Nonprofit Balance Sheet Template

See exactly what your nonprofit owns, owes, and holds in net assets — a balance sheet built for fund accounting, grant reporting, and donor restriction tracking.

What's Inside This Nonprofit Balance Sheet Template

This template includes 4 worksheets, each designed for a specific part of your nonprofit financial workflow:

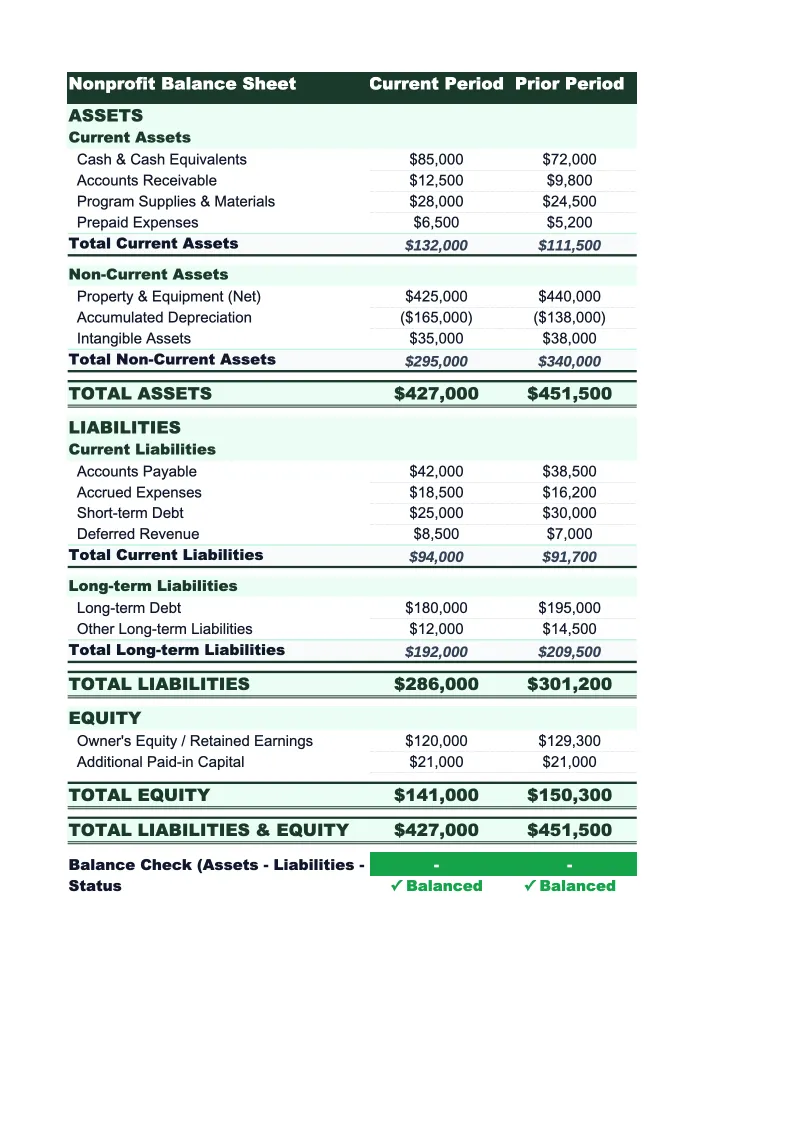

Statement of Financial Position

The core balance sheet organized in the format auditors, grant officers, and boards expect for nonprofits.

Net Assets Detail

A supporting worksheet that breaks down your net assets by restriction type before they roll up to the main statement.

Grants & Pledges Receivable

A dedicated schedule for tracking amounts owed to your organization — both grants awarded but not yet received and multi-year pledges from donors.

Period Comparison

A side-by-side view comparing two statement dates — typically fiscal year-end to prior year-end, or quarter-end to prior quarter-end.

Nonprofit Balance Sheet Template Features

- Net assets split by donor restriction status (ASC 958 compliant)

- Grants and pledges receivable schedule with aging and restriction tracking

- Deferred revenue line items for unearned grant funds

- Endowment and long-term investment asset classification

- Accounting equation check — flags any imbalance automatically

- Period-over-period comparison for board reports and grant renewals

How to Use This Nonprofit Balance Sheet Spreadsheet

Download the file and open it in Excel or Google Sheets — no plugins or macros required. Start with the Grants & Pledges Receivable sheet: list every grant that's been awarded but not yet received, along with any multi-year donor pledges. Enter the funder name, amount, expected payment date, and whether the funds are restricted. This step is worth doing first because receivables often represent a significant portion of your assets, and getting them right sets a solid foundation for the rest of the balance sheet.

Next, work through the Statement of Financial Position sheet itself. Enter your current cash balances across all bank accounts (operating, savings, and any restricted cash held separately). Add accrued liabilities — unpaid wages, vendor invoices, and any grant funds received that haven't yet been spent (those go in deferred revenue, not net assets). Then move to the Net Assets Detail sheet to break down your unrestricted reserves, board-designated funds, temporarily restricted grants, and any endowment principal. The main sheet pulls from this detail automatically and checks that everything balances.

15 minutes from download to your first statement of financial position

Download the template, enter your accounts, and see your nonprofit's full financial position — assets, liabilities, net assets by restriction class, and period-over-period trends.

Why Every Nonprofit Needs a Statement of Financial Position

Most nonprofits focus intensely on their income statement — how much came in, how much went out, and whether the programs ran within budget. The balance sheet gets less attention, but it's the document that reveals whether an organization is financially stable or one bad grant cycle away from a crisis. A nonprofit can run a balanced budget every year while still depleting its operating reserves, accumulating debt, or spending down restricted funds faster than it's replenishing them. The statement of financial position is how you see those patterns before they become emergencies.

Nonprofit balance sheets have two features that make them structurally different from for-profit equivalents. First, equity is called net assets, and it must be split by donor restriction status. Unrestricted (now called without donor restrictions under ASC 958) is what you can actually use for operations. Restricted funds look like net assets but can only be spent on specific programs or after specific dates — they don't provide liquidity. Auditors, sophisticated funders, and board finance committees will always look at this split first when assessing financial health. The second distinctive feature is deferred revenue: grant funds received before the conditions are met are a liability, not income. Organizations that treat advance grant payments as unrestricted income can overstate their financial position significantly.

Nonprofit Industry at a Glance

Financial templates built for nonprofit organizations — from community foundations to service-delivery charities. Pre-loaded with fund accounting categories, grant tracking, and program expense ratios.

Revenue Drivers

- Grants (government & foundation)

- Individual donations

- Program fees

- Membership dues

- Special events

- Corporate sponsorships

Key Cost Categories

- Personnel & benefits

- Program expenses

- Administrative overhead

- Fundraising costs

- Occupancy

- Equipment & technology

Typical Margins

Gross: N/A · Net: 2-5% operating surplus

Seasonality

Grant cycles create Q1 and Q4 revenue spikes; year-end giving peaks in December. Fiscal years often run July–June rather than calendar year.

Key Performance Indicators

Nonprofit Balance Sheet Template FAQ

More Nonprofit Templates

Nonprofit Budget Template for Excel

$29

Nonprofit Business Plan Template for Excel

$39

Nonprofit Cash Flow Template for Excel

$29

Nonprofit Expense Tracker Template for Excel

$29

Nonprofit Financial Model Template for Excel

$29

Nonprofit Income Statement Template for Excel

$29

Nonprofit Invoice Template for Excel

$29

Nonprofit KPI Dashboard Template for Excel

$29

Nonprofit P&L Template for Excel

$29

Nonprofit Pro Forma Template for Excel

$29

Nonprofit Project Budget Template for Excel

$29

Nonprofit Sales Forecast Template for Excel

$29

Nonprofit Valuation Template for Excel

$29

More Balance Sheet Templates

Nonprofit Balance Sheet Template

$29