Construction Pro Forma Example: What to Include and How to Build One

A practical construction pro forma example — covering hard costs, soft costs, contingency, and return metrics for project financing and investor presentations.

A construction pro forma is the financial model you build before any money moves — before permits are pulled, before a crew is mobilized, before the loan closes. It answers one question: given the projected costs, financing, and revenue, does this project generate an acceptable return?

Lenders require it. Investors expect it. And smart developers use it long before either of those conversations happen, to decide whether a project is worth pursuing at all.

This post walks through what a construction pro forma includes, the benchmarks that inform the inputs, and a worked example for a ground-up commercial project.

Pro Forma vs. Budget vs. Estimate

Three documents that often get conflated:

| Document | What It Covers | Primary Use |

|---|---|---|

| Cost estimate | Line-item cost breakdown | Pre-bid planning |

| Construction budget | Total spend tracking | Cost control during build |

| Pro forma | Costs, revenue, financing, returns | Lender packages, investor presentations, go/no-go decisions |

The budget answers "what will this cost?" The pro forma answers "will this project make money, and by how much?" A complete pro forma contains the budget as one of its inputs — but it also projects revenue, structures the financing, calculates carry costs, and produces return metrics.

When You Need a Construction Pro Forma

Securing a construction loan. Banks and private lenders require a full pro forma before approving a construction loan. They use it to verify DSCR (debt service coverage ratio), confirm that the loan-to-cost ratio fits their program, and stress-test the project under cost overrun scenarios. A loan request without a credible pro forma doesn't get past the initial review.

Raising equity capital. If you're bringing in outside investors — high-net-worth individuals, family offices, or real estate syndicates — they evaluate deals based on levered IRR and equity multiple. These numbers come from the pro forma.

Evaluating feasibility before predevelopment spend. Entitlements, architectural plans, and environmental studies can cost $50,000–$300,000 before a shovel hits the ground. A preliminary pro forma run before those costs are committed tells you whether the project clears your return hurdle — and whether those predevelopment costs are worth spending.

Bidding on contracts. General contractors run internal pro formas before submitting bids to verify that the contract price, given anticipated costs and overhead, produces an acceptable margin. If the bid-level margin falls below target, the pro forma flags it before submission.

What a Construction Pro Forma Includes

1. Revenue / Sales Projections

What the completed project generates:

- For-sale projects (single-family homes, condos, commercial buildings for sale): projected sales price per unit or per square foot, based on market comparables

- For-rent projects (multifamily, commercial leases): projected rents, lease-up timeline, stabilized occupancy rate

- Absorption schedule: how long it takes to sell or lease all units once construction ends

The absorption schedule matters enormously for IRR calculations. A project that takes 18 months to lease up has very different returns than one that reaches stabilization in 6 months — even if total revenue is identical. Every month of vacancy adds to holding costs and delays the equity return.

2. Hard Costs

Hard costs are direct construction costs — the physical work. They typically represent 70–80% of total project cost:

- Site work, demolition, and grading

- Foundation and structure

- Framing and enclosure (roofing, windows, exterior)

- Mechanical, electrical, plumbing (MEP)

- Interior finishes and fixtures

- Landscaping and site improvements

Hard costs should be sourced from a detailed contractor estimate or recent bid. Using square-footage averages from national databases is a starting point for feasibility modeling, but bids are required for lender packages. Our construction budget example shows how to break down hard costs by category with realistic percentages.

3. Soft Costs

Soft costs are indirect project costs — everything that isn't physical construction. They run 15–30% of total project cost and are the most commonly underestimated line item in early-stage pro formas:

- Architecture and engineering fees

- Permits and entitlements

- Environmental studies and inspections

- Developer fee

- Legal and accounting fees

- Marketing and sales costs

- Property taxes during construction

Omitting or low-balling soft costs is one of the fastest ways to lose credibility with lenders. A pro forma that shows $0 for permits on a commercial project signals that the developer hasn't done the work.

4. Financing Costs

- Construction loan origination fees (typically 1–2% of loan amount)

- Construction loan interest carry — the interest that accrues daily during the build period

- Loan extension fees (if the project takes longer than the initial loan term)

- Lender-required reserves and escrows

The interest carry line deserves particular attention. It's a function of loan amount, interest rate, and time. A $5M construction loan at 8% annual interest carries at roughly $33,000 per month. A project that runs 4 months over schedule adds $132,000 in interest expense that wasn't in the original pro forma.

5. Contingency

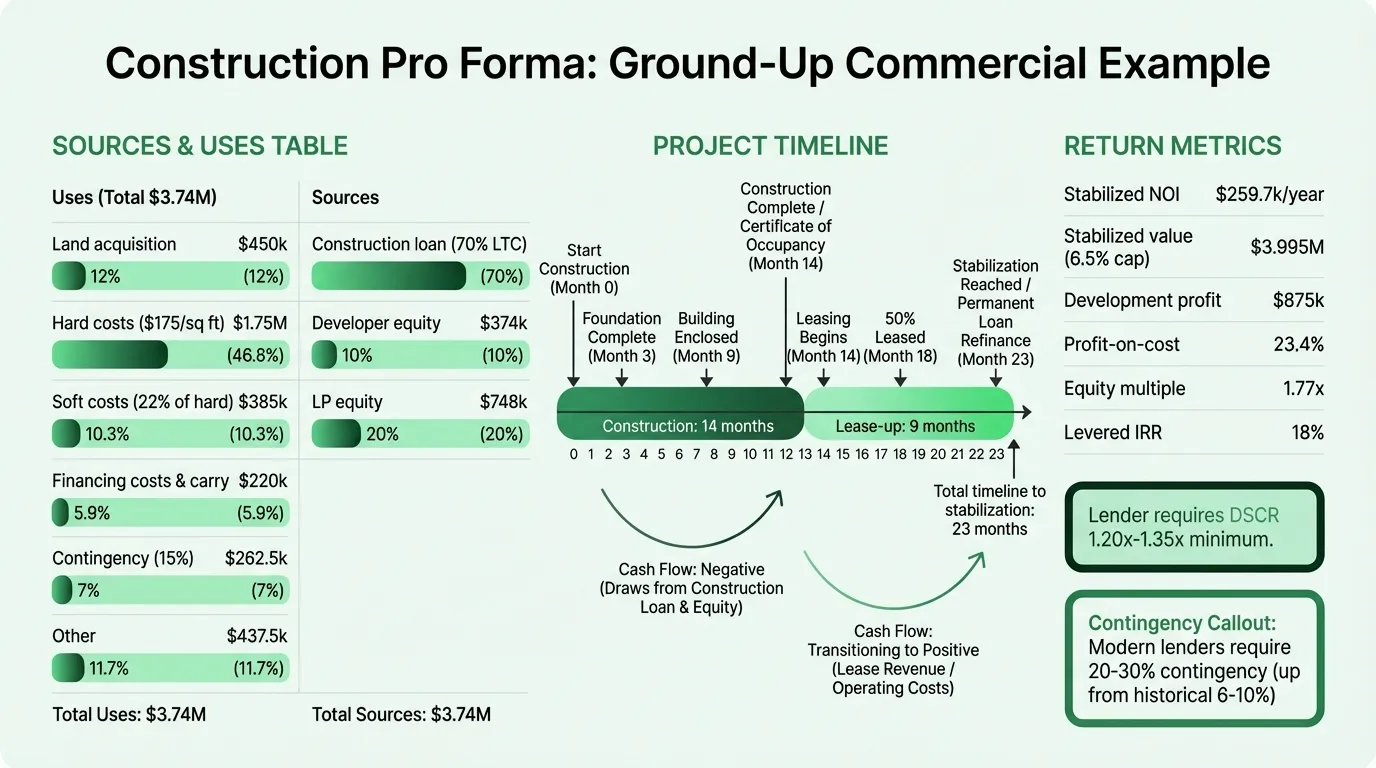

Contingency covers cost overruns, scope changes, and unexpected conditions. According to Partner Engineering and Science's 2024 industry analysis, many institutional lenders now require 20–30% contingency on ground-up construction loans over $1M — up significantly from the historical 6–10% standard.

This shift reflects the reality that 85–90% of construction projects experience some form of cost overrun. Projects in the single-digit contingency range are increasingly viewed by lenders as underfunded, not efficient.

6. Sources and Uses

The sources and uses table shows where project capital comes from and how it's deployed:

Sources (how it's funded):

- Senior construction loan

- Mezzanine debt (if applicable)

- Developer / GP equity

- Limited partner / investor equity

Uses (where capital goes):

- Land or acquisition costs

- Hard costs

- Soft costs

- Financing costs

- Contingency

Sources must equal uses. Lenders review this table to confirm the project is fully capitalized and that equity is funded before debt begins drawing.

7. Return Metrics

| Metric | What It Measures | Typical Threshold |

|---|---|---|

| Profit-on-cost | Development profit ÷ total cost | 15–25%+ for ground-up development |

| Unlevered IRR | Return on all capital, ignoring financing | Project-quality benchmark |

| Levered IRR | Return on equity after debt service | 15–25% for ground-up development |

| Equity multiple | Total equity returned ÷ equity invested | 1.5x–2.5x over a 2–5 year hold |

| DSCR | Operating income ÷ annual debt payments | 1.20x–1.35x (lender minimum) |

Worked Example: Ground-Up Commercial Building

This example is a 10,000 sq ft commercial building — a simplified model to illustrate the pro forma structure.

Project Assumptions

- 10,000 rentable sq ft, suburban market

- Target rent: $28/sq ft/year ($23,333/month at stabilization)

- Lease-up period: 9 months to full occupancy

- Hold: stabilize and sell at a 6.5% cap rate

- Construction period: 14 months

- Construction loan: 70% LTC at 8.5% interest

Sources and Uses

| Uses | Amount | % of Total |

|---|---|---|

| Land acquisition | $450,000 | 12.0% |

| Hard costs ($175/sq ft) | $1,750,000 | 46.8% |

| Soft costs (22% of hard) | $385,000 | 10.3% |

| Financing costs (interest carry + fees) | $220,000 | 5.9% |

| Contingency (15% of hard costs) | $262,500 | 7.0% |

| Lease-up carry | $155,000 | 4.1% |

| Developer fee | $187,000 | 5.0% |

| Reserves | $130,500 | 3.5% |

| Total Project Cost | $3,740,000 | 100% |

| Sources | Amount | % of Total |

|---|---|---|

| Construction loan (70% LTC) | $2,618,000 | 70% |

| Developer equity | $374,000 | 10% |

| LP equity | $748,000 | 20% |

| Total | $3,740,000 | 100% |

Revenue and Returns

| Metric | Value |

|---|---|

| Stabilized NOI ($28/sq ft, 93% occupancy) | $259,700/year |

| Stabilized value at 6.5% cap | $3,995,000 |

| Less loan payoff | ($2,618,000) |

| Net equity proceeds | $1,377,000 |

| Total equity invested | $1,122,000 |

| Development profit | $875,000 |

| Profit-on-cost | 23.4% |

| Equity multiple | ~1.77x |

| Levered IRR (23-month total timeline) | ~18% |

This project clears the 15% levered IRR threshold and produces a profit-on-cost above 20% — both typical targets for ground-up commercial development. Run your own project numbers through the construction profit margin calculator to check whether your contractor margins support the pro forma assumptions.

Need a ready-made pro forma template for your construction?

Download a pre-built spreadsheet with industry-specific categories, formulas, and formatting.

Industry Benchmarks to Use as Inputs

According to the CFMA's 2024 Construction Financial Benchmarker (based on FY2023 data from 1,290 companies):

- Average net income before taxes across all contractors: 6.3%

- Best-in-class (top 25%): 11.9%

- Average SG&A as a percentage of revenue: 11.8%

The NAHB's 2025 Cost of Doing Business Study reported average gross margin for residential builders at 20.7% — the highest level since 2006.

These benchmarks are most useful when evaluating contractor-managed construction projects (where the developer is also the GC) or when building internal pro formas for bid-level decisions. Our construction pricing guide covers how these margin benchmarks translate into actual labor rates and overhead recovery. For development pro formas, the critical benchmarks are contingency percentage, LTC ratios, and DSCR — not margin percentages.

The Three-Scenario Model

A credible construction pro forma shows three scenarios, not one:

Base case: Your realistic expectation. Use conservative cost inputs (not the low bid) and market-rate absorption assumptions.

Upside case: If construction finishes on schedule, costs run 5% below budget, and absorption completes in 6 months instead of 9. What does the levered IRR look like?

Downside case: If costs run 10–15% over budget, the project takes 4 extra months, and lease-up takes 18 months. Does the project still service its debt? Does equity still recover its principal?

Lenders run their own downside scenarios on every deal they underwrite. A pro forma that only shows the base case will be stress-tested by the lender anyway — it's better to show you've already done that work and understand the risk.

What Makes a Construction Pro Forma Credible

Soft costs are fully loaded. Pro formas that show minimal soft costs signal either inexperience or intentional optimism. Permits, entitlements, and professional fees add up — typically 15–30% of hard costs.

Interest carry is calculated on actual timeline. A flat "financing costs" number without a monthly interest calculation suggests the developer hasn't modeled what a timeline slip costs. Show the math: loan balance × monthly rate × construction months. The construction cash flow example illustrates how these timing gaps compound during the build period.

Contingency reflects the project type. Ground-up construction in an infill urban location warrants more contingency than a simple metal building on a cleared suburban site. The contingency line should reflect the project's complexity.

Revenue assumptions have market support. Projected rents or sale prices should reference named comparable properties or a recent market study — not just "market rate."

The downside scenario still survives. Not profitably, necessarily — but without wiping out investor equity or defaulting on the construction loan.

The Construction Pro Forma Template is built for lender packages and investor presentations, with a sources and uses table, monthly interest carry calculation, and scenario modeling built in.

How the Pro Forma Fits the Broader Financial Picture

The pro forma is the pre-construction planning document. Once the project is underway, it becomes the benchmark you measure against.

Each month, compare actual costs to pro forma estimates. If hard costs are tracking 8% above budget at month four, you have time to adjust — reduce soft cost overruns, negotiate with subs, or request a contingency draw — before the overrun compounds.

After the project closes, the Construction Income Statement Template covers ongoing financial reporting. The Construction Budget Template handles cost tracking during the build. The three documents work together: the pro forma sets the plan, the budget tracks execution, and the income statement reports results.

A construction project without a pro forma is a project where no one knows what the return should be — which means no one knows when the project is off track until it's too late to fix it. Present projections to stakeholders with Deckary.

Last updated: March 23, 2026

Frequently Asked Questions

Related Articles

Coffee Shop Income Statement Example: Revenue, Costs, and Margins

A coffee shop income statement example with beverage cost benchmarks, labor targets, prime cost rules, and a worked P&L for an independent café doing $480K/year.

Daycare Income Statement Example: Revenue, Costs, and Margins

A daycare income statement example with tuition revenue, CACFP reimbursements, staff cost benchmarks, and a worked P&L for a 50-child childcare center.

Food Truck Income Statement Example: Line Items and Benchmarks

A food truck income statement example with food cost benchmarks, unique line items like commissary and pitch fees, and a worked P&L for a single-truck operation.

Healthcare Income Statement Example: Revenue, Expenses, and Margins

A healthcare income statement example covering net patient revenue, contractual adjustments, expense benchmarks, and operating margin targets for providers.

Healthcare Pro Forma Example: What to Include and How to Build One

A practical healthcare pro forma example — covering revenue projections, payer mix, expense benchmarks, and a worked model for a new medical practice or service line.

Hotel Pro Forma Example: What to Include and How to Build One

A practical hotel pro forma example — covering RevPAR, GOP, undistributed expenses, FF&E reserves, and a worked model for acquisition or development underwriting.