Consulting Valuation Template

Value your consulting practice using seller's discretionary earnings multiples, a revenue approach, client concentration analysis, and an owner-dependency scorecard — built around how consulting firms actually sell.

What's Inside This Consulting Business Valuation Template

This template includes 6 worksheets, each designed for a specific part of your consulting financial workflow:

Business Inputs

The data foundation for the entire model.

Revenue Multiple Approach

A revenue-based screening method for establishing a broad value range before digging into earnings.

SDE Multiple Approach

Seller's Discretionary Earnings is the primary income-based valuation method for owner-operated consulting businesses and other professional services firms.

Client Concentration Analysis

Client concentration is the factor buyers scrutinize most carefully in consulting transactions, and this sheet quantifies the risk.

Owner Dependency Scorecard

A structured scoring model for the factors that most directly determine how much of a consulting practice's value is transferable to a new owner.

Valuation Summary

A single-page output consolidating all three valuation approaches into one view across conservative, base, and optimistic scenarios.

Consulting Business Valuation Template Features

- Revenue multiple calculation benchmarked to consulting firm and professional services transactions with retainer vs. project adjustments

- SDE normalization with full owner compensation add-back and a multiple selection matrix for consulting-specific value drivers

- Client concentration analysis tracking top-10 client revenue share, contract transferability, and multi-year retention history

- Owner dependency scorecard scoring eight transferability factors including client loyalty, methodology documentation, and recurring revenue

- Transition scenario comparison showing asset sale, earnout structure, and full going-concern scenarios in the Valuation Summary

- Three-scenario output with SDE sensitivity table and revenue multiple range showing the full negotiation band

How to Use This Consulting Business Valuation Spreadsheet

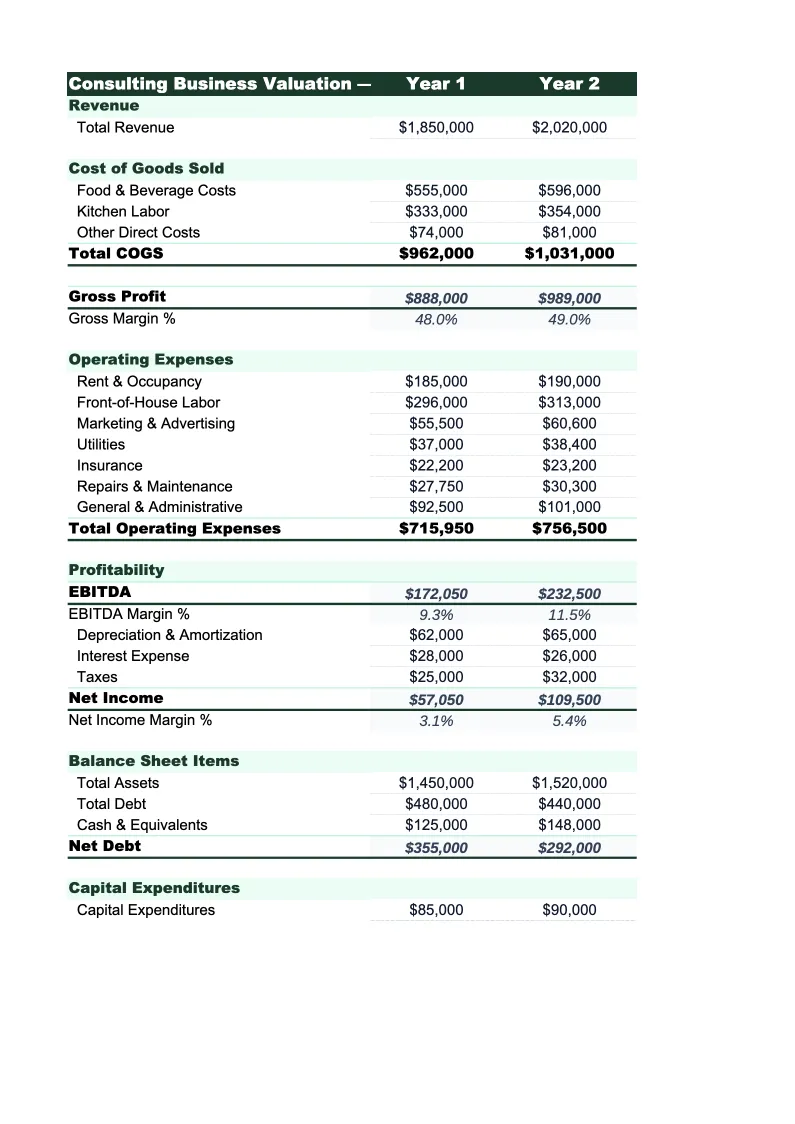

Start with the Business Inputs sheet. Pull your trailing twelve-month revenue by engagement type from your accounting software — most consulting firms use QuickBooks, FreshBooks, or a simple spreadsheet to track hourly billing, retainer invoices, and project fees separately. Break out owner compensation completely: salary, profit distributions, and any business expenses that are genuinely personal (personal vehicle, travel that isn't client-billable, entertainment). You'll also need operational data: total billable hours in the trailing twelve months, effective hourly rate, number of active clients, how many are on retainers versus project-by-project, and headcount of any consultants or contractors who work on client engagements beyond the owner. If your accounting mixes subcontractor costs into a single line, separate them — buyers look at the gross margin after contractor costs as a proxy for how scalable and defensible the practice's profitability is.

Work through the Revenue Multiple and SDE Multiple sheets, then complete the Client Concentration Analysis and Owner Dependency Scorecard. The client concentration section is where most consulting firms encounter an uncomfortable truth: a significant portion of their revenue is concentrated in two or three clients with whom the owner has a personal relationship, and that concentration directly compresses the SDE multiple a buyer will accept. Document each major client relationship honestly — whether the engagement is governed by a formal master service agreement with the firm entity, whether it's a personal relationship that would likely follow the owner if they went elsewhere, and the length of the relationship. These factors determine how a buyer structures the offer and whether they'll require an earnout. The Owner Dependency Scorecard scores the factors that a buyer or a business broker will walk through with you during diligence — understanding your score in advance lets you identify specific improvements before going to market.

Know what your consulting practice is worth before you sell

Enter your revenue, SDE, client concentration data, and operational metrics — and get a defensible valuation range with the SDE approach, client analysis, and owner dependency scorecard that buyers will use to make their offer.

How Consulting Firms Are Valued When They Sell

Consulting business valuations come down to one question faster than almost any other business type: does the practice's revenue follow the owner, or does it follow the firm? For a solo consultant whose clients chose them because of their specific expertise, network, and reputation — which describes the majority of high-earning independent consultants — the honest answer is that most of the revenue follows the person. Buyers understand this, and they price it into offers: the practice may be generating $500,000 per year, but if a buyer could lose 60% of that revenue when the founder leaves, they're not paying for $500,000 in revenue. They're paying for the equipment, the IP, and whatever portion of the client base can genuinely be retained under new ownership. This is why most solo consulting practices sell at relatively modest multiples or as structured earnouts rather than clean acquisitions.

The factors that move a consulting valuation toward the high end of the range are the same ones that reduce the owner's operational centrality. Recurring retainer revenue is the most important: clients on monthly or quarterly retainers who have contracted with the firm for ongoing advisory work represent revenue that a new owner can inherit with a reasonable expectation of continuity, particularly if the retainer covers strategy, compliance, or oversight functions that the client needs regardless of who specifically delivers the work. Employed consultants who carry their own client portfolios independently — not just support the owner on projects, but manage relationships and run engagements from kickoff to delivery without the owner's involvement — are the second most important factor. Proprietary methodologies, assessment tools, or training programs that clients pay for as products rather than as pure consulting hours create revenue that is genuinely IP-based and transfers cleanly with a sale. And a client base diversified across industries and geographies, without any single client representing more than 15–20% of total revenue, reduces the concentration risk that depresses multiples more than almost any other single factor.

Consulting Industry at a Glance

Financial templates built for consulting firms and independent consultants. Pre-loaded with billing structures for hourly, retainer, and project-based engagements.

Revenue Drivers

- Hourly billing

- Monthly retainers

- Fixed-fee project work

- Expense reimbursements

Key Cost Categories

- Contractor/subcontractor fees

- Travel and accommodation

- Software and tools

- Professional development

- Marketing and business development

- Office and administrative overhead

Typical Margins

Gross: 50-80% · Net: 20-40%

Seasonality

Q1 tends to be slow as clients finalize budgets; Q4 often sees a surge in project closes. Summer can dip for firms serving corporate clients.

Key Performance Indicators

Consulting Business Valuation FAQ

More Consulting Templates

Consulting Balance Sheet Template for Excel

$29

Consulting Budget Template for Excel

$29

Consulting Business Plan Template for Excel

$39

Consulting Cash Flow Template for Excel

$29

Consulting Expense Tracker Template for Excel

$29

Consulting Financial Model Template for Excel

$29

Consulting Income Statement Template for Excel

$29

Consulting Invoice Template for Excel

$29

Consulting KPI Dashboard Template for Excel

$29

Consulting P&L Template for Excel

$29

Consulting Pro Forma Template for Excel

$29

Consulting Project Budget Template for Excel

$29

Consulting Sales Forecast Template for Excel

$29

Consulting Valuation Template

$29