Nonprofit Accounting: A Practical Guide for Organizations

Nonprofit accounting follows different rules than for-profit bookkeeping. This guide covers fund accounting, net assets, the four required statements, Form 990, and common mistakes.

Nonprofit accounting isn't just bookkeeping with a charitable twist. It operates under a different accounting framework, uses different financial statements, and serves a fundamentally different purpose: demonstrating stewardship rather than reporting profit.

Get it wrong, and you risk audit findings, breached grant agreements, donor distrust, and IRS penalties. Get it right, and your financials become a credibility tool — evidence that the organization can be trusted with money.

How Nonprofit Accounting Differs from For-Profit

The governing standard is FASB ASC Topic 958 (Not-for-Profit Entities), which sits within GAAP but adds requirements specific to mission-driven organizations. The differences go deeper than terminology.

| Area | For-Profit | Nonprofit |

|---|---|---|

| Equity section | Shareholders' equity | Net assets (no ownership) |

| Goal of reporting | Profit / shareholder return | Mission impact / stewardship |

| Revenue classification | By type (sales, interest) | By restriction status |

| Expense reporting | By function or department | By nature AND function (dual required) |

| Financial statements | 3 required | 4 required |

| Annual tax filing | Form 1120 / 1065 | Form 990 (public document) |

The most operationally significant difference: every expense must be classified two ways — by what it is (salaries, rent, utilities) and by what it supports (program services, management, fundraising). This dual classification requirement drives the Statement of Functional Expenses, which is unique to nonprofits.

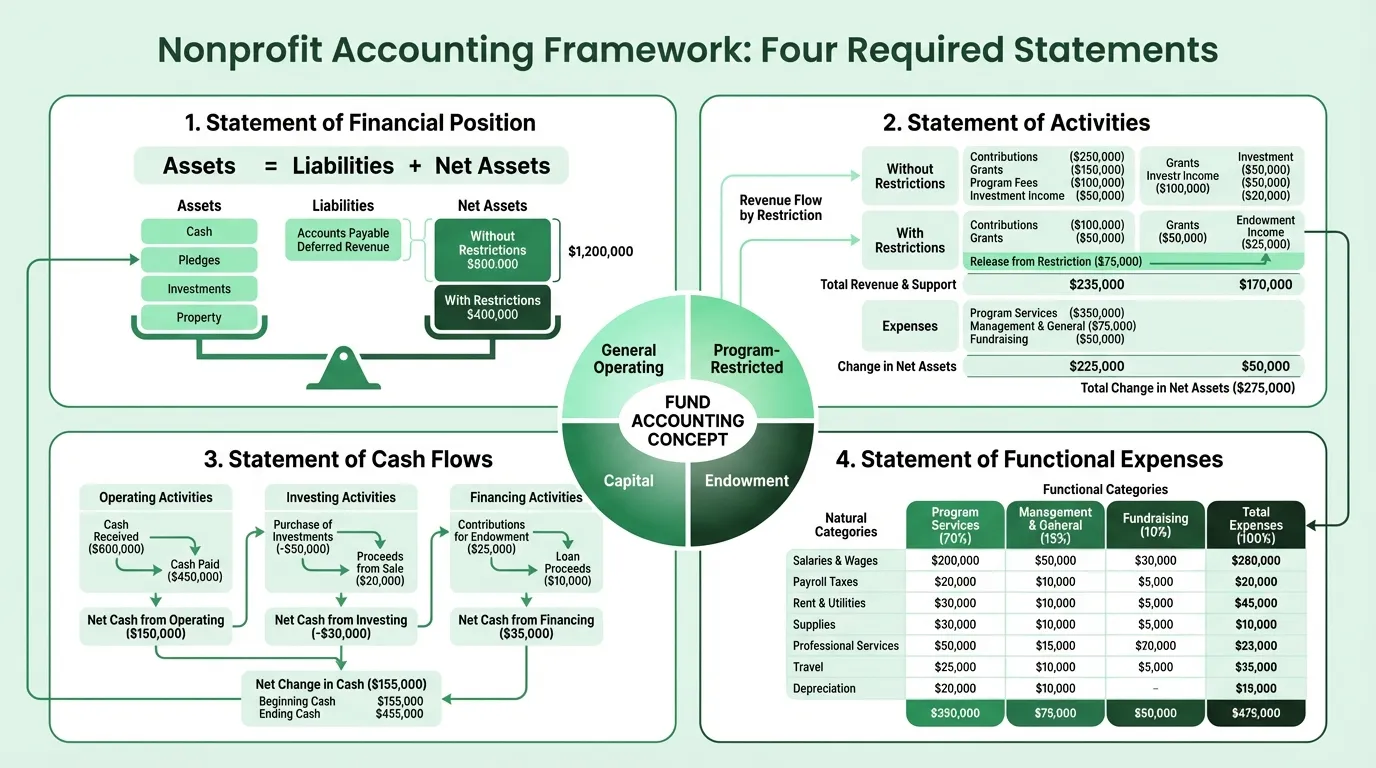

The Four Required Financial Statements

For-profit companies prepare three core financial statements. Nonprofits prepare four.

Statement of Financial Position

This is the nonprofit equivalent of a balance sheet: Assets = Liabilities + Net Assets. The formal name under GAAP reflects its purpose — you're reporting financial stewardship, not shareholder equity.

The key difference from a corporate balance sheet is the net assets section. Instead of equity, you have two classes of net assets:

- Without donor restrictions — funds the board can use at its discretion for any organizational purpose

- With donor restrictions — funds that carry donor-imposed conditions (time, purpose, or both)

See the Nonprofit Balance Sheet Example for a detailed walkthrough of what each line item represents.

Statement of Activities

This is the income statement equivalent. It shows revenue, expenses, and the resulting change in net assets — across both net asset classes.

Revenue is reported by restriction class: a $50,000 government grant with purpose restrictions appears in "with donor restrictions," while unrestricted individual donations appear in "without donor restrictions." When restrictions are satisfied — a program is completed, a time period passes — the amount is "released from restriction" and reclassified as a line item moving between the two columns.

The bottom line isn't "net income" — it's "change in net assets."

Statement of Cash Flows

Largely similar to a for-profit cash flow statement. Operating, investing, and financing activities. The main difference is that donor-restricted contributions intended for long-term purposes (capital gifts, endowment gifts) are reported as financing activities, not operating — because they're not available for general operations.

Statement of Functional Expenses

This is the statement most distinctive to nonprofits. Every expense category appears on two axes:

Natural categories (rows): Salaries and wages, employee benefits, payroll taxes, professional services, supplies, telephone, occupancy, depreciation, etc.

Functional categories (columns): Program services (broken down by program), management and general, fundraising.

The result is a grid showing exactly how every dollar flows. A program director whose time splits 70% to programs and 30% to fundraising appears proportionally in both columns.

This statement is what donors and watchdog organizations scrutinize when evaluating overhead ratios. Charity Navigator benchmarks suggest that effective organizations spend 70% or more of total expenses on program services. The BBB Wise Giving Alliance recommends at least 65%. See how these ratios work in practice in our nonprofit income statement example.

Fund Accounting: The Organizational Logic

Fund accounting is the system underneath the financial statements. Rather than pooling all money into a single ledger, fund accounting maintains separate ledgers for distinct funding streams.

Common fund types:

- General operating fund — unrestricted gifts and earned income available for any purpose

- Restricted program funds — grants or donations designated for specific programs

- Capital fund — gifts restricted for facilities or equipment

- Endowment fund — principal must be maintained in perpetuity; only investment income may be spent

Each fund tracks its own revenues, expenses, and balance. When a restricted grant is received, it goes into its program fund — not the general fund. When expenses are incurred against that grant, they're drawn from the same fund. This makes it straightforward to demonstrate to a grantor that their money was spent as intended.

Without fund accounting, managing multiple grants simultaneously becomes prone to commingling errors. A government grant that requires return of unspent funds needs to be tracked with precision — if it's mixed with general operating funds, you may not know how much was spent against it until an auditor asks. A nonprofit expense tracker helps maintain the fund-level separation that prevents commingling.

Restricted vs. Unrestricted Net Assets

Under ASU 2016-14 (effective for fiscal years beginning after December 15, 2017), FASB simplified net asset classification from three categories to two.

Previous model: Unrestricted / Temporarily Restricted / Permanently Restricted

Current model: Without donor restrictions / With donor restrictions

The new "with donor restrictions" class combines what used to be temporary and permanent restrictions. Under this model, endowment funds (where principal must be maintained forever) and time-restricted gifts (use in a future period) both sit in the same class, with disclosure in the notes explaining the composition.

Important nuance: Board-designated reserves — where the board sets aside funds internally for specific purposes — are classified as without donor restrictions under GAAP. Only external donor-imposed restrictions change the classification. If your board votes to hold 3 months of expenses in reserve, those funds remain unrestricted and the designation must be disclosed separately.

When a restriction is satisfied, the release appears as a line item on the Statement of Activities: "Net assets released from restrictions — satisfaction of program restrictions." This reclassification is how the financial statements track that restricted money was used appropriately.

Need a ready-made p&l template for your nonprofit?

Download a pre-built spreadsheet with industry-specific categories, formulas, and formatting.

Revenue Recognition: Grants and Donations

ASU 2018-08 is the standard that changed how nonprofits recognize grant revenue. Before it, many organizations recognized government grants as revenue when received. After it, the analysis is more rigorous.

Step 1: Is it an exchange transaction or a contribution?

- An exchange (reciprocal) transaction is one where the resource provider receives commensurate value — a government contract to deliver specific services, for instance. Recognize revenue under ASC 606 as performance obligations are satisfied.

- A contribution (nonreciprocal) is where the donor receives no direct benefit. Most private foundation grants fall here. Proceed to Step 2.

Step 2: Is the contribution conditional or unconditional?

- Unconditional contributions have no barriers. Recognize as revenue immediately when received (classified by donor restriction status).

- Conditional contributions require meeting a specific barrier (a matching requirement, completing a deliverable) AND carry a right of return if conditions aren't met. Record as a refundable advance — a liability — until conditions are substantially met, then recognize revenue.

The practical impact: most government grants that look like contributions are now analyzed as either exchange transactions or conditional contributions, which delays revenue recognition until the work is done. This matters for budgeting: grant funding that was previously booked as revenue on receipt now only hits the income statement as the program is delivered.

Form 990: Your Public Financial Statement

Form 990 is the annual federal filing for tax-exempt organizations — and unlike corporate tax returns, it's a public document. Anyone can search your 990 on ProPublica Nonprofit Explorer or Candid.

Filing thresholds:

| Gross Receipts | Total Assets | Form Required |

|---|---|---|

| $50,000 or less | Any | Form 990-N (e-Postcard) |

| Under $200,000 | Under $500,000 | Form 990-EZ |

| $200,000+ OR | $500,000+ | Full Form 990 |

| Private foundations | Any | Form 990-PF |

Filing deadline: 15th day of the 5th month after fiscal year end. For calendar-year filers, that's May 15. A 6-month extension is available.

Key sections on the full 990:

- Part III — Program accomplishments (what you actually did)

- Part VI — Governance (board composition, conflict-of-interest policy, whistleblower policy)

- Part VII — Compensation of officers and highest-paid employees

- Part VIII — Statement of Revenue

- Part IX — Statement of Functional Expenses

The Form 990 is how major donors, grantors, and watchdog organizations evaluate your organization before deciding to give. Having clean, consistent financials that match what appears on your 990 is a credibility signal.

Missed filing penalty: $20 per day (up to $10,500 per year) for smaller organizations; $100 per day (up to $50,000 per year) for larger ones. Three consecutive missed filings triggers automatic revocation of tax-exempt status — which requires a reinstatement application to undo.

Common Nonprofit Accounting Mistakes

Mishandling restricted funds. Spending restricted donations on general operations — even temporarily — violates donor agreements and can trigger repayment demands. The fix is fund accounting with locked-down restricted fund ledgers. See also how restricted funds appear on the Nonprofit Balance Sheet.

Misclassifying functional expenses. Overstating program expenses by dumping administrative or fundraising costs into program categories inflates your program ratio. This is a common audit finding and can result in financial statement restatement. Conversely, failing to allocate shared costs (a manager's salary split across functions) leaves the functional expense statement inaccurate.

Ignoring in-kind contributions. Donated goods, services, and use of facilities must be recorded at fair market value if they would otherwise be purchased. ASU 2020-07 (effective 2022) added enhanced disclosure requirements specifically for contributed nonfinancial assets. Omitting them understates both revenue and expenses.

Misclassifying grants as contributions. A government grant that requires delivering specific services on a defined timeline is often an exchange transaction under ASU 2018-08 — not a contribution. Recognizing it as immediate revenue when it's actually an exchange transaction misstates your financials.

Weak internal controls. One person controlling authorization, recording, and custody of funds is a segregation-of-duties failure auditors flag consistently. At minimum, the person who processes payments shouldn't also reconcile the bank account.

Missing Form 990 deadlines. The penalties are real, and three consecutive misses trigger revocation. Set calendar reminders for 90 days before the deadline so there's time to prepare or request an extension. Keeping a current nonprofit budget makes the 990 preparation process significantly faster.

Forgetting to release restrictions. When grant conditions are satisfied or time periods pass, the release from restriction must be recorded. Failing to do this leaves money sitting in "with donor restrictions" that should be in "without donor restrictions" — overstating restricted net assets and understating available funds.

Setting Up the Books for Nonprofit Accounting

Whether you use QuickBooks Nonprofit, Sage Intacct, or a dedicated nonprofit platform like Aplos, the structural requirements are the same:

Chart of accounts by function. Your expense categories need to support both natural and functional classification. Set up accounts at the intersection of both dimensions (or use classes/dimensions to tag each transaction with a functional category).

Fund or class tracking. For each restricted grant or program, create a separate class, fund, or project code. Every revenue and expense transaction related to that grant should be coded to it.

Net asset accounts by class. Set up separate equity accounts for net assets without donor restrictions and net assets with donor restrictions. Track releases from restriction as journal entries when conditions are met.

Grant tracking schedule. A separate grant tracking spreadsheet — showing each grant, its restrictions, spending to date, balance remaining, and reporting deadlines — is one of the most useful management tools for nonprofits with multiple funders.

The Nonprofit Budget Template and Nonprofit Cash Flow Template are pre-structured for fund-based tracking, with separate columns for restricted and unrestricted funds.

The Three Reports That Drive Nonprofit Financial Management

Statement of Activities tells you whether the organization is sustaining itself — whether total revenue exceeds total expenses, and whether the mix of restricted and unrestricted funding is healthy. A surplus in restricted funds while unrestricted net assets are declining is a warning sign: you have plenty of program money but can't cover overhead.

Statement of Financial Position tells you where you stand at a point in time. Key metrics: months of liquid unrestricted reserves, the ratio of restricted to unrestricted net assets, and whether net assets are growing or shrinking over time. The nonprofit balance sheet example breaks down what each section reveals. You can verify your cash position quickly with the nonprofit cash flow calculator.

Statement of Functional Expenses is what your board, auditors, and major donors use to evaluate whether your overhead is defensible. The goal isn't minimizing overhead — it's being able to explain why the overhead you have is necessary to deliver the mission. Present financial reports to your board with Deckary.

Nonprofit accounting has more moving parts than for-profit bookkeeping, but the underlying discipline is the same: accurate records, timely reporting, and financial controls that protect the organization. The reward is trust — from donors, grantors, the IRS, and the communities you serve.

Last updated: March 24, 2026

Frequently Asked Questions

Related Articles

Church Accounting Best Practices: A Practical Guide

How church accounting works — fund accounting, restricted funds, internal controls, financial reports, and the tax rules that catch churches off guard.

Church Balance Sheet Example: A Line-by-Line Breakdown

A complete church balance sheet example with real line items, fund accounting explained, and the benchmarks church boards use to assess financial health.

Construction Accounting: A Practical Guide for Contractors

Construction accounting is different from standard accounting. This guide covers job costing, WIP schedules, retainage, revenue recognition methods, and common mistakes.

Construction Balance Sheet Example: A Line-by-Line Breakdown

A complete construction company balance sheet example with real line items, WIP accounting, retainage, overbilling, and what sureties and lenders look for.

Daycare Balance Sheet Example: Line by Line

A complete daycare balance sheet example with real line items — enrollment deposits, playground equipment, subsidy receivables, and what the numbers mean.

Food Truck Balance Sheet Example: A Line-by-Line Breakdown

A complete food truck balance sheet example with real line items, truck depreciation rules, and what makes a food truck's financials different from a restaurant.