SaaS Accounting Best Practices for Founders and Finance Teams

A practical guide to SaaS accounting — covering revenue recognition, deferred revenue, ASC 606, and the metrics that matter for investor reporting.

SaaS accounting has one fundamental problem that traditional business accounting doesn't: the timing mismatch between when customers pay and when revenue is earned.

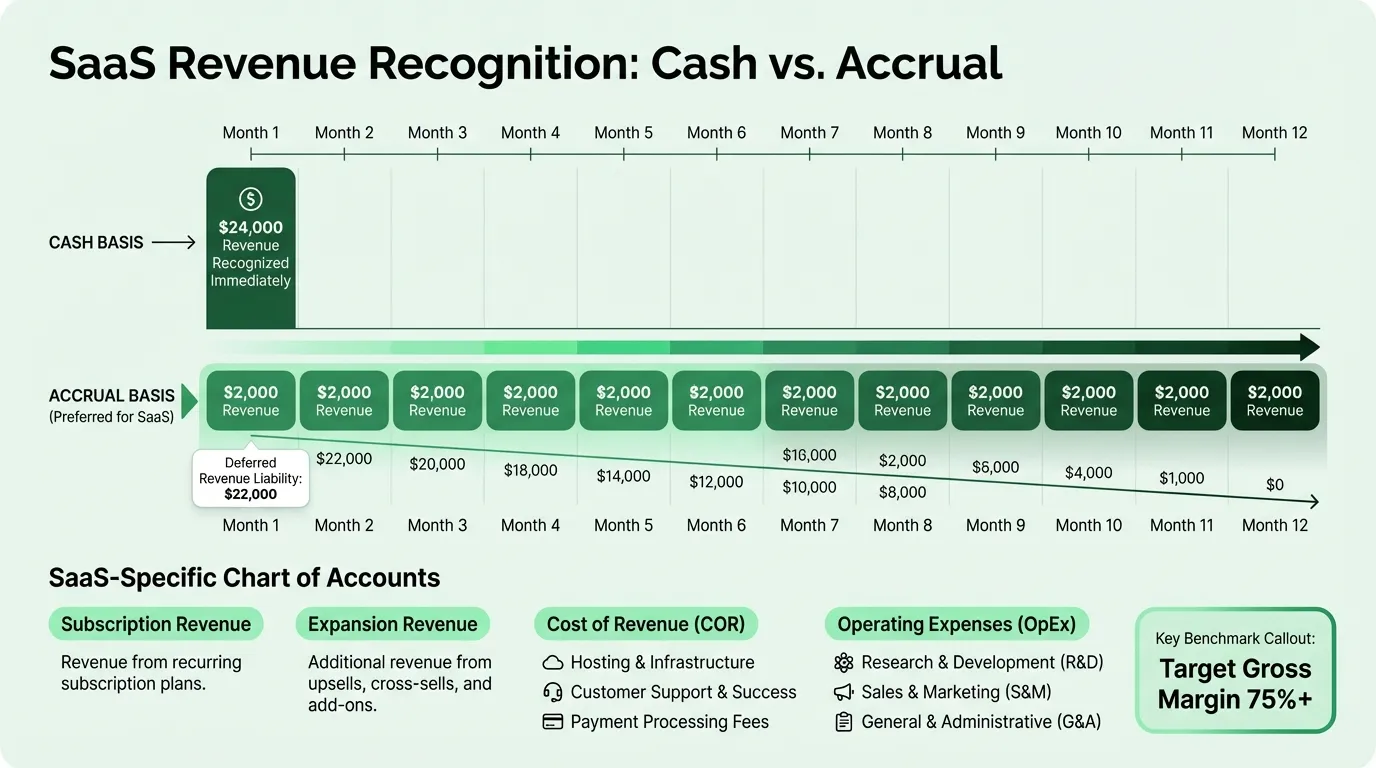

A customer who pays $24,000 upfront for a two-year subscription isn't generating $24,000 in revenue on day one. Under GAAP, they're generating $1,000 per month over 24 months. The remaining $23,000 sits on the balance sheet as a liability — deferred revenue — until the service is delivered. This distinction reshapes every financial statement your company produces and every metric investors use to evaluate it.

Get this foundation right and everything downstream — reporting, fundraising, due diligence — becomes straightforward. Get it wrong early and you'll eventually face an expensive restatement.

Why SaaS Accounting Is Different

Traditional product businesses recognize revenue when a transaction closes. You sell something, you invoice the customer, you record the revenue. These events happen at roughly the same time.

SaaS breaks this completely. A customer pays you before service is delivered, but you can't recognize that cash as revenue until you've actually provided the service. Every subscription renewal, upgrade, downgrade, or cancellation requires re-evaluating how revenue is recognized. A single contract can touch your books dozens of times over its life.

Three structural differences define SaaS accounting:

Revenue recognition is time-based, not transaction-based. Revenue is earned ratably over the subscription period. Twelve months of a $12,000 contract = $1,000/month in recognized revenue. Period.

Deferred revenue is a core balance sheet item. For companies with annual prepays, the deferred revenue liability can equal or exceed one full year of revenue. It's not a rounding error — it's a significant balance that must be reconciled every month.

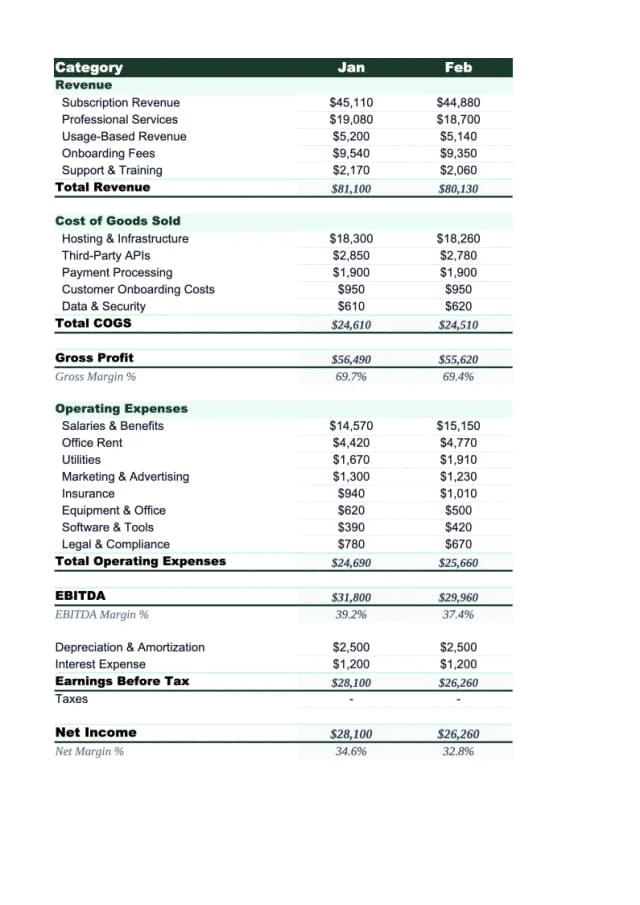

The metrics that matter aren't on a standard P&L. MRR, ARR, Net Revenue Retention, CAC, LTV, and churn rates are the numbers investors use to evaluate SaaS businesses. A generic P&L doesn't surface any of them. See how these metrics relate to the line items in our SaaS income statement example.

Switch to Accrual Accounting Before You Fundraise

Cash-basis accounting records income when cash is received and expenses when cash is paid. It's simple, but for a SaaS business it produces financials that misrepresent performance in both directions: a strong quarter of annual contract closings looks like an anomaly, and a quarter with few new closings looks weaker than it is.

Most advisors recommend switching to accrual accounting when your company approaches $3M ARR, is preparing for a fundraise, or when any institutional investor enters the picture. The better answer is to start with accrual from day one — the cost of building the right accounting structure early is far lower than the cost of restating prior-period financials before a Series A.

Under accrual accounting:

- Revenue is recognized as service is delivered, not when cash is received

- Expenses are recorded in the period they're incurred, not when the bill is paid

- Deferred revenue, accounts receivable, and prepaid expenses appear on the balance sheet

- Financial statements are comparable period-over-period in a way that cash-basis statements aren't

The practical implication: when a customer pays $60,000 for an annual subscription in January, your accrual P&L shows $5,000/month in revenue. Your cash flow statement shows the full $60,000 in January. Both are correct — they measure different things.

ASC 606: The Five-Step Framework

ASC 606 is the GAAP accounting standard that governs SaaS revenue recognition. If your company has investors, is preparing for fundraising, or is working toward an audit, compliance is required. The framework involves five steps:

- Identify the contract. Is there a signed agreement with enforceable rights and clear payment terms?

- Identify performance obligations. What distinct promises does the company owe? Core SaaS access, implementation services, training, and premium support may each be separate obligations requiring separate revenue allocation.

- Determine the transaction price. What will the company actually collect, accounting for discounts, variable fees, and refund provisions?

- Allocate the transaction price. For multi-element arrangements, split the price across each obligation based on standalone selling price (SSP).

- Recognize revenue. Record revenue as each obligation is satisfied — typically ratably over the subscription term for core SaaS.

The step that trips up most early-stage SaaS companies is step two. If implementation services are bundled with the subscription, are they a distinct performance obligation recognized upon completion — or part of the subscription bundle recognized ratably? The answer has significant revenue timing implications and requires documentation. Without documented revenue recognition policies, these judgments can't be audited or defended.

Build a SaaS-Specific Chart of Accounts

The default chart of accounts in QuickBooks or Xero is built for general businesses. It won't separate subscription revenue from professional services revenue, or cloud infrastructure costs from other operating expenses. That matters because investors scrutinize gross margin — and calculating it correctly requires the right account structure.

A SaaS chart of accounts separates:

Revenue accounts:

- Subscription revenue (core SaaS)

- Expansion revenue (upsells, add-ons, seat additions)

- Professional services revenue (implementation, onboarding, training)

- Non-recurring fees (setup fees, one-time charges)

Cost of revenue (COGS) — only what directly delivers the service:

- Hosting and cloud infrastructure

- Customer support payroll

- Third-party software embedded in the product

Operating expenses by function:

- Sales and marketing

- Research and development

- General and administrative

This structure makes it possible to calculate subscription gross margin separately from blended gross margin — a distinction investors care about. SaaS subscription gross margin should be 75% or higher. Professional services typically run 20-40% and should never be mixed into the subscription gross margin calculation. Check your margins against industry benchmarks with the SaaS profit margin calculator.

The SaaS P&L Template and SaaS Income Statement Template are structured with these categories separated.

Need a ready-made p&l template for your saas?

Download a pre-built spreadsheet with industry-specific categories, formulas, and formatting.

Track Deferred Revenue Every Month

Deferred revenue requires a monthly reconciliation. The journal entry flow:

- When cash is received: Debit Cash, Credit Deferred Revenue (liability)

- As service is delivered each month: Debit Deferred Revenue, Credit Subscription Revenue

The deferred revenue balance on your balance sheet should equal the total unearned future service obligation across all active contracts at any point in time. If a customer is 4 months into a 12-month prepaid contract, 8 months of their subscription value sits in deferred revenue.

For companies with annual contracts, this balance grows during high-renewal periods and shrinks over the following months. Watching it is useful: if deferred revenue is declining quarter over quarter despite new sales, it may signal a renewal/churn problem before it's visible in recognized revenue. Our SaaS balance sheet example shows how deferred revenue sits alongside other liabilities and what investors check first.

The SaaS Balance Sheet Template includes deferred revenue as a distinct current liability line with a tracking reconciliation.

The Metrics Investors Actually Use

Standard P&L metrics — net income, operating expenses, EBITDA — are secondary for SaaS evaluation. The metrics that drive investor decisions:

| Metric | What it measures | Benchmark |

|---|---|---|

| MRR | Monthly subscription revenue from active customers | Foundation for all SaaS financials |

| ARR | Annualized subscription run-rate (MRR × 12) | Primary valuation input |

| Net Revenue Retention (NRR) | Revenue retained + expansion from existing customers | 100-110% healthy; 110%+ best-in-class |

| Gross Margin | Subscription revenue minus direct COGS | 75%+ for software subscriptions |

| LTV:CAC | Lifetime value vs. cost to acquire a customer | 3:1 minimum; 4:1+ healthy |

| CAC Payback Period | Months to recover customer acquisition cost | Under 12 months elite; 15-18 months median |

| Rule of 40 | Revenue growth % + profit margin % | ≥40 is the benchmark |

NRR deserves particular attention. NRR above 100% means your existing customer base is growing on its own — upsells and expansions are offsetting churn. A company with 110% NRR can grow ARR without acquiring a single new customer. This is the metric that most clearly separates sustainable SaaS businesses from those that are leaking value.

The formula: (Starting MRR + Expansion MRR − Churned MRR − Contraction MRR) ÷ Starting MRR × 100.

The SaaS KPI Dashboard Template tracks MRR, ARR, NRR, churn, and CAC payback in a single view designed for monthly board reporting.

Common Accounting Mistakes to Fix Now

Recognizing revenue when cash hits the bank. The most common early mistake. A $60,000 annual prepay is not $60,000 in revenue — it's $5,000/month. Overstating revenue this way will surface during any investor diligence or audit, and correcting it retroactively is painful.

Treating bookings as revenue. Bookings are signed contract value — not earned revenue, not collected cash. "We signed $500K in Q3" is a bookings number. Recognized revenue for that quarter might be $50K if contracts started at different dates.

Not reconciling billing systems with accounting software. Stripe, Chargebee, or Recurly contains different representations of the same data as your accounting software. Without deliberate monthly reconciliation, discrepancies compound quietly. A billing configuration issue can halt invoicing for weeks before anyone notices.

Using a generic chart of accounts. If subscription revenue and professional services revenue sit in the same account, your gross margin is wrong. Fix this before the numbers matter — not during due diligence.

Ignoring capitalized software development costs. Under ASC 350-40, application development stage costs can be capitalized and amortized rather than expensed immediately. This distinction materially affects both your P&L and balance sheet. Engineering-heavy SaaS companies that expense all development costs may be understating assets and overstating expenses.

Delaying the switch to accrual. Every quarter you operate on cash basis is another quarter of financials that may need restatement. The longer you wait, the more expensive the correction. If you're also revisiting your monetization approach, our SaaS pricing best practices guide covers value metrics and tier structure.

The Financial Foundation

SaaS accounting isn't more complex than traditional accounting — it's differently complex. The revenue recognition rules, deferred revenue mechanics, and SaaS-specific metrics form a coherent system once you understand how they fit together. The companies that get into trouble are the ones that delay building this system until it's forced on them.

The core infrastructure: a SaaS-structured chart of accounts, accrual-basis financials, documented revenue recognition policies, a monthly deferred revenue reconciliation, and a KPI dashboard that tracks the metrics investors actually care about.

If you're building the financial model alongside this — projections, scenario planning, and investor-ready forecasts — the SaaS Financial Model Template covers ARR build, cohort modeling, and expense planning in a format designed for board and investor presentations. Need to present these financials to investors? Deckary makes consulting-grade PowerPoint slides.

Last updated: March 24, 2026

Frequently Asked Questions

Related Articles

Church Accounting Best Practices: A Practical Guide

How church accounting works — fund accounting, restricted funds, internal controls, financial reports, and the tax rules that catch churches off guard.

Church Balance Sheet Example: A Line-by-Line Breakdown

A complete church balance sheet example with real line items, fund accounting explained, and the benchmarks church boards use to assess financial health.

Construction Accounting: A Practical Guide for Contractors

Construction accounting is different from standard accounting. This guide covers job costing, WIP schedules, retainage, revenue recognition methods, and common mistakes.

Construction Balance Sheet Example: A Line-by-Line Breakdown

A complete construction company balance sheet example with real line items, WIP accounting, retainage, overbilling, and what sureties and lenders look for.

Daycare Balance Sheet Example: Line by Line

A complete daycare balance sheet example with real line items — enrollment deposits, playground equipment, subsidy receivables, and what the numbers mean.

Food Truck Balance Sheet Example: A Line-by-Line Breakdown

A complete food truck balance sheet example with real line items, truck depreciation rules, and what makes a food truck's financials different from a restaurant.