Real Estate Valuation Template

Estimate what your real estate brokerage, agency, or property management firm is worth using the three valuation methods buyers and lenders rely on — pre-built for commission-based and fee-based business models.

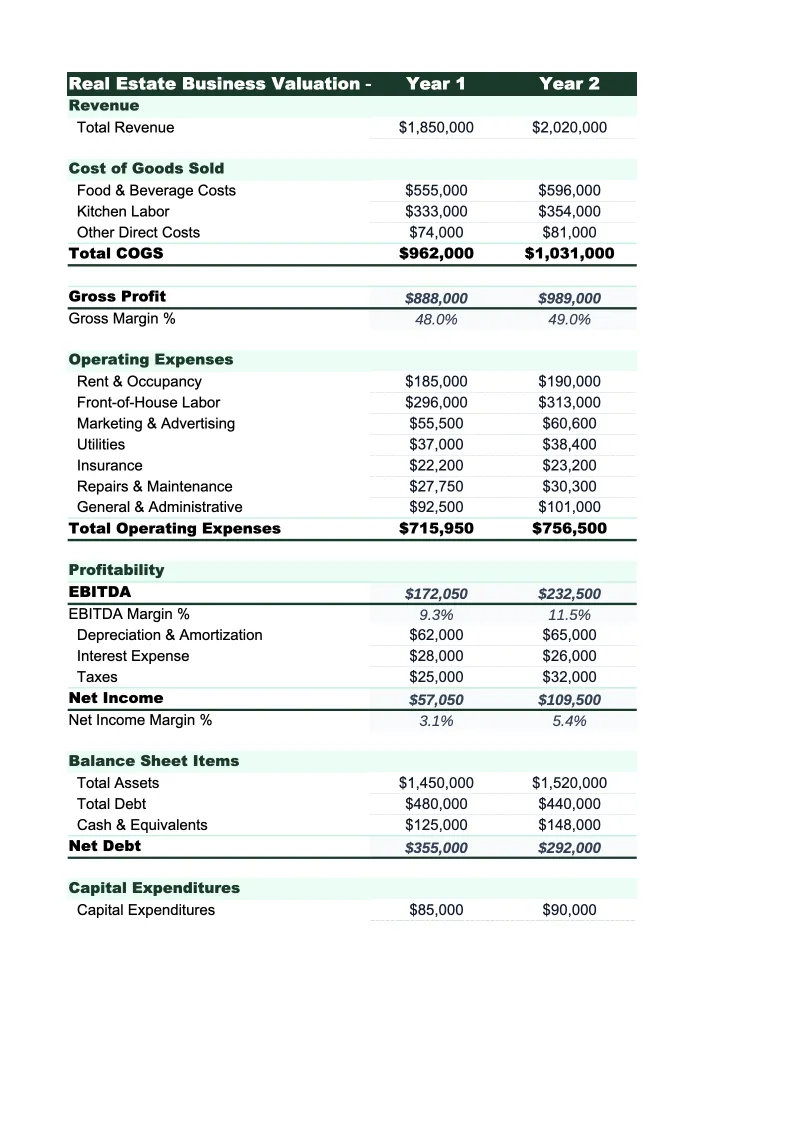

What's Inside This Real Estate Valuation Template

This template includes 5 worksheets, each designed for a specific part of your real estate financial workflow:

Income Approach

Values the business based on its normalized earnings power.

Market Approach

Values the business by comparing it to recent transactions in the real estate industry.

Asset Approach

Calculates the net asset value of the business — what you'd recover if you wound it down today.

Valuation Summary

Pulls results from all three methods and calculates a weighted average valuation.

Inputs & Assumptions

A single control panel where you enter the business metrics that feed all three valuation methods: three years of GCI and management fee revenue, agent count and per-agent productivity, owner compensation and add-backs, recurring vs.

Real Estate Business Valuation Template Features

- Three valuation methods: income (SDE/EBITDA), market multiples, and asset-based

- Separate multiple benchmarks for brokerages vs. property management companies

- Recurring vs. transactional revenue split affects multiple range automatically

- Owner compensation and add-back normalization for accurate SDE

- Weighted average with adjustable method weights and valuation range output

- DCF section with 5-year projection and terminal value for buyer-side modeling

How to Use This Real Estate Valuation Spreadsheet

Start with the Inputs & Assumptions sheet. Pull your last three years of income statements and identify your revenue mix — what percentage comes from closed transaction commissions versus recurring property management fees. This split is the single biggest driver of your multiple range, and getting it right upfront saves rework later. Enter your owner compensation and work through the add-back schedule: most real estate owners pay themselves above-market salaries, run personal vehicles through the business, or carry discretionary marketing expenses that won't transfer to a new owner. Each add-back increases your normalized earnings and directly affects the final valuation.

With inputs set, move to the Income Approach and Market Approach sheets. The income approach will give you an SDE or EBITDA multiple — review the multiple range suggested by the sheet and adjust if your situation warrants it. A brokerage with consistent agent retention and a growing property management division commands more than one where two top producers account for 40% of GCI. The Market Approach compares your metrics against recent industry transactions and helps you cross-check the income approach. Pay attention to the comparable multiple range — if your income approach lands outside the market range, investigate why before taking the number to a broker.

Know what your real estate business is worth

Download the template, enter your financials, and walk into any buyer, lender, or partner conversation with a number you can defend.

How Real Estate Businesses Are Valued

Real estate businesses come in two fundamentally different flavors when it comes to valuation: transaction-dependent brokerages and fee-based property management companies. A brokerage where revenue resets to zero at the start of each year because every sale has to be won anew is a very different asset from a property management firm collecting predictable monthly fees on 200 units. Buyers pay more for predictability, which is why property management companies routinely sell at higher multiples than residential brokerages of the same size. The distinction matters because many real estate businesses operate both models simultaneously, and the revenue mix significantly affects the blended multiple.

For transactional brokerages, the income approach using Seller's Discretionary Earnings (SDE) is the standard method. Small brokerages — one to five agents, owner-operated — typically sell for 1x–2.5x SDE. Larger brokerages with proven agent recruitment systems, strong brand presence, and low dependence on any single producer can reach 3x–4x EBITDA. The market approach using GCI multiples (typically 0.5x–1.5x) provides a useful cross-check. For property management companies, recurring management fees are valued like subscription revenue — 2x–4x annual recurring revenue is common, and companies with long-term management contracts and low client churn command the top of that range. The critical input is agent or client concentration: if 30% of revenue comes from one team or one property owner, buyers apply a discount.

Real Estate Industry at a Glance

Financial templates built for real estate professionals — agents, brokers, property managers, appraisers, and inspectors. Pre-loaded with commission tracking, management fee structures, and transaction-based billing.

Revenue Drivers

- Sales commissions

- Property management fees

- Lease-up / tenant placement fees

- Appraisal & inspection fees

Key Cost Categories

- MLS & licensing fees

- Marketing & advertising

- E&O insurance

- Transaction coordination

- Technology & CRM

- Office & brokerage fees

Typical Margins

Gross: 40-70% · Net: 15-35%

Seasonality

Peak activity spring through summer (March–August); winter slowdown, especially December–January. Commercial real estate has less pronounced seasonality.

Key Performance Indicators

Real Estate Business Valuation FAQ

More Real Estate Templates

Real Estate Balance Sheet Template for Excel

$29

Real Estate Budget Template for Excel

$29

Real Estate Business Plan Template for Excel

$39

Real Estate Cash Flow Template for Excel

$29

Real Estate Expense Tracker Template for Excel

$29

Real Estate Financial Model Template for Excel

$29

Real Estate Income Statement Template for Excel

$29

Real Estate Invoice Template for Excel

$29

Real Estate KPI Dashboard Template for Excel

$29

Real Estate P&L Template for Excel

$29

Real Estate Pro Forma Template for Excel

$29

Real Estate Project Budget Template for Excel

$29

Real Estate Sales Forecast Template for Excel

$29

Real Estate Valuation Template

$29