Roofing Balance Sheet Template

Track what your roofing company owns, owes, and is worth — a balance sheet built for contractors with vehicle and equipment schedules, AR aging for insurance claim jobs, and period-over-period comparison.

What's Inside This Roofing Balance Sheet Template

This template includes 4 worksheets, each designed for a specific part of your roofing financial workflow:

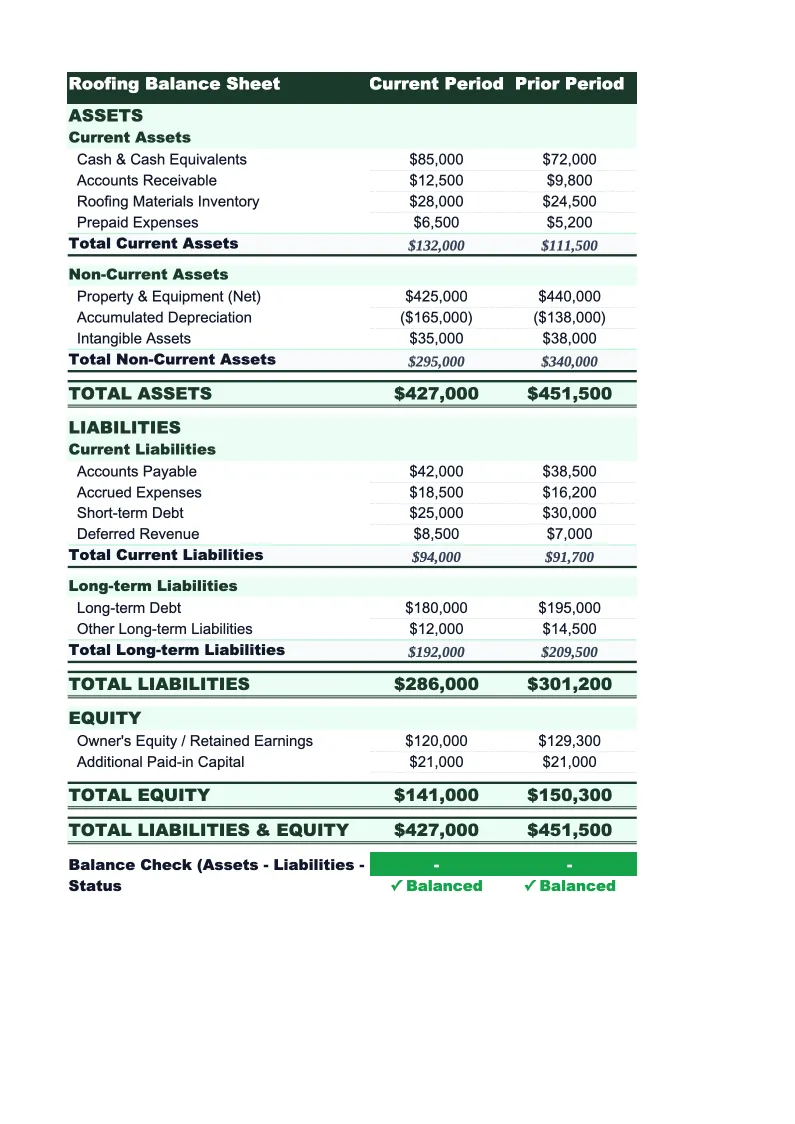

Balance Sheet

The core financial statement organized around the roofing contractor's chart of accounts.

Equipment & Vehicle Register

A fixed-asset register tracking every truck, trailer, aerial lift, and major piece of equipment the company owns.

AR Aging

An accounts receivable aging report that tracks every open job invoice by customer name, invoice date, job address, and invoice amount, then buckets each balance into aging columns: current (0–30 days), 31–60 days, 61–90 days, and 90+ days past due.

Period Comparison

A side-by-side view of two balance sheet dates — most commonly current year-end versus prior year-end, or a mid-year checkpoint against the same date last year.

Roofing Balance Sheet Template Features

- Balance sheet pre-loaded with roofing contractor asset and liability categories

- Equipment & vehicle register with straight-line depreciation for trucks, trailers, and lifts

- AR aging report with 0–30, 31–60, 61–90, and 90+ day buckets for insurance claim tracking

- Premium finance loan and workers comp liability tracked as separate current liability line items

- Accounting equation check — flags any imbalance automatically

- Year-over-year comparison view for bank renewals and financial reviews

How to Use This Roofing Balance Sheet Spreadsheet

Start with the Equipment & Vehicle Register. Pull your depreciation schedule from last year's tax return or your accounting software and enter each truck, trailer, and major piece of equipment with its purchase date, original cost, and useful life. The sheet calculates depreciation automatically and produces category totals that flow into the non-current assets section of the balance sheet. For most roofing companies, this is the most time-consuming setup step — but it only needs to be done once. After the initial entry, you're just adding new assets when you buy and removing old ones when you sell or retire them.

Next, complete the AR Aging sheet using your open invoices. List each unpaid job with the customer name, job address, invoice date, and amount. The sheet automatically buckets each balance by age and feeds the total into current assets on the balance sheet. Pay attention to the 60+ day column — insurance claim jobs frequently sit there while adjusters and mortgage companies process paperwork, and you need to distinguish between invoices that will collect and those that are genuinely at risk. Then fill in the Balance Sheet directly: pull cash from your bank statement, enter material inventory from your shop count, add prepaid insurance and supplier deposits, and match vehicle loan balances to the individual assets in your register.

15 minutes from download to your first roofing balance sheet

Download the template, enter your vehicles, open invoices, and account balances, and see your roofing company's full financial position — assets, receivables, equipment equity, and liabilities all in one place.

Why Every Roofing Contractor Needs a Balance Sheet Template

Roofing contractors face a balance sheet challenge that most service businesses don't: the combination of heavy capital investment in vehicles and equipment, highly variable receivables tied to insurance claim timelines, and large annual insurance premiums that create lump-sum prepaid assets or premium finance liabilities. A roofing company running $1.5 million in annual revenue might carry $300,000 in vehicle and equipment assets, $150,000 in open receivables, and $40,000 in prepaid insurance at any given time — yet many owner-operators have no structured way to see all of this on a single page. The result is decisions made based on bank balance alone, which is a poor proxy for financial health.

The receivables picture for roofing is genuinely more complicated than most trades. A straightforward residential repair job might collect in two weeks. A full replacement with a supplemented insurance claim can take 90–120 days: the initial payment comes in, the homeowner signs the check over and a supplement is filed, the mortgage company holds the depreciation amount until inspections are done, and the final check doesn't arrive until the job paperwork is fully closed. Tracking these balances in an AR aging report — separated from quick-pay cash jobs — gives you an accurate view of your real liquidity. Treating a 90-day insurance claim as equivalent to a 10-day cash job overstates how quickly that money is available.

Roofing Industry at a Glance

Financial templates built for roofing contractors — from owner-operators running residential crews to multi-crew companies handling commercial projects. Pre-loaded with materials, labor, and job-cost categories specific to the roofing industry.

Revenue Drivers

- Residential re-roofing (full replacements)

- Roof repairs and patching

- Commercial roofing projects

- Gutter installation and repair

- Insurance claim work

- Emergency repairs

Key Cost Categories

- Roofing materials (shingles, underlayment, flashing)

- Subcontractor and crew labor

- Disposal and dumpster rental

- Permit fees

- Equipment and tools

- Insurance (liability, workers comp)

- Vehicle and transportation

- Overhead and office costs

Typical Margins

Gross: 25-40% · Net: 6-15%

Seasonality

Peak season runs spring through early fall (April–October); storm events drive unpredictable surges year-round. November through March is the slow season in northern markets, though southern markets work year-round.

Key Performance Indicators

Roofing Balance Sheet Template FAQ

More Roofing Templates

Roofing Budget Template for Excel

$29

Roofing Business Plan Template for Excel

$39

Roofing Cash Flow Template for Excel

$29

Roofing Expense Tracker Template for Excel

$29

Roofing Financial Model Template for Excel

$29

Roofing Income Statement Template for Excel

$29

Roofing Invoice Template for Excel

$29

Roofing KPI Dashboard Template for Excel

$29

Roofing P&L Template for Excel

$29

Roofing Pro Forma Template for Excel

$29

Roofing Project Budget Template for Excel

$29

Roofing Sales Forecast Template for Excel

$29

Roofing Business Valuation Template for Excel

$29

More Balance Sheet Templates

Roofing Balance Sheet Template

$29