Nonprofit Balance Sheet Example: What It Includes and How to Read It

A complete nonprofit balance sheet example with real line items, net asset classifications, and what donors, auditors, and grantors look for when they review it.

A nonprofit's balance sheet is a public document — it appears in your Form 990, which anyone can look up. Donors, grantors, and prospective board members use it to decide whether your organization is financially healthy enough to trust with their support.

Understanding what's on it — and what the numbers actually mean — matters for both internal management and external credibility.

What a Nonprofit Balance Sheet Is Actually Called

Under GAAP, nonprofits use the term Statement of Financial Position rather than "balance sheet." The structure is identical — Assets = Liabilities + Net Assets — but the name reflects the purpose. Nonprofits don't have shareholders earning a return. They hold resources in trust for a mission. "Financial position" signals accountability; "balance sheet" implies ownership.

In practice, "nonprofit balance sheet" is widely understood and acceptable in informal contexts. Audited financial statements, grant applications, and board reporting should use Statement of Financial Position.

How It Differs from a For-Profit Balance Sheet

The foundational difference is one word: net assets replaces equity. Everything else flows from there.

| For-Profit | Nonprofit |

|---|---|

| Balance Sheet | Statement of Financial Position |

| Shareholders' Equity | Net Assets |

| Retained Earnings | Net Assets Without Donor Restrictions |

| N/A | Net Assets With Donor Restrictions |

The other structural difference is the classification of net assets. Under current GAAP (FASB ASC 958, updated by ASU 2016-14 effective for most nonprofits in 2018), nonprofits present exactly two classes of net assets:

- Net assets without donor restrictions — funds the organization can use for any mission-aligned purpose, including operating expenses. Board-designated reserves fall here.

- Net assets with donor restrictions — funds subject to donor-stipulated conditions, either purpose restrictions ("for the after-school program only") or time restrictions ("to be used in fiscal year 2027"), or both. Endowment corpus is permanently restricted.

Before 2018, GAAP used three classes: unrestricted, temporarily restricted, and permanently restricted. Many practitioners still use this older language informally. On audited financials, the two-class presentation is required.

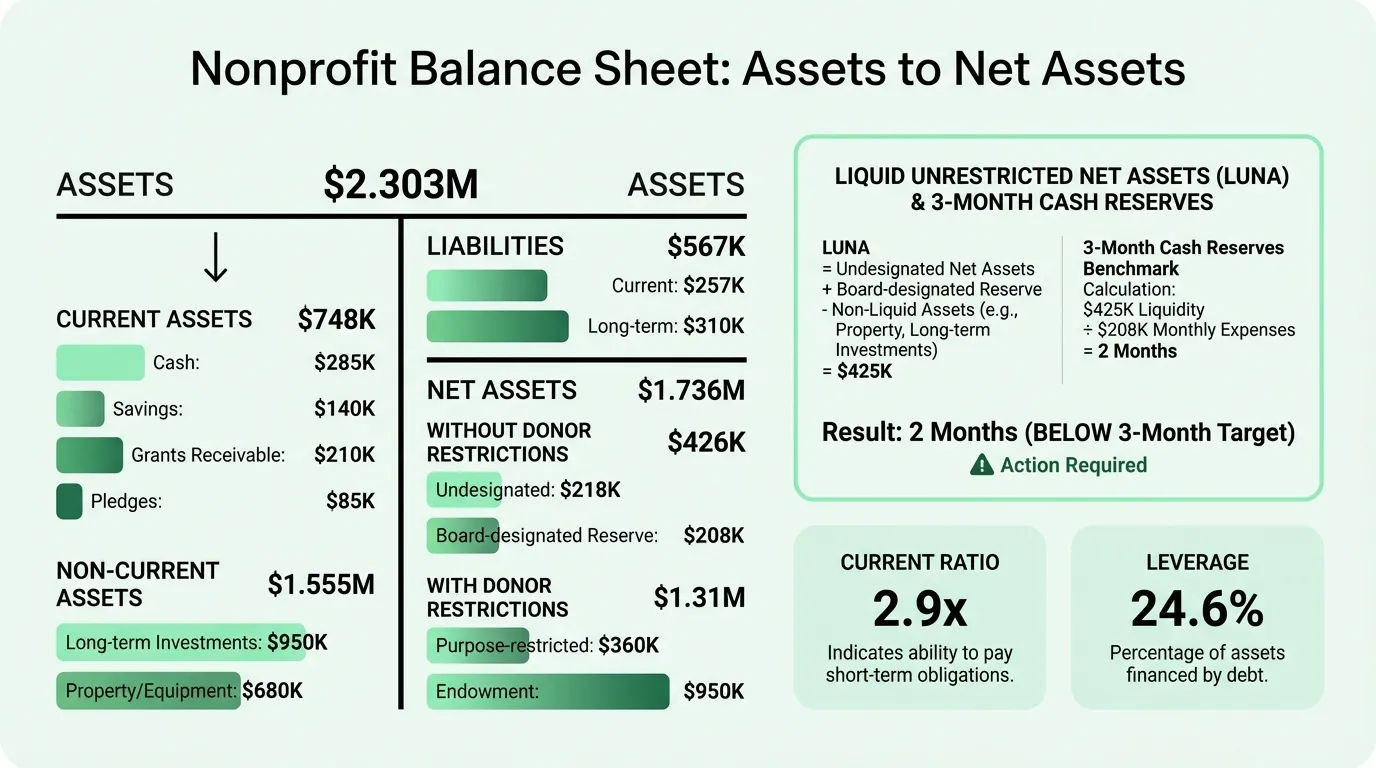

Complete Nonprofit Balance Sheet Example

Here's a representative Statement of Financial Position for a mid-size human services nonprofit with $2.5M in annual expenses:

Assets

Current Assets

| Line Item | Amount |

|---|---|

| Cash and cash equivalents | $285,000 |

| Savings and money market | $140,000 |

| Grants receivable (current) | $210,000 |

| Pledges receivable (current, net of allowance) | $85,000 |

| Prepaid expenses | $28,000 |

| Total Current Assets | $748,000 |

Non-Current Assets

| Line Item | Amount |

|---|---|

| Pledges receivable (long-term) | $120,000 |

| Long-term investments (endowment) | $950,000 |

| Property and equipment | $680,000 |

| Less: accumulated depreciation | ($195,000) |

| Total Non-Current Assets | $1,555,000 |

Total Assets: $2,303,000

Liabilities

Current Liabilities

| Line Item | Amount |

|---|---|

| Accounts payable | $62,000 |

| Accrued salaries and benefits | $78,000 |

| Payroll taxes payable | $18,000 |

| Deferred revenue | $45,000 |

| Refundable advances | $30,000 |

| Current portion of long-term debt | $24,000 |

| Total Current Liabilities | $257,000 |

Long-Term Liabilities

| Line Item | Amount |

|---|---|

| Mortgage payable | $310,000 |

| Total Long-Term Liabilities | $310,000 |

Total Liabilities: $567,000

Net Assets

| Line Item | Amount |

|---|---|

| Without donor restrictions — undesignated | $218,000 |

| Without donor restrictions — board-designated reserve | $208,000 |

| Total Without Donor Restrictions | $426,000 |

| With donor restrictions — purpose-restricted | $360,000 |

| With donor restrictions — endowment (permanent) | $950,000 |

| Total With Donor Restrictions | $1,310,000 |

| Total Net Assets | $1,736,000 |

Total Liabilities and Net Assets: $2,303,000

This organization looks solid on paper. But the analysis below shows what the numbers actually reveal.

Reading the Balance Sheet: What the Numbers Mean

Liquidity: The Number That Actually Matters

Total net assets of $1.7M sounds reassuring. It isn't, by itself.

$950,000 of that is the endowment corpus — permanently restricted and not available for operations. $360,000 is purpose-restricted for specific programs. What's left for general operations is $426,000 in net assets without donor restrictions.

The metric that captures this is Liquid Unrestricted Net Assets (LUNA):

LUNA = Net Assets Without Donor Restrictions − Board-Designated Amounts − Fixed Assets (net)

For this organization: $426,000 − $208,000 (board-designated reserve) − ($680,000 − $195,000) net fixed assets = negative LUNA if calculated strictly against operational liquidity.

A simpler quick check: look at unrestricted cash and liquid assets relative to monthly expenses. This organization has $285,000 in cash + $140,000 in savings = $425,000 liquid. Monthly operating expenses at $2.5M/year ≈ $208,000/month. That's about 2 months of liquidity — below the 3-month recommended minimum. For broader context on fund accounting rules and controls, see our nonprofit accounting guide.

The Nonprofit Finance Fund's 2025 State of the Nonprofit Sector Survey found that 52% of nonprofits have 3 months or less of cash on hand, and 18% have one month or less. Most nonprofits are closer to this situation than the total net assets figure suggests.

The Current Ratio

Current Ratio = Current Assets / Current Liabilities

In this example: $748,000 / $257,000 = 2.9

A ratio above 2.0 is generally considered strong. Above 1.0 is the minimum threshold for financial stability — it means current assets exceed near-term obligations. A current ratio below 1.0 is a warning sign: the organization may struggle to pay its bills within the year.

Deferred Revenue vs. Refundable Advances

These two liability line items are often confused:

Deferred revenue is money received for services not yet delivered — event ticket sales, membership dues paid in advance, or grant funds received before program delivery. It becomes revenue once the organization performs the related activity.

Refundable advances are conditional grants. If the nonprofit fails to meet specific grant conditions (targets, deliverables, allowable expenses), it must return the funds. These stay on the balance sheet as a liability until conditions are substantially met. Misclassifying a refundable advance as revenue is one of the more consequential errors on a nonprofit balance sheet.

Pledges Receivable

Pledges receivable are donor commitments to give in the future. They appear as assets because nonprofits record unconditional pledges when made, not when cash arrives. The balance sheet should show them net of:

- A discount to present value for multi-year pledges

- An allowance for estimated uncollectible pledges

A pledges receivable balance that grows year over year without corresponding cash collection may indicate pledge defaults accumulating — something auditors and finance committee members watch for.

Need a ready-made balance sheet template for your nonprofit?

Download a pre-built spreadsheet with industry-specific categories, formulas, and formatting.

What Auditors Look For

Auditors reviewing a nonprofit balance sheet focus on a few key areas:

Negative unrestricted net assets. If total net assets without donor restrictions is negative, the organization has spent beyond what it has available — often by "borrowing" from restricted funds to cover operating gaps. This is both a financial red flag and potentially a legal violation of donor intent. Reviewing spending against a structured nonprofit budget is the first step toward correcting the imbalance.

Going-concern indicators. Auditors assess whether the organization can continue operations for at least 12 months. Declining cash trends, a current ratio below 1.0, maxed-out or absent lines of credit, and significant operating deficits in consecutive years all trigger this analysis.

Grant compliance. Restricted net assets must be supported by documentation showing that restricted funds are being tracked and spent only on donor-stipulated purposes. Auditors verify that restrictions are properly reflected in the financial statements.

Mandatory liquidity disclosures. Since ASU 2016-14 took effect, audits must include quantitative and qualitative disclosure of financial assets available to meet cash needs within one year. This is not optional even for smaller nonprofits.

Key Ratios for Financial Health

| Ratio | Formula | Strong | Concerning |

|---|---|---|---|

| Current Ratio | Current Assets / Current Liabilities | 2.0+ | Below 1.0 |

| Cash Reserves | Unrestricted Cash / Monthly Expenses | 3–6 months | Under 1 month |

| Leverage | Total Liabilities / Total Assets | Under 30% | Over 50% |

| Program Expense | Program Costs / Total Expenses | 70%+ | Under 60% |

In the example above: leverage ratio = $567,000 / $2,303,000 = 24.6% — a solid position. Program expense ratio lives on the Statement of Activities (the nonprofit income statement equivalent), not the balance sheet itself, but auditors and Charity Navigator use it in conjunction with the balance sheet review.

What the Balance Sheet Doesn't Tell You

Two important gaps:

Operating performance. The balance sheet is a snapshot at a single date. It doesn't show whether this was a surplus year or deficit year, whether revenue is trending up or down, or how expenses are allocated between programs and administration. The Statement of Activities answers those questions.

Cash timing. Positive net assets and positive current ratio don't mean the organization has cash when it needs it. Grants receivable and pledges receivable are assets, but they're not cash. An organization can be technically solvent while unable to make payroll because receivables haven't converted to cash. The Statement of Cash Flows shows actual cash movement in and out. You can model timing gaps with the nonprofit cash flow calculator.

The Nonprofit Balance Sheet Template is structured with these three views in mind — balance sheet position, net asset classification, and the liquidity calculations that matter most to boards and auditors. For a complete financial picture, it pairs with the Nonprofit Budget Template to track planned versus actual spending and the Nonprofit Cash Flow Template to monitor when funds actually arrive and go out.

A Note on Form 990

Your balance sheet is filed publicly as Part X of Form 990. Every major donor, foundation, and journalist can look it up on ProPublica's Nonprofit Explorer or Candid (formerly GuideStar). This isn't just an accounting document — it's an organizational credibility signal.

A balance sheet that shows growing unrestricted net assets, healthy liquidity, and declining leverage tells a story of financial discipline. One that shows negative unrestricted net assets, shrinking cash, and conditional grants sitting in liabilities raises questions — even if program outcomes are strong.

Getting the numbers right and understanding what they communicate is part of responsible nonprofit management. The Nonprofit Balance Sheet Template gives you a starting point that matches auditor expectations and the presentation grantors are used to seeing.

Last updated: March 24, 2026

Frequently Asked Questions

Related Articles

Church Accounting Best Practices: A Practical Guide

How church accounting works — fund accounting, restricted funds, internal controls, financial reports, and the tax rules that catch churches off guard.

Church Balance Sheet Example: A Line-by-Line Breakdown

A complete church balance sheet example with real line items, fund accounting explained, and the benchmarks church boards use to assess financial health.

Construction Accounting: A Practical Guide for Contractors

Construction accounting is different from standard accounting. This guide covers job costing, WIP schedules, retainage, revenue recognition methods, and common mistakes.

Construction Balance Sheet Example: A Line-by-Line Breakdown

A complete construction company balance sheet example with real line items, WIP accounting, retainage, overbilling, and what sureties and lenders look for.

Daycare Balance Sheet Example: Line by Line

A complete daycare balance sheet example with real line items — enrollment deposits, playground equipment, subsidy receivables, and what the numbers mean.

Food Truck Balance Sheet Example: A Line-by-Line Breakdown

A complete food truck balance sheet example with real line items, truck depreciation rules, and what makes a food truck's financials different from a restaurant.