Accounting Firm Valuation Template

Value your accounting or CPA firm using seller's discretionary earnings multiples, a revenue approach, client book portability analysis, and a practitioner dependency scorecard — built around how accounting practices actually change hands.

What's Inside This Accounting Firm Valuation Template

This template includes 6 worksheets, each designed for a specific part of your accounting firm financial workflow:

Business Inputs

The data entry foundation for the entire model.

Revenue Multiple Approach

A top-down valuation method that sets a broad value range using trailing twelve-month gross revenue.

SDE Multiple Approach

Seller's Discretionary Earnings is the primary income-based valuation method for solo practitioners and small CPA firms where one owner-operator drives the majority of client relationships and technical work.

Client Book Analysis

The core risk assessment for any accounting practice transaction.

Practitioner Dependency Scorecard

A structured scoring model that evaluates how much of the practice's revenue and client goodwill is transferable independent of the selling practitioner.

Valuation Summary

A single-page output consolidating the revenue multiple and SDE multiple approaches into one view across conservative, base, and optimistic scenarios.

Accounting Firm Valuation Template Features

- Revenue multiple calculation benchmarked to CPA and accounting firm transactions with recurring, business-service, and individual tax revenue adjustments

- SDE normalization with full owner compensation add-back, realization and collection rate adjustments, and a multiple selection matrix for accounting practice value drivers

- Client book portability analysis tracking top-15 client revenue concentration, engagement letter structure, and service type classification

- Practitioner dependency scorecard scoring eight transferability factors including staff depth, recurring revenue percentage, and documented workflow systems

- Transition structure comparison showing direct asset purchase, earnout structure, and going-concern merger scenarios with client retention implications

- Three-scenario valuation output with SDE sensitivity table showing the full negotiation band from 1.5x to 5.0x

How to Use This Accounting Firm Valuation Spreadsheet

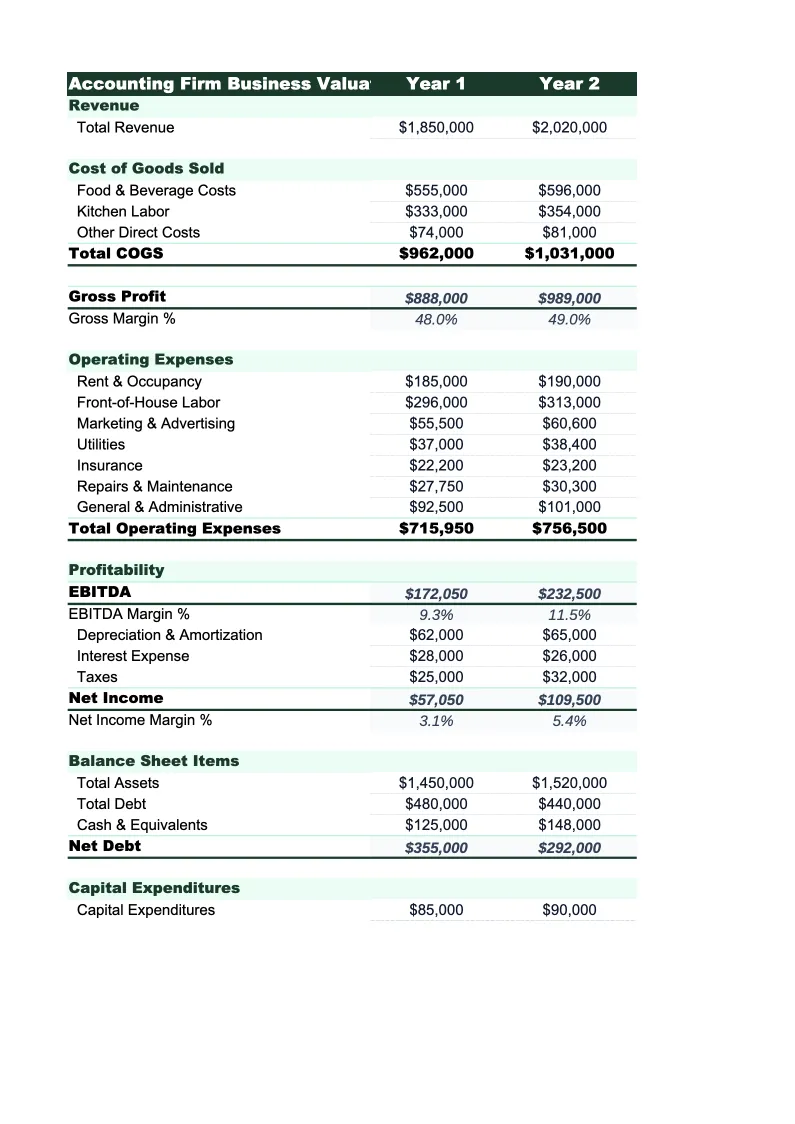

Start with the Business Inputs sheet. Pull trailing twelve-month revenue from your practice management software or accounting system — most CPA firms track revenue across tax preparation, bookkeeping, payroll, advisory, and audit in separate billing categories, and keeping them separated matters because each service type commands a different valuation premium. Enter the owner's total compensation completely: salary or guaranteed draws, profit distributions, and any personal expenses run through the practice. Operational metrics are equally important: total billable hours per professional, your practice's blended utilization rate (billable hours divided by total available hours — healthy practices typically run 65–75%), realization rate (what you actually collect relative to standard billing rates — most well-run practices achieve 85–95%), and collection rate (typically 92–98% for practices with strong engagement letter and invoicing discipline). Active client count, the number of clients under recurring monthly or annual engagement agreements, and the headcount of professional staff capable of independently managing client engagements all flow into the downstream sheets.

Work through the Revenue Multiple and SDE Multiple sheets, then complete the Client Book Analysis and Practitioner Dependency Scorecard. The client book analysis is where most solo practitioners encounter the core tension in accounting practice sales: a large proportion of client relationships — particularly individual tax clients — exist because the client specifically trusts the owner-practitioner, not the firm entity. Document each major client relationship honestly: whether the engagement is governed by a signed firm-level engagement letter, whether the client came as a personal referral to the owner, and how long the engagement has been active. Long-tenured clients often develop strong personal loyalty to their preparer that is difficult to estimate in advance. The Practitioner Dependency Scorecard then scores the factors a buyer or practice broker will evaluate during diligence. Working through it in advance highlights the specific improvements — converting month-to-month client arrangements into formal engagement letters, training staff to handle client communications and questions independently, or moving client data into a centralized practice management platform — that would move your practice up the multiple range before going to market.

Know what your accounting practice is worth before you sell

Enter your billings by service type, SDE, client book data, and operational metrics — and get a defensible valuation range with the SDE approach, portability analysis, and practitioner dependency scorecard that buyers will use to make their offer.

How Accounting Firms Are Valued When They Sell

Accounting firm valuations are driven by one central question: how much of the practice's revenue will follow the selling practitioner out the door, and how much will stay with the firm under new ownership. Solo CPA practices where every client relationship runs through the principal — where clients call the owner's personal cell, receive deliverables signed by the owner's name, and came to the firm through the owner's personal referral network — face the highest attrition risk in a transition and command the lowest multiples on the revenue multiple scale. The industry standard for accounting practice sales acknowledges this directly: most transactions include a transition period of 12–24 months where the selling practitioner continues working with clients in some capacity, specifically to support retention. The transaction price is often structured to partially depend on whether clients actually stay — earnout provisions tied to client billing retention at 12 and 24 months post-close are standard in professional practice acquisitions, and they reflect the buyer's recognition that what they are purchasing is an introduction to clients, not a guaranteed revenue stream.

The characteristics that push an accounting firm toward the upper end of the valuation range reflect one underlying dynamic: revenue that persists independent of the selling practitioner. Monthly bookkeeping, payroll processing, and CAS retainer arrangements with business clients are the most transferable revenue in any CPA practice because they are governed by a firm-level engagement letter with a business entity, the work is typically performed by staff rather than the principal, and the client's primary measure of satisfaction is accuracy and timeliness — which a competent successor can deliver. Annual individual tax preparation, by contrast, is the most owner-dependent revenue category in an accounting practice: individual clients chose their specific preparer for reasons of trust, comfort, and personal referral, and attrition rates of 20–35% in the 12 months following a principal transition are common for primarily tax-preparation practices. Practices with employed CPAs and enrolled agents who carry client portfolios independently are more transferable than solo operations because the client base is already distributed across multiple professional relationships rather than concentrated on the principal alone.

Accounting Firm Industry at a Glance

Financial templates built for accounting firms and CPA practices — from solo practitioners to multi-partner firms. Pre-loaded with billable hour tracking, realization rate calculations, and service categories that reflect how accounting firms actually bill.

Revenue Drivers

- Tax preparation and planning

- Audit and assurance

- Bookkeeping and client accounting services (CAS)

- Advisory and fractional CFO services

- Payroll processing

Key Cost Categories

- Professional staff salaries and benefits

- Administrative staff

- Occupancy and rent

- Technology and software (tax, practice management)

- Malpractice (E&O) insurance

- Marketing and business development

- CPE and professional development

- Subcontractors and offshore staff

Typical Margins

Gross: 50-65% · Net: 20-35%

Seasonality

Heavy busy season January through April 15; secondary crunch in September through October 15 for extensions. Slowest months are July and August.

Key Performance Indicators

Accounting Firm Valuation FAQ

More Accounting Firm Templates

Accounting Firm Balance Sheet Template for Excel

$29

Accounting Firm Budget Template for Excel

$29

Accounting Firm Business Plan Template for Excel

$39

Accounting Firm Cash Flow Template for Excel

$29

Accounting Firm Expense Tracker Template for Excel

$29

Accounting Firm Financial Model Template for Excel

$29

Accounting Firm Income Statement Template for Excel

$29

Accounting Firm Invoice Template for Excel

$29

Accounting Firm KPI Dashboard Template for Excel

$29

Accounting Firm P&L Template for Excel

$29

Accounting Firm Pro Forma Template for Excel

$29

Accounting Firm Project Budget Template for Excel

$29

Accounting Firm Sales Forecast Template for Excel

$29

More Valuation Templates

Accounting Firm Valuation Template

$29