Moving Company Valuation Template

Value your moving company using SDE or EBITDA multiples, a fleet and equipment asset approach, DOT authority and license valuation, and an operations profile covering crew utilization, claims ratio, and customer concentration — built around the factors buyers and brokers actually use when pricing residential and commercial moving businesses.

What's Inside This Moving Company Valuation Template

This template includes 5 worksheets, each designed for a specific part of your moving company financial workflow:

Business Inputs

The data entry foundation for the entire valuation model.

Earnings Multiple Approach

Moving company valuations operate on two different earnings frameworks depending on the size and complexity of the business, and this sheet handles both.

Asset-Based Approach

A floor-value calculation based on the tangible and intangible assets a buyer would be acquiring — particularly relevant for moving company transactions because the fleet is the primary tangible asset, DOT authority has real value, and the replacement cost of building a licensed and insured moving operation from scratch is significant.

Operations Profile

Moving company valuations are heavily influenced by operational metrics that don't appear directly on the income statement but that experienced buyers and business brokers scrutinize because they determine whether the revenue and earnings are reliable and transferable.

Valuation Summary

A single-page output consolidating the earnings multiple approach and the asset-based floor into one view across conservative, base, and optimistic scenarios.

Moving Company Valuation Template Features

- Dual earnings multiple framework covering SDE multiples for owner-operated local movers (1.5–3.0x) and EBITDA multiples for larger operations with commercial accounts (2.5–4.5x), with a scoring matrix for five value drivers including owner dependency and claims ratio

- Fleet asset valuation entering each vehicle individually by make, model, year, mileage, and current market resale value — plus moving equipment, warehouse, and any owned real estate

- DOT authority and intangible asset section capturing the value of operating authority, carrier safety rating, commercial account contracts, and customer database as distinct line items in the asset-based approach

- Operations Profile sheet analyzing job count by move type, crew utilization rate, cargo claims ratio, customer concentration by account, and referral versus paid-lead revenue split

- Revenue concentration adjustment that discounts the base valuation for over-dependence on a single corporate relocation client — quantifying the risk that buyers will price in

- Three-scenario Valuation Summary with earnings multiple sensitivity table, DOT authority premium section, and deal structure comparison covering cash, seller financing, and twelve-month earnout arrangements

How to Use This Moving Company Business Valuation Spreadsheet

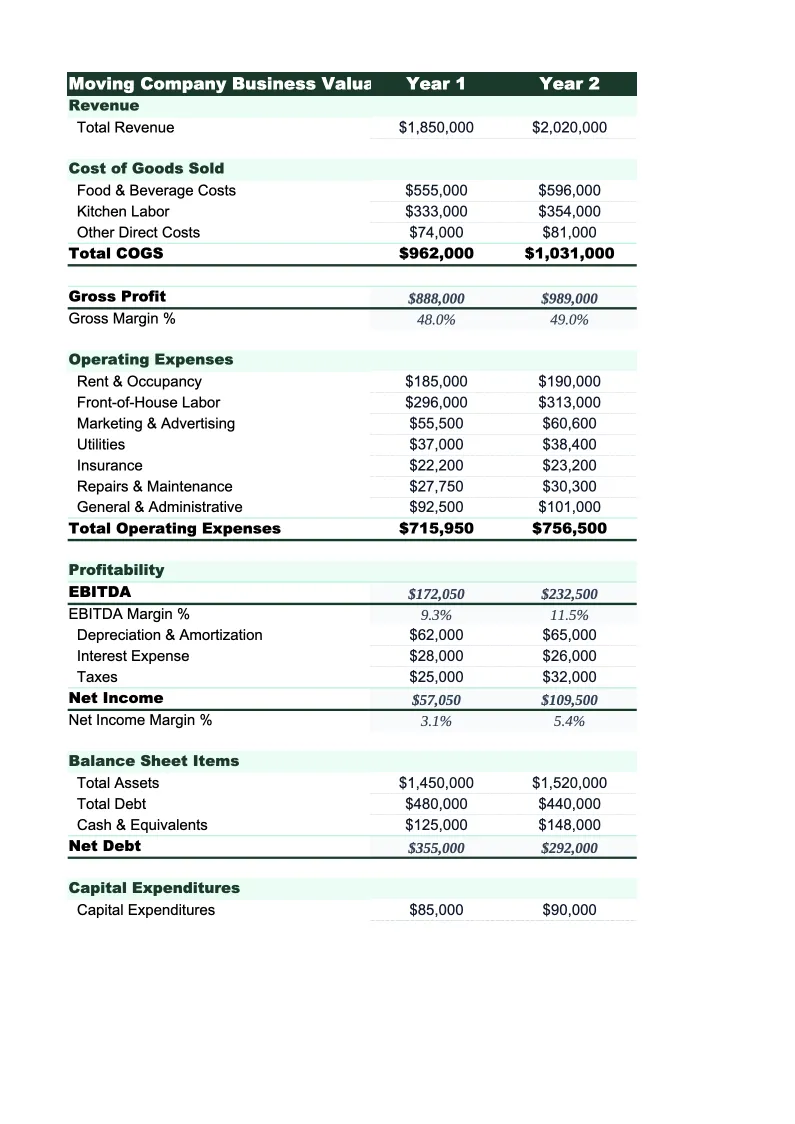

Start with the Business Inputs sheet. Pull your trailing twelve-month revenue broken down by move type — local residential, long-distance, commercial, and storage fees — from your job management system or accounting software. Separate these categories rather than entering a single revenue total, because they carry different margins and buyers value them differently. For the fleet section, gather each vehicle's year, make, model, and current mileage, then estimate current auction or dealer resale value for each unit — NADA or trade dealer quotes work well here, and being accurate matters more than being optimistic because buyers will verify fleet values during due diligence. Enter owner compensation fully: salary, any health insurance paid through the business, personal vehicles expensed through the company, and any other personal expenses running through the P&L.

Work through the Operations Profile sheet carefully before applying any multiple. Crew utilization, claims ratio, and customer concentration are the three metrics that will most directly affect where your operation falls in the multiple range — a claims ratio above 3% of revenue or a single corporate account representing more than 25% of total annual revenue will trigger hard questions from any experienced buyer and will compress the multiple they're willing to pay. Calculate your referral and repeat business percentage by reviewing the last two to three years of new customer sources: a business where 40–50% of new jobs come from past customer referrals and repeat relocations is significantly more defensible than one where most new business comes from paid lead generation, because the referral channel transfers with the business and the paid leads require ongoing marketing spend to sustain.

Know what your moving company is worth before you sell

Enter your revenue by move type, fleet values, earnings, and operations profile — and get a defensible valuation range with the earnings multiple approach, fleet asset floor, DOT authority premium, and customer concentration adjustment that buyers will use to structure their offer.

How Moving Companies Are Valued When They Sell

Moving company valuations differ from most service businesses in two important ways. First, the business has a significant asset base — the fleet — that buyers must finance or assume, and the age and condition of that fleet is a direct input into the offer price rather than just a due diligence concern. A moving company running ten-year-old trucks with deferred maintenance is a fundamentally different acquisition from one running a fleet purchased in the last three years, and buyers separate these clearly in their underwriting. Second, the business operates under federal and state regulatory frameworks — DOT operating authority, MC numbers for interstate carriers, state-level permits — that have real transfer value and that create meaningful barriers to entry for anyone trying to build a competing operation from scratch in the same market. This regulatory intangibility, while invisible on the balance sheet, is something experienced buyers assign value to explicitly.

The factors that move a moving company to the top of its multiple range are consistent across company sizes. Owner independence is the primary driver: a moving company where the owner handles daily dispatch, writes every estimate, and maintains all key commercial relationships personally is worth meaningfully less than one where trained office staff and a lead dispatcher handle daily operations under documented procedures. Buyers are acquiring a business, not hiring themselves into a job, and the cost of the owner's absence — whether from retirement, relocation, or simply stepping back — is the central risk they're pricing. Claims ratio is the second major driver: a clean safety and claims record reflects crew training quality, equipment maintenance discipline, and job selection practices, and it translates directly into lower insurance costs that a buyer will benefit from going forward. Revenue diversification matters at every scale — a company generating revenue across local residential, long-distance, and commercial moves with no single customer exceeding 15% of annual revenue is a substantially safer acquisition than one heavily dependent on a single corporate relocation contract.

Moving Company Industry at a Glance

Financial templates built for moving companies — from local movers to long-distance carriers. Pre-loaded with job-based billing, labor tracking, and the KPIs that matter for seasonal service businesses.

Revenue Drivers

- Local moves (hourly billing)

- Long-distance moves (flat-rate/weight-based)

- Packing services

- Storage and SIT fees

- Specialty item handling (pianos, safes)

- Valuation and liability coverage

Key Cost Categories

- Crew labor (field)

- Truck costs and fuel

- Insurance (cargo, liability, workers comp)

- Packing materials

- Marketing and lead generation

- Administrative labor

- Equipment maintenance

Typical Margins

Gross: 25-45% · Net: 7-10%

Seasonality

Peak season May–August accounts for ~60% of annual moves. June is the single busiest month. November–February is slowest; cash reserves built in summer cover winter operations.

Key Performance Indicators

Moving Company Valuation FAQ

More Moving Company Templates

Moving Company Balance Sheet Template for Excel

$29

Moving Company Budget Template for Excel

$29

Moving Company Business Plan Template for Excel

$39

Moving Company Cash Flow Template for Excel

$29

Moving Company Expense Tracker Template for Excel

$29

Moving Company Financial Model Template for Excel

$29

Moving Company Income Statement Template for Excel

$29

Moving Company Invoice Template for Excel

$29

Moving Company KPI Dashboard Template for Excel

$29

Moving Company P&L Template for Excel

$29

Moving Company Pro Forma Template for Excel

$29

Moving Company Project Budget Template for Excel

$29

Moving Company Sales Forecast Template for Excel

$29

Moving Company Valuation Template

$29