Church Valuation Template

Assess a congregation's financial health, property value, and long-term sustainability using giving trend analysis, reserve scoring, property assessment, and a structured framework for mergers, closures, and denominational reviews.

What's Inside This Church Valuation Template

This template includes 5 worksheets, each designed for a specific part of your church financial workflow:

Church Inputs

The data entry foundation for the entire assessment.

Financial Health Scorecard

A structured assessment of the congregation's financial condition across six dimensions that denominational leaders, lenders, merger partners, and church boards use to evaluate organizational health and sustainability.

Property & Asset Assessment

A systematic inventory and assessment of the congregation's real and personal property assets — typically the largest component of a church's balance sheet and the primary asset in any merger, closure, or property transaction.

Giving Sustainability Analysis

A forward-looking assessment of whether the congregation's current giving base can sustain its existing financial commitments, and what the giving base looks like relative to attendance and demographic trends.

Merger & Transition Summary

A single-page output consolidating the financial health score, property assessment, giving sustainability analysis, and key operational metrics into a structured framework for merger conversations, denominational assessments, pastoral transitions, or property decisions.

Church Valuation Template Features

- Financial health scorecard across six dimensions — operating reserve, personnel cost ratio, facilities cost ratio, giving per attender, debt service coverage, and giving trend — benchmarked to church financial consulting standards

- Property and asset assessment comparing book value to estimated fair market value for sanctuary, parsonage, educational buildings, and major equipment with unrealized appreciation calculation

- Giving sustainability analysis tracking giving unit count, per-household giving trends, and giving concentration across top 10, 25, and 50 giving households

- Three-scenario giving sustainability projection modeling flat, 3% decline, and 5% decline trajectories against current expense structure to show financial runway

- Merger and transition summary separating financial position, property position, ministry value, and transition risk as distinct components for consolidation conversations

- Property disposition scenario calculating net proceeds from potential property sale after mortgage payoff, transaction costs, and denominational recapture provisions

How to Use This Church Valuation Spreadsheet

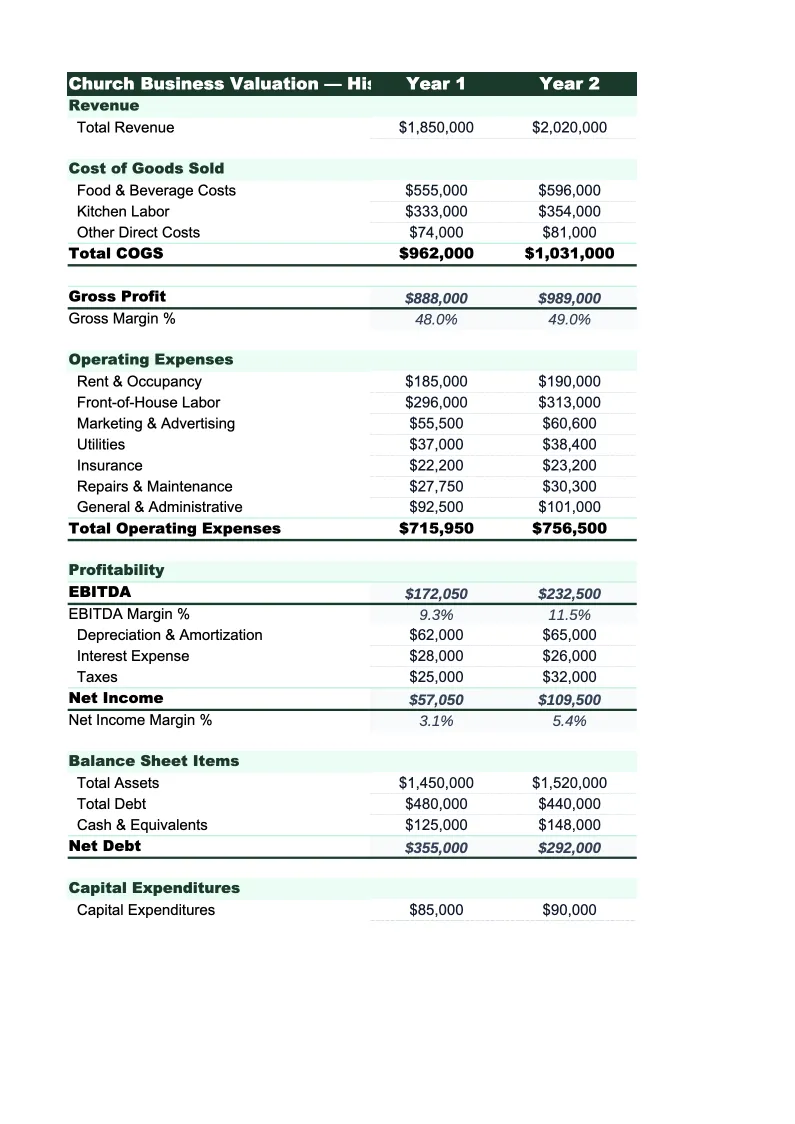

Start with the Church Inputs sheet. Pull trailing twelve-month revenue data from your church management software or accounting system — most churches track giving, facility income, and special offerings in separate accounts, and keeping them separated here matters because each source carries a different predictability profile. Enter balance sheet figures including unrestricted operating funds, all designated fund balances by purpose, endowment assets if any, and outstanding mortgage or loan balances. The real property section in the Property Assessment sheet requires current book value from your depreciation schedule and an estimated current market value — your county assessor's website shows the assessed value, which is typically 80–90% of market value in most jurisdictions and gives you a reasonable starting estimate. Operational metrics including average weekly attendance and giving unit count are essential inputs; pull those from your church management system or attendance records.

Complete the Financial Health Scorecard and Giving Sustainability Analysis before your next board meeting, strategic planning session, or any conversation with denominational leadership. The scorecard will surface the ratios — personnel cost percentage, facilities cost percentage, and operating reserve — that church financial consultants and denominational bodies use to assess congregation health. Pay particular attention to the giving concentration analysis: many congregations are surprised to find that 30–40% of their giving comes from 5–10 households, which creates meaningful vulnerability to deaths, relocations, and life-stage giving changes in that core group. The sustainability projection scenarios are sobering for congregations experiencing gradual giving decline — the model shows exactly how many years of financial runway remain at the current trajectory, which forces a realistic conversation about whether the path is sustainable.

Know your congregation's financial health before the next board meeting

Enter your giving data, expense structure, property values, and fund balances — and get a complete picture of operating reserve depth, giving sustainability, and what your church is actually worth.

How Churches Are Valued for Mergers and Sustainability Planning

Valuing a church is not the same as valuing a for-profit business, but churches are financially assessed more often than most congregations realize. Denominational bodies conduct financial reviews when churches request loans for building projects, when they fall behind on denominational assessments, or when they are candidates for merger or closure. Lenders evaluate financial health when refinancing a mortgage or financing a building expansion. Boards conduct internal assessments when a long-tenured pastor retires and the congregation needs to evaluate whether current commitments are sustainable under new leadership. Real estate decisions — whether to sell a building and relocate, lease unused space, or pursue a renovation — require a clear picture of what the property is worth and what the congregation's balance sheet actually looks like. In all of these contexts, the same core metrics drive the assessment: operating reserve, giving per attender, personnel and facilities cost ratios, debt service coverage, and the concentration and trajectory of the giving base.

The financial characteristics that define a healthy, sustainable congregation are consistent across denominations and sizes, even though the absolute numbers vary widely. An operating reserve of 3–6 months of expenses is the most widely cited benchmark — congregations below 2 months are one bad year of giving away from a cash crisis, and bad years happen: attendance drops during pastoral transitions, major donors relocate, facilities require unexpected capital expenditures. Personnel costs below 55% of total budget leave enough margin for facilities maintenance, ministry programming, and reserve accumulation; congregations that push personnel above 60% consistently find themselves deferring maintenance and cutting ministry to cover payroll. Giving per attender is the most useful comparative metric because it normalizes for congregation size: a church of 150 attenders giving $180,000 annually ($1,200 per attender) is in a different financial position than one giving $120,000 ($800 per attender), even though the giving amounts are not dramatically different. Understanding where your congregation sits relative to these benchmarks — and whether the trajectory is improving or declining — is the starting point for any sustainability conversation.

Church Industry at a Glance

Financial templates built for churches and religious organizations — facility rentals, ceremony fees, staff payroll, and ministry budgets.

Revenue Drivers

- Tithes and weekly offerings

- Facility rental income

- Special offerings (Christmas, Easter)

- School and childcare tuition

- Cemetery and memorial service fees

Key Cost Categories

- Personnel and housing allowance

- Facilities and occupancy

- Worship and ministry programs

- Missions and benevolence

- Administration and software

- Debt service

Typical Margins

Gross: N/A · Net: 0-5% operating surplus

Seasonality

Giving peaks at Christmas and Easter; summer typically sees 10-20% attendance and giving decline. Year-end giving surge in December is common for tax purposes.

Key Performance Indicators

Church Valuation Template FAQ

More Church Templates

Church Balance Sheet Template for Excel

$29

Church Budget Template for Excel

$29

Church Budget & Financial Plan Template for Excel

$39

Church Cash Flow Template for Excel

$29

Church Expense Tracker Template for Excel

$29

Church Financial Model Template for Excel

$29

Church Income Statement Template for Excel

$29

Church Invoice Template for Excel

$29

Church KPI Dashboard Template for Excel

$29

Church P&L Template for Excel

$29

Church Pro Forma Template for Excel

$29

Church Project Budget Template for Excel

$29

Church Revenue Forecast Template for Excel

$29

More Valuation Templates

Church Valuation Template

$29