worked P&L for an independent café doing $480K/year.

Daycare Income Statement Example: Revenue, Costs, and Margins

A daycare income statement example with tuition revenue, CACFP reimbursements, staff cost benchmarks, and a worked P&L for a 50-child childcare center.

Food Truck Income Statement Example: Line Items and Benchmarks

A food truck income statement example with food cost benchmarks, unique line items like commissary and pitch fees, and a worked P&L for a single-truck operation.

Healthcare Income Statement Example: Revenue, Expenses, and Margins

A healthcare income statement example covering net patient revenue, contractual adjustments, expense benchmarks, and operating margin targets for providers.

Healthcare Pro Forma Example: What to Include and How to Build One

A practical healthcare pro forma example — covering revenue projections, payer mix, expense benchmarks, and a worked model for a new medical practice or service line.

Hotel Pro Forma Example: What to Include and How to Build One

A practical hotel pro forma example — covering RevPAR, GOP, undistributed expenses, FF&E reserves, and a worked model for acquisition or development underwriting.