Nonprofit Valuation Template

Assess a nonprofit's financial health, sustainability, and organizational value using reserve analysis, donor concentration scoring, program efficiency ratios, and a structured framework for merger and acquisition conversations — built for how nonprofits actually change hands.

What's Inside This Nonprofit Valuation Template

This template includes 5 worksheets, each designed for a specific part of your nonprofit financial workflow:

Organization Inputs

The data entry foundation for the entire assessment.

Financial Health Scorecard

A structured assessment of the organization's financial condition across six dimensions that charity evaluators, foundation program officers, and merger partners use to assess organizational capacity.

Donor Concentration Analysis

A detailed look at the dependency and transferability of the organization's donor and funder base — the primary risk factor in any nonprofit merger, leadership transition, or sustainability assessment.

Asset-Based Approach

An estimation of the organization's tangible asset value, used primarily in merger and acquisition contexts where one nonprofit is acquiring another's programs, client base, or physical infrastructure.

Merger Valuation Summary

A single-page output consolidating the financial health score, donor concentration analysis, asset-based assessment, and program impact metrics into a structured merger or partnership discussion framework.

Nonprofit Valuation Template Features

- Financial health scorecard across six dimensions — operating reserve, program expense ratio, fundraising efficiency, government dependency, donor concentration, and revenue diversification — benchmarked to Charity Navigator and GuideStar standards

- Donor and funder concentration analysis tracking top-20 relationships by revenue share, grant renewal history, and transferability classification

- Asset-based valuation separating unrestricted liquid assets, restricted funds, endowment, real property, and intangible program assets

- Merger valuation summary comparing financial value, mission value, operational value, and funder relationship value as distinct components

- Sustainability trajectory assessment using three years of financial data to identify improving, stable, or declining organizational health

- Program integration complexity scoring based on client complexity, government contract terms, staff specialization, and geographic scope

How to Use This Nonprofit Valuation Spreadsheet

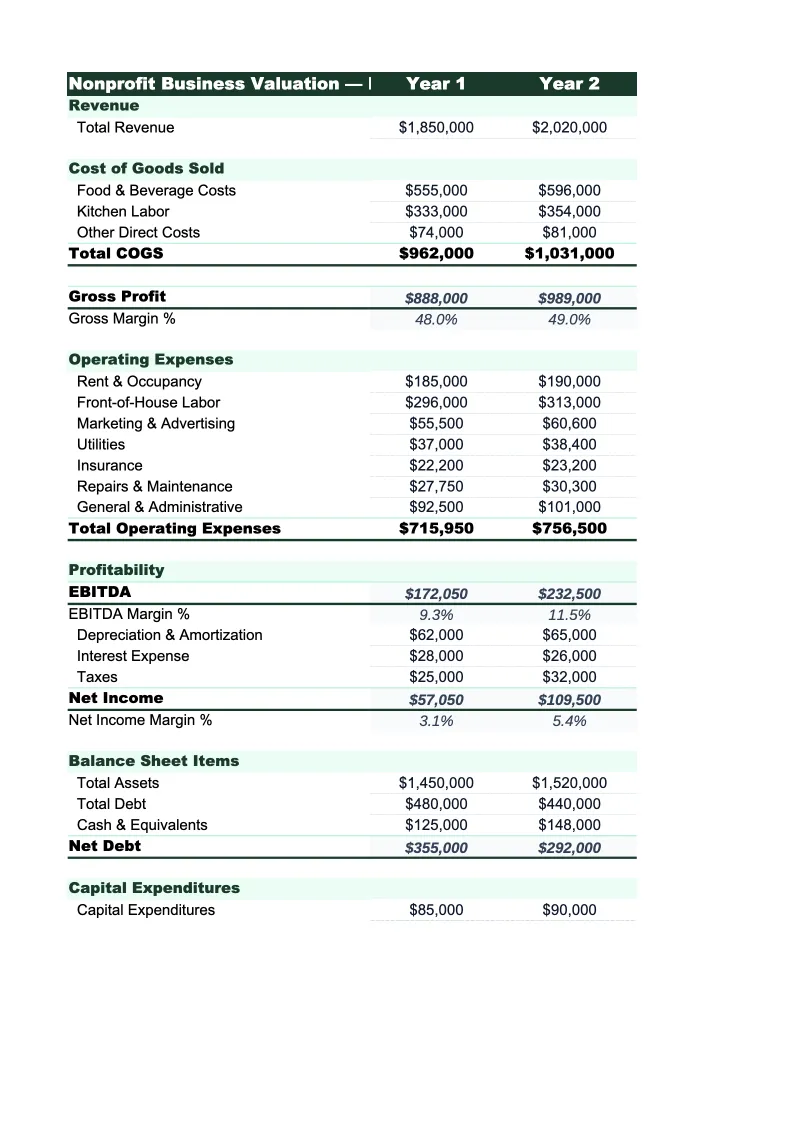

Start with the Organization Inputs sheet. Pull trailing twelve-month revenue data from your most recent audited financial statements or your accounting system — most nonprofits track revenue across government grants, foundation grants, individual donations, events, and earned income in separate general ledger accounts, and keeping them separated here matters because each source type carries a different risk profile. Enter balance sheet figures for net assets in all three categories: unrestricted, temporarily restricted, and permanently restricted. Operational metrics including active donor count, recurring donor count, and development staff headcount flow into the Financial Health Scorecard and Donor Concentration Analysis, so gather those from your CRM or donor database. If your organization has multiple program areas, enter program expenses by program so the program expense ratio reflects the true mission-delivery percentage.

Work through the Financial Health Scorecard, then complete the Donor Concentration Analysis. The scorecard will surface your organization's strengths and vulnerabilities across the six dimensions that foundation program officers, merger partners, and major donors use to assess organizational capacity. Pay particular attention to operating reserve — many nonprofits that feel financially stable are actually running with fewer than two months of reserve, which creates significant fragility in the event of a delayed grant payment or an unexpected expense. The Donor Concentration Analysis is where most organizations encounter uncomfortable clarity about dependency: if your top three funders represent 50% or more of contributed revenue, the organization's sustainability is highly sensitive to those specific relationships, and that risk needs to be understood and managed.

Know your organization's financial health before your next board meeting

Enter your revenue mix, net assets, donor concentration, and program expenses — and get a complete picture of operating reserve depth, fundraising efficiency, and organizational sustainability.

How Nonprofits Are Valued for Mergers and Sustainability Planning

Valuing a nonprofit organization is fundamentally different from valuing a for-profit business — there are no shareholders, no equity, and no purchase price changes hands. But nonprofits are valued all the time, in contexts that matter: foundation program officers assess organizational capacity before making multi-year grants; potential merger partners evaluate whether absorbing a smaller nonprofit would strengthen or strain the acquirer's finances; boards considering leadership transitions need to understand whether the organization's revenue base is transferable to a new executive director or is deeply dependent on the outgoing leader's personal relationships; and planned giving advisors need to assess whether the organization has the financial health to responsibly steward a bequest. In all of these contexts, what's being assessed is sustainability and mission-delivery capacity — not shareholder return. The key metrics that matter are operating reserve depth, program expense efficiency, fundraising cost structure, and how distributed or concentrated the revenue base is.

The characteristics that make a nonprofit financially healthy, and therefore valuable to funders and merger partners, cluster around a few core ratios. A program expense ratio above 70% signals that the organization is efficiently converting resources into mission delivery rather than consuming them in overhead — though ratios above 90% can indicate underinvestment in the administration and fundraising infrastructure needed to sustain operations. An operating reserve of 3–6 months of operating expenses is the most commonly cited benchmark for organizational resilience; it provides a buffer against delayed grant payments, unexpected legal or facility costs, or the loss of a major funder relationship. Fundraising efficiency below $0.20 per dollar raised indicates a healthy balance between development investment and return; costs above $0.35 per dollar raised suggest either significant infrastructure challenges or overreliance on expensive event-based fundraising. Revenue diversification — no single source above 35–40% of total revenue — is the structural characteristic that most clearly distinguishes sustainably funded nonprofits from those that are one government contract or one foundation relationship away from a financial crisis.

Nonprofit Industry at a Glance

Financial templates built for nonprofit organizations — from community foundations to service-delivery charities. Pre-loaded with fund accounting categories, grant tracking, and program expense ratios.

Revenue Drivers

- Grants (government & foundation)

- Individual donations

- Program fees

- Membership dues

- Special events

- Corporate sponsorships

Key Cost Categories

- Personnel & benefits

- Program expenses

- Administrative overhead

- Fundraising costs

- Occupancy

- Equipment & technology

Typical Margins

Gross: N/A · Net: 2-5% operating surplus

Seasonality

Grant cycles create Q1 and Q4 revenue spikes; year-end giving peaks in December. Fiscal years often run July–June rather than calendar year.

Key Performance Indicators

Nonprofit Valuation Template FAQ

More Nonprofit Templates

Nonprofit Balance Sheet Template for Excel

$29

Nonprofit Budget Template for Excel

$29

Nonprofit Business Plan Template for Excel

$39

Nonprofit Cash Flow Template for Excel

$29

Nonprofit Expense Tracker Template for Excel

$29

Nonprofit Financial Model Template for Excel

$29

Nonprofit Income Statement Template for Excel

$29

Nonprofit Invoice Template for Excel

$29

Nonprofit KPI Dashboard Template for Excel

$29

Nonprofit P&L Template for Excel

$29

Nonprofit Pro Forma Template for Excel

$29

Nonprofit Project Budget Template for Excel

$29

Nonprofit Sales Forecast Template for Excel

$29

Nonprofit Valuation Template

$29