Church Balance Sheet Template

See exactly what your church owns, owes, and holds in trust — a balance sheet built for religious organizations with restricted and unrestricted net assets, building and equipment schedules, and designated fund tracking.

What's Inside This Church Balance Sheet Template

This template includes 4 worksheets, each designed for a specific part of your church financial workflow:

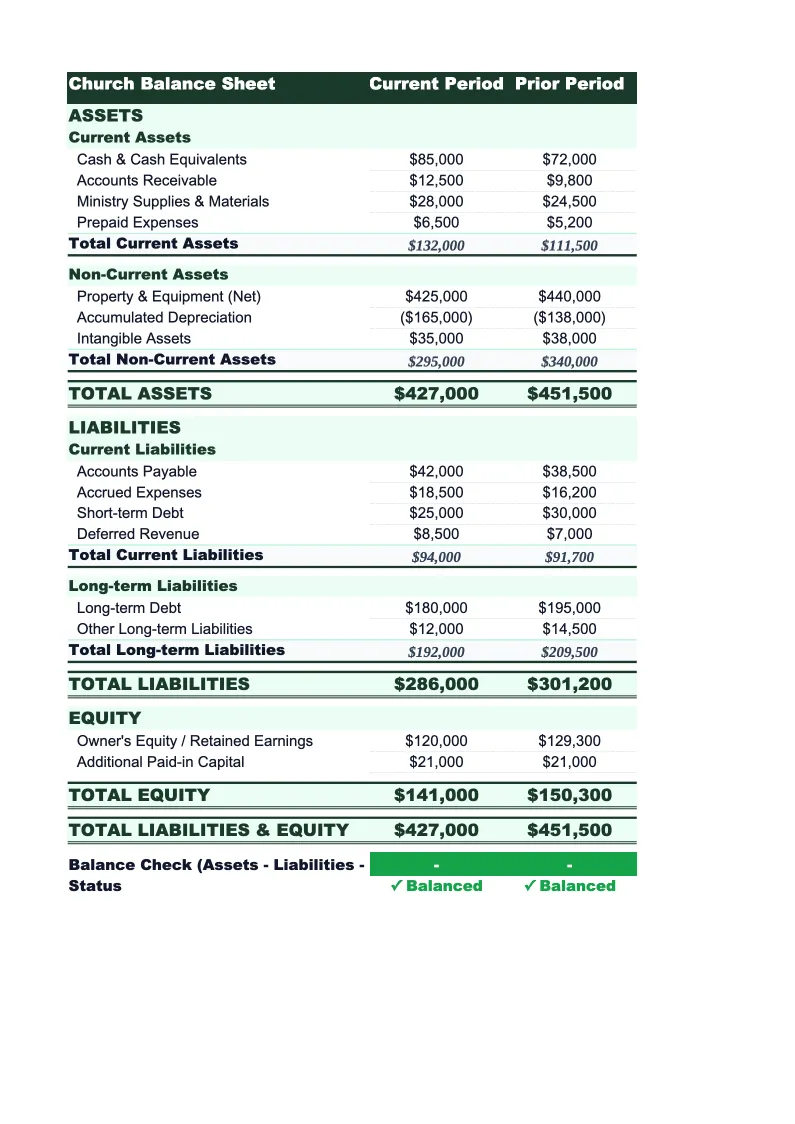

Balance Sheet

The core financial statement organized around church and religious nonprofit accounting conventions.

Net Assets & Funds

A fund register that tracks the opening balance, contributions received, disbursements, and closing balance for each designated fund the church maintains.

Fixed Assets

A fixed-asset register for every significant asset the church owns: land, building, parking lot improvements, HVAC and mechanical systems, sanctuary furnishings and pews, audio-visual and livestream equipment, musical instruments, computers and office technology, kitchen equipment, and vehicles.

Period Comparison

A side-by-side comparison of two balance sheet dates, typically the current fiscal year-end versus the prior year-end or the same quarter year-over-year.

Church Balance Sheet Template Features

- Net assets split into without donor restrictions and with donor restrictions categories following nonprofit accounting standards

- Designated fund register tracks opening balance, contributions, disbursements, and closing balance for each ministry fund

- Fixed asset register with depreciation schedules for buildings, AV equipment, vehicles, and donated assets

- Deferred revenue line for prepaid facility rentals and school tuition deposits

- Accounting equation check — automatically flags any imbalance between total assets and liabilities plus net assets

- Period-over-period comparison for annual congregational reporting, denomination filings, and grant applications

How to Use This Church Balance Sheet Spreadsheet

Start with the Fixed Assets sheet before entering anything else. Work through your church's list of owned property and equipment: land and building (recorded at original cost or appraised value at time of gift), major HVAC and mechanical systems, sanctuary furnishings, audio-visual equipment, instruments, vehicles, and office technology. For each item, enter the description, purchase or gift date, original cost or fair market value, and estimated useful life. The sheet calculates accumulated depreciation and net book value automatically, producing category totals that flow into the balance sheet. If your church has received donated assets — a common occurrence — record them at the fair market value on the date of the gift and flag them in the donated column.

Next, complete the Net Assets & Funds sheet. List every fund your church maintains — general operations, building and capital, benevolence, missions, youth, endowment — and enter the opening balance and any activity during the period. Categorize each fund as without donor restrictions or with donor restrictions based on whether the funds can be used at board discretion or are tied to a donor's specific intent. Then fill in the balance sheet: pull cash from your bank statements, receivables from any outstanding rental or tuition invoices, payables from vendor bills, and your mortgage balance from the most recent loan statement. The fund sheet totals will populate the net assets section of the balance sheet automatically.

15 minutes from download to your first church balance sheet

Download the template, enter your funds and property, and see your church's complete financial position — assets, liabilities, restricted funds, and net assets included.

Why Every Church Needs a Balance Sheet Template

Most churches track their checkbook and present a monthly income-and-expense report to the board — but far fewer maintain a proper balance sheet. The income statement tells you whether giving covered expenses last month; the balance sheet tells you whether the church is in a financially stable position overall. How much is in the building fund versus available for general operations? Is the mortgage being paid down? Are net assets growing year over year? Is there enough in reserve to cover two months of payroll if giving drops in the summer? These questions can only be answered by a balance sheet, and churches that can't answer them are making financial decisions based on incomplete information.

Church balance sheets have two features that distinguish them from for-profit businesses. The first is the net assets structure: instead of owner's equity, churches report net assets split between without donor restrictions and with donor restrictions. This distinction matters because a church with $200,000 in the bank might actually have very limited financial flexibility — if $150,000 is in a capital campaign fund designated by donors for a new building, only $50,000 is available for general operations. Misclassifying restricted funds as unrestricted — or simply not tracking the distinction — is one of the most common financial management failures in smaller churches, and it can create real legal and relational problems when restricted gifts are used for other purposes. The second feature is donated assets: churches regularly receive property, vehicles, and equipment as gifts, which must be recorded at fair market value on the date of the gift.

Church Industry at a Glance

Financial templates built for churches and religious organizations — facility rentals, ceremony fees, staff payroll, and ministry budgets.

Revenue Drivers

- Tithes and weekly offerings

- Facility rental income

- Special offerings (Christmas, Easter)

- School and childcare tuition

- Cemetery and memorial service fees

Key Cost Categories

- Personnel and housing allowance

- Facilities and occupancy

- Worship and ministry programs

- Missions and benevolence

- Administration and software

- Debt service

Typical Margins

Gross: N/A · Net: 0-5% operating surplus

Seasonality

Giving peaks at Christmas and Easter; summer typically sees 10-20% attendance and giving decline. Year-end giving surge in December is common for tax purposes.

Key Performance Indicators

Church Balance Sheet Template FAQ

More Church Templates

Church Budget Template for Excel

$29

Church Budget & Financial Plan Template for Excel

$39

Church Cash Flow Template for Excel

$29

Church Expense Tracker Template for Excel

$29

Church Financial Model Template for Excel

$29

Church Income Statement Template for Excel

$29

Church Invoice Template for Excel

$29

Church KPI Dashboard Template for Excel

$29

Church P&L Template for Excel

$29

Church Pro Forma Template for Excel

$29

Church Project Budget Template for Excel

$29

Church Revenue Forecast Template for Excel

$29

Church Valuation Template for Excel

$29

More Balance Sheet Templates

Church Balance Sheet Template

$29