Nonprofit Budget Example: What to Include and Why

A practical nonprofit budget example covering revenue categories, expense ratios, reserve targets, and the line items watchdogs and funders actually look at.

According to the Nonprofit Finance Fund's 2025 survey of more than 2,200 organizations, 36% of nonprofits ended 2024 with an operating deficit — the highest proportion recorded in ten years of survey data. The same survey found 52% of nonprofits have three months or less of cash on hand.

Budget problems don't announce themselves. They accumulate quietly through overly optimistic revenue projections, underallocated overhead costs, and single-scenario planning until the organization faces a real crisis. The antidote is a budget structured clearly enough that you can see problems before they arrive.

This is what a sound nonprofit budget looks like — and what separates organizations that manage their finances well from those that don't.

How a Nonprofit Budget Is Structured

A nonprofit operating budget has two sides: revenue and expenses. Unlike a for-profit budget, it also distinguishes between restricted and unrestricted funds, and organizes expenses into three functional categories required by IRS Form 990.

Revenue

| Category | What Goes Here |

|---|---|

| Individual donations | One-time gifts, recurring/monthly donors |

| Grants — unrestricted | Foundation and government grants with no programmatic restriction |

| Grants — restricted | Grants designated for specific programs |

| Earned income | Program fees, service contracts, consulting |

| Corporate contributions | Sponsorships, corporate matching |

| Special events | Gala revenue, fundraising events (net of direct costs) |

| Investment income | Interest, dividends, endowment draws |

| Membership dues | If applicable |

The most common budgeting mistake on the revenue side is including grants and gifts that aren't yet confirmed. A sound revenue budget only includes funds with a realistic probability of being received. Unrestricted revenue is especially valuable because it can cover any expense category — restricted funds can only be spent as the donor or grantor specifies.

Expenses — Functional Categories

Form 990 requires nonprofit expenses to be classified into three functions:

Program Services — Direct costs of delivering the mission: staff time spent on programs, client services, program supplies, and direct service delivery costs.

Management & General (M&G) — Organizational infrastructure: executive leadership, finance, HR, IT systems, legal, and accounting. These costs benefit the entire organization but can't be attributed to a specific program.

Fundraising — Donor outreach, grant writing, events, direct mail, and the staff time spent on development activities.

Most expenses (especially salaries) need to be allocated across these three categories based on actual time spent. A program director who splits time between running programs and writing grant reports allocates that salary proportionally. Our nonprofit income statement example shows how these functional allocations appear on the Statement of Activities.

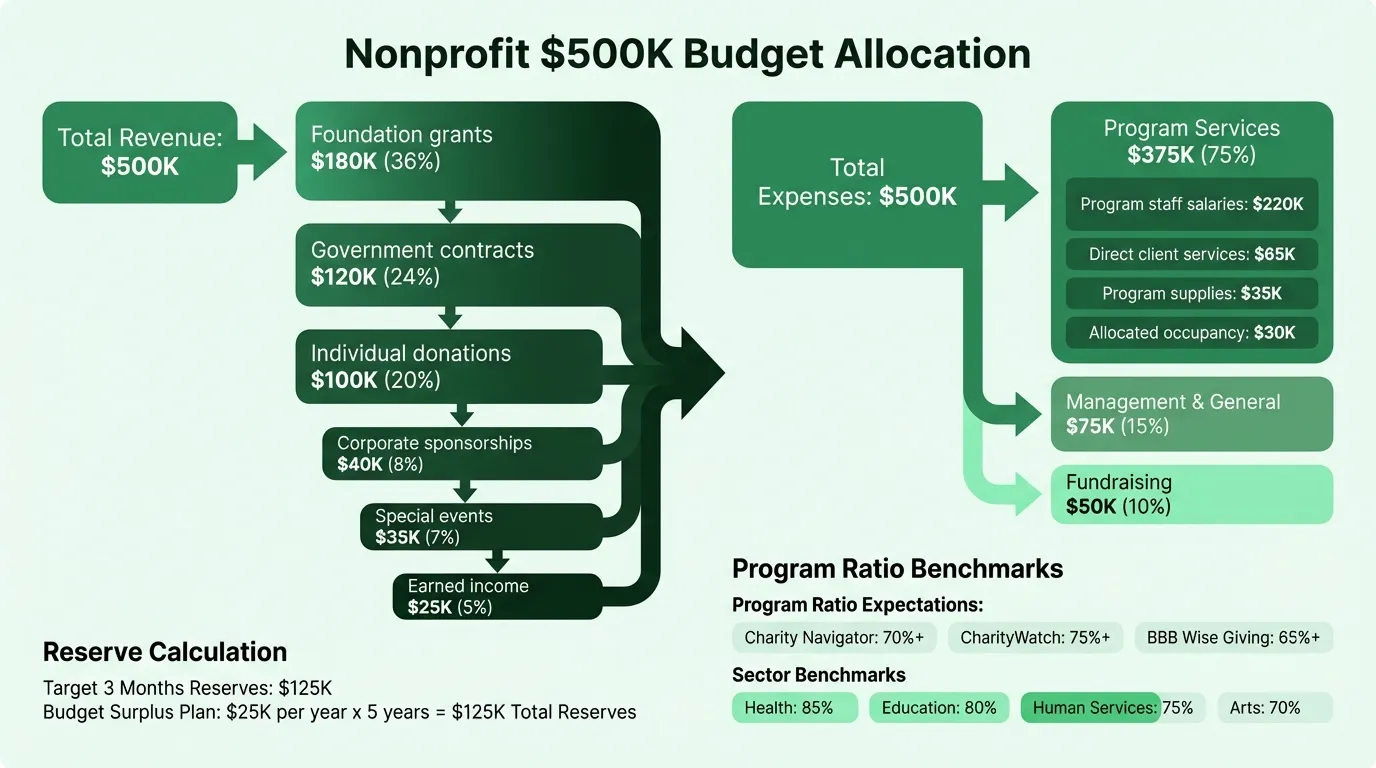

Example: What a $500,000 Nonprofit Budget Looks Like

Here's a realistic example for a human services organization with a $500,000 annual budget:

Revenue

| Source | Amount | % of Total |

|---|---|---|

| Foundation grants (restricted) | $180,000 | 36% |

| Government contracts | $120,000 | 24% |

| Individual donations | $100,000 | 20% |

| Corporate sponsorships | $40,000 | 8% |

| Special events (net) | $35,000 | 7% |

| Earned income / fees | $25,000 | 5% |

| Total Revenue | $500,000 |

Expenses by Function

| Function | Amount | % of Total |

|---|---|---|

| Program Services | $375,000 | 75% |

| Management & General | $75,000 | 15% |

| Fundraising | $50,000 | 10% |

| Total Expenses | $500,000 |

Planned surplus: $0 — but this example should actually budget a small surplus of $15,000–$25,000 to build reserves. More on that below.

Program Expenses Detail

| Line Item | Amount |

|---|---|

| Program staff salaries & benefits | $220,000 |

| Direct client services | $65,000 |

| Program supplies & materials | $35,000 |

| Allocated occupancy (program share) | $30,000 |

| Allocated technology (program share) | $15,000 |

| Program travel | $10,000 |

| Total Program | $375,000 |

Management & General Detail

| Line Item | Amount |

|---|---|

| Executive director (M&G share) | $30,000 |

| Finance staff & accounting | $20,000 |

| Insurance | $8,000 |

| Technology (M&G share) | $7,000 |

| Professional services (audit, legal) | $10,000 |

| Total M&G | $75,000 |

What Watchdogs and Funders Actually Look At

Three major charity watchdogs publish standards for expense allocation. Knowing these helps you structure your budget for both financial health and donor confidence.

Charity Navigator gives full marks to organizations spending 70% or more of total expenses on program services. It removed administrative expense ratio as a standalone metric from its rating system in 2023, but program ratio remains a key factor.

CharityWatch sets the bar at 75% or more going to programs, with fundraising costs no higher than $0.25 per dollar raised.

BBB Wise Giving Alliance recommends at least 65% of total expenses go to program activities.

These ratios are useful benchmarks, not optimization targets. Deliberately underfunding overhead to hit a ratio number leads to the "nonprofit starvation cycle" — underpaying staff, deferring technology investments, and skipping the financial systems that keep the organization functional. Research shows that $1 of overhead spending can increase revenue by $3.45. GuideStar, Charity Navigator, and BBB Wise Giving Alliance jointly published a letter urging donors to move away from overhead ratios as a primary measure of effectiveness.

Typical program ratios by sector, per PBMares:

| Sector | Program | M&G | Fundraising |

|---|---|---|---|

| Health | 85% | 7% | 8% |

| Education & Research | 80% | 10% | 10% |

| Environmental & Animal | 78% | 12% | 10% |

| Human Services | 75% | 12% | 13% |

| Arts & Culture | 70% | 15% | 15% |

Need a ready-made budget template for your nonprofit?

Download a pre-built spreadsheet with industry-specific categories, formulas, and formatting.

The Reserve Line That Most Budgets Are Missing

The Nonprofit Finance Fund's 2025 survey found 52% of nonprofits have three months or less of cash. The standard target is 3–6 months of operating expenses in unrestricted reserves.

Most organizations in that 52% are there because they never budgeted for reserve-building. If the budget hits zero and the plan is to break even, there's no mechanism for reserves to grow.

Fix this by treating the operating reserve as a line item expense. If your operating expenses are $500,000 per year and you want to build toward three months of reserves ($125,000), you need to budget a surplus of roughly $25,000 per year for five years. That starts with a budget that intentionally plans a surplus — not a budget built to balance at zero. You can check your current reserve position on the nonprofit balance sheet by comparing unrestricted net assets to monthly expenses.

Budgets for grant-dependent organizations — especially those with significant government funding — need even larger reserves. The NFF's 2025 survey found 84% of nonprofits with government funding expect cuts to that funding in 2025. Organizations without reserves have no runway to adjust.

Common Nonprofit Budget Mistakes

Copying last year's budget. Rolling over the prior year without adjusting for inflation, new programs, or staff changes leaves the budget out of sync with reality before the year even starts. Salaries, utilities, and technology costs all need to be re-evaluated annually.

Only building one scenario. A single budget model leaves the organization exposed. Best practice is to build three: base case (most likely revenue), conservative case (what if one major grant doesn't come through), and an optimistic case. Organizations with government funding in 2025 need a contingency plan specifically for funding cuts.

Overstating revenue. The pressure to "make the numbers work" pulls revenue projections up. Only include grants and gifts you have a realistic basis to expect. If you land additional funding during the year, treat it as a budget revision — don't build it into the original plan to balance the expenses you want to run.

Breaking even as the goal. Break-even budgeting is not conservative — it's a structural problem. It guarantees no reserve-building, no buffer for unexpected costs, and no capacity to adapt when circumstances change.

Underallocating indirect costs to programs. When grant funders ask for a program budget, include a proportionate share of rent, admin staff, and technology. Submitting program budgets that only include direct costs understates the true cost of service delivery and creates structural deficits that compound over time.

Treating the budget as static. A budget reviewed once at the start of the year and not revisited until December is not a management tool. Variance analysis — comparing actuals to budget at least quarterly — is how you catch problems while there's still time to act. Use a nonprofit expense tracker to capture actual spending as it happens, making quarterly variance reviews straightforward.

Restricted vs. Unrestricted: The Allocation Problem

Restricted grants fund specific programs and can't be redirected to cover unexpected shortfalls elsewhere. This creates a real cash management problem: an organization can have plenty of restricted funds on hand while being unable to make payroll because that money can only be spent on program X.

The structural fix is a budget that specifically targets unrestricted revenue growth. Individual donors and corporate sponsors are typically unrestricted. Foundation grants vary — some are entirely restricted, others include an M&G allocation. When negotiating grant budgets, always include indirect cost recovery to offset what the grant draws from shared infrastructure.

Organizations that are heavily grant-dependent with little unrestricted revenue are most vulnerable to the cash flow problems that come from restricted fund imbalances. Our nonprofit accounting guide covers the revenue recognition rules that determine when grant funding hits the books.

Building Your Nonprofit Budget

A Nonprofit Budget Template gives you the structure to work from — revenue by source, expenses by functional category, salary allocation across functions, and reserve tracking built in.

If you're also tracking profitability and net assets, a Nonprofit Balance Sheet Template captures where restricted and unrestricted assets stand at any point in time, and the Nonprofit Income Statement Template tracks revenue and expenses over a period.

The budget is a planning document. The income statement and balance sheet are how you report on what actually happened against that plan. Together they give you — and your board, auditors, and funders — a complete picture of the organization's financial position.

Start the annual budget process in October. That gives the board time to review scenarios, ask questions, and approve before the fiscal year begins. Entering January without an approved budget means operating on assumptions that no one has validated.

Last updated: March 23, 2026

Frequently Asked Questions

Related Articles

Coffee Shop Budget Example: Real Numbers and Benchmarks

A practical coffee shop budget example with real cost benchmarks — covering beverage COGS, labor, rent, equipment maintenance, and the line items most operators underestimate.

Church Budget Example: Categories, Percentages, and What to Include

A practical church budget example with real percentages for staff, facilities, missions, and programs — plus the line items most churches overlook.

Construction Budget Example: Line Items, Percentages, and What to Include

A practical construction budget example covering hard costs, soft costs, overhead allocation, and the line items most contractors underestimate.

Daycare Budget Example: Categories, Benchmarks, and What to Watch

A practical daycare budget example covering revenue sources, expense ratios, occupancy thresholds, and the line items that determine whether a center stays financially viable.

Event Planning Budget Example: Real Numbers for Your Business

A practical event planning budget example covering agency overhead, per-event costs, revenue models, and the benchmarks every planner needs to protect margins.

Hotel Budget Example: Departments, Benchmarks, and Real Numbers

A practical hotel budget example covering the USALI department structure, labor benchmarks, GOP targets, and the line items independent hoteliers most often miss.