Law Firm Valuation Template

Value your law firm using seller's discretionary earnings multiples, a revenue approach, book of business portability analysis, and an attorney dependency scorecard — built around how legal practices actually change hands.

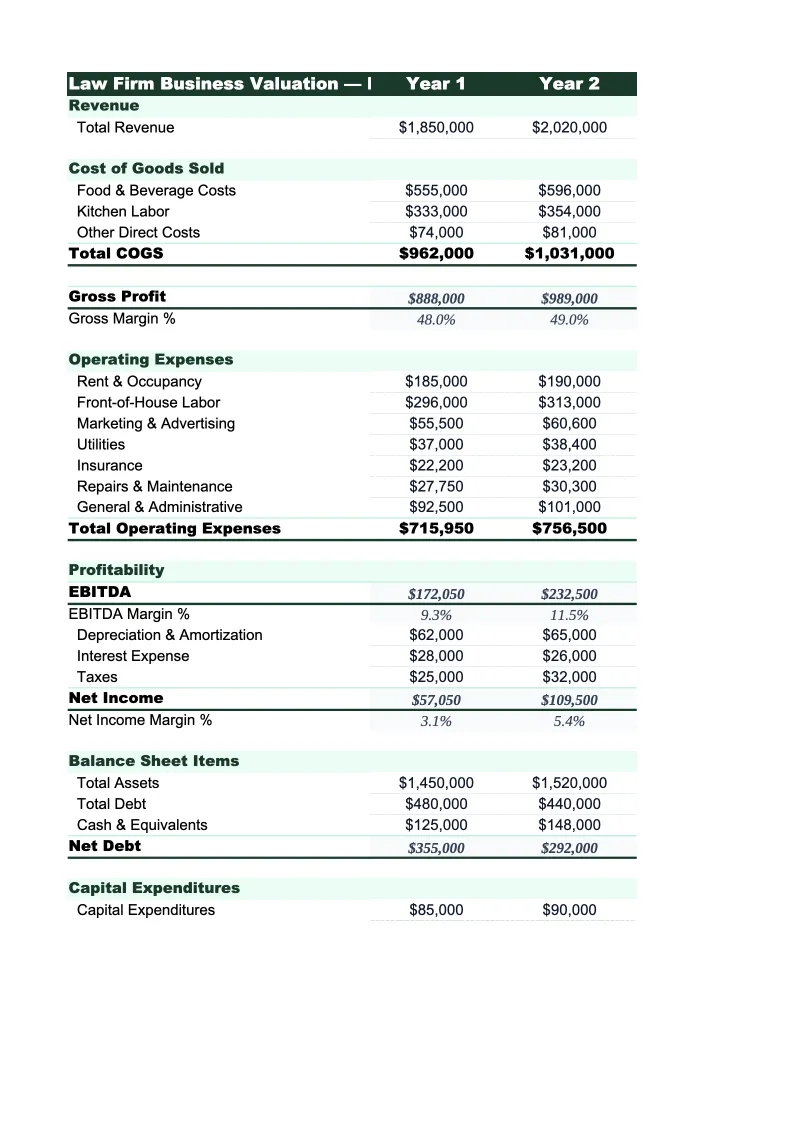

What's Inside This Law Firm Valuation Template

This template includes 6 worksheets, each designed for a specific part of your law firm financial workflow:

Business Inputs

The data entry foundation for every calculation in the model.

Revenue Multiple Approach

A top-down valuation method that establishes a broad value range using trailing twelve-month gross revenue.

SDE Multiple Approach

Seller's Discretionary Earnings is the primary income-based valuation method for solo practices and small law firms with a dominant principal.

Book of Business Analysis

The central risk assessment for any law firm transaction.

Attorney Dependency Scorecard

A structured scoring model for evaluating how much of the practice's revenue and client goodwill is transferable independent of the selling attorney.

Valuation Summary

A single-page output consolidating the revenue multiple approach and the SDE multiple approach into one view across conservative, base, and optimistic scenarios.

Law Firm Valuation Template Features

- Revenue multiple calculation benchmarked to law firm and legal practice transactions with retainer, hourly, and contingency revenue adjustments

- SDE normalization with full principal attorney compensation add-back, realization and collection rate adjustments, and a multiple selection matrix for legal practice value drivers

- Book of business portability analysis tracking top-15 client revenue share, engagement letter structure, and ABA Rule 1.17 compliance notes

- Attorney dependency scorecard scoring eight transferability factors including client loyalty, associate depth, referral network portability, and documented workflows

- Transition scenario comparison showing asset purchase, earnout structure, and full going-concern scenarios with client consent considerations

- Three-scenario valuation output with SDE sensitivity table showing the full negotiation band from 1.25x to 4.0x

How to Use This Law Firm Valuation Spreadsheet

Start with the Business Inputs sheet. Pull trailing twelve-month revenue from your practice management software or accounting system — most firms track hourly, flat fee, retainer, and contingency revenue in separate billing categories, and keeping them separate matters for valuation because each type commands a different multiple. Break out the principal attorney's total compensation completely: salary or guaranteed draws, any profit distributions, and personal expenses run through the firm (professional liability insurance for personal matters, personal vehicle, personal travel). You'll also need operational data: total billable hours per attorney in the trailing twelve months, your practice's blended realization rate (billed versus worked hours — typically 85–95% for efficient practices), and collection rate (collected versus billed — typically 90–98% for healthy practices). Active matter count, percentage of revenue from retainer clients, and headcount of associates or of-counsel attorneys who carry client matters independently all go into this sheet as well.

Work through the Revenue Multiple and SDE Multiple sheets, then complete the Book of Business Analysis and Attorney Dependency Scorecard. The book of business section is where most solo and small firm attorneys encounter the core tension in legal practice sales: nearly all of their billing relationships are with clients who came to them personally — through referrals, bar associations, previous firm relationships, or reputation in a specific practice area — and who may or may not continue with a new owner. Document each major client relationship honestly: whether it's governed by an engagement letter with the firm entity, whether the relationship would realistically follow the selling attorney to retirement or a successor practice, and the length of the engagement. The Attorney Dependency Scorecard then scores the factors a buyer or practice broker will walk through during diligence. Understanding your score in advance identifies the specific improvements — converting informal client relationships to formal firm retainers, helping associates develop independent client relationships, or documenting intake and case management workflows — that would increase the achievable multiple before going to market.

Know what your law practice is worth before you sell

Enter your billings, SDE, book of business data, and operational metrics — and get a defensible valuation range with the SDE approach, portability analysis, and attorney dependency scorecard that buyers will use to make their offer.

How Law Firms Are Valued When They Sell

Law firm valuations share the owner-dependency problem with consulting practices but add a layer of complexity unique to legal services: the professional relationship between an attorney and a client is not automatically transferable, and selling an active law practice requires compliance with state-specific ethics rules governing practice sales — most of which derive from ABA Model Rule 1.17. Clients of a selling attorney have the right to choose new counsel, to take their files, and to be notified of any change in the attorney who holds their matter. This means that even when a buyer purchases a practice's book of business, they are effectively purchasing the opportunity to be introduced to the clients — not a guaranteed revenue stream. Solo and small firm practices where clients chose the practice specifically for the principal attorney's expertise, courtroom reputation, or personal referral network face the most acute version of this risk, and it is the single largest factor that drives legal practice sale prices below what the firm's revenue figures might imply.

The factors that push a law firm valuation toward the higher end of the range reflect one underlying principle: revenue that doesn't depend on the selling attorney being present. Institutional clients — corporations, nonprofits, government agencies, and organizations that retain the firm for ongoing legal work under a master engagement agreement with the firm entity — represent the most transferable revenue because the relationship is with the firm, not with a specific attorney. Associates and of-counsel attorneys who carry their own matters independently, maintain direct client communication, and have established direct relationships with clients before the sale significantly reduce the dependency risk because the client's relationship with the firm is broader than the principal alone. Retainer agreements in practice areas where the legal service itself is relatively standardized — business formation, lease review, HR compliance, estate planning maintenance — are more transferable than contingency fee personal injury matters or complex commercial litigation where the principal's specific courtroom judgment is the product. And a documented case management system — documented intake processes, deadline tracking protocols, client communication standards — demonstrates to a buyer that the practice can be operated by someone other than the current principal.

Law Firm Industry at a Glance

Financial templates built for law firms and legal practices — from solo practitioners to mid-size firms. Pre-loaded with billing rate structures, matter tracking, and trust account categories.

Revenue Drivers

- Billable hours (hourly engagements)

- Flat fee matters

- Retainer agreements

- Contingency fee recoveries

Key Cost Categories

- Attorney compensation & draws

- Paralegal & staff salaries

- Malpractice insurance

- Legal research subscriptions (Westlaw, LexisNexis)

- Office rent & overhead

- Bar dues, CLE & licensing

Typical Margins

Gross: 40-60% · Net: 15-35%

Seasonality

Q4 typically busiest for transactional and corporate practices (year-end deals); litigation practices are more event-driven. January is slower across most practice areas.

Key Performance Indicators

Law Firm Valuation FAQ

More Law Firm Templates

Law Firm Balance Sheet Template for Excel

$29

Law Firm Budget Template for Excel

$29

Law Firm Business Plan Template for Excel

$39

Law Firm Cash Flow Template for Excel

$29

Law Firm Expense Tracker Template for Excel

$29

Law Firm Financial Model Template for Excel

$29

Law Firm Income Statement Template for Excel

$29

Law Firm Invoice Template for Excel

$29

Law Firm KPI Dashboard Template for Excel

$29

Law Firm P&L Template for Excel

$29

Law Firm Pro Forma Template for Excel

$29

Law Firm Project Budget Template for Excel

$29

Law Firm Sales Forecast Template for Excel

$29

Law Firm Valuation Template

$29