SaaS Valuation Template

Value your SaaS company using ARR multiples, discounted cash flow, and Rule of 40 scoring — with benchmarks calibrated to current software M&A markets.

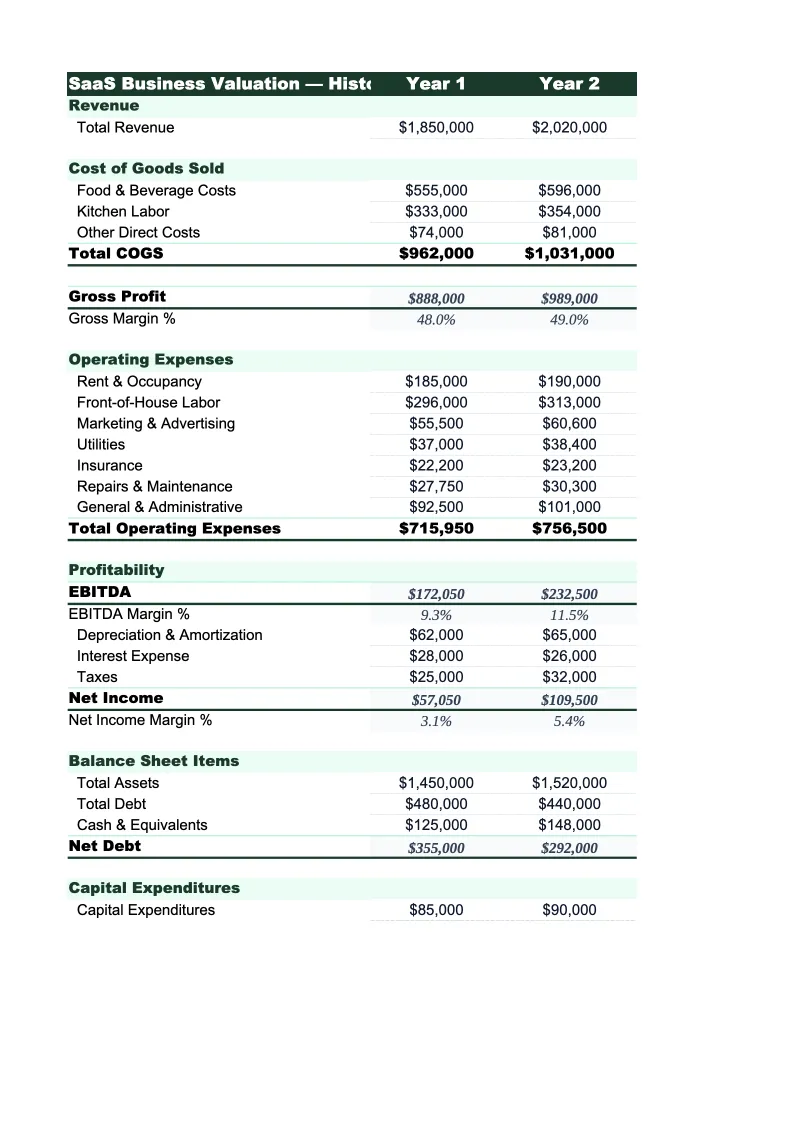

What's Inside This SaaS Valuation Template

This template includes 5 worksheets, each designed for a specific part of your saas financial workflow:

Company Inputs

The starting point for your entire valuation.

ARR Multiple Approach

The primary valuation method for most SaaS companies.

DCF Model

A five-year discounted cash flow model built around SaaS unit economics.

Comparable Transactions

A reference table of recent SaaS M&A transactions and public company trading multiples to help you contextualize your own valuation.

Valuation Summary

A single-page output that pulls the results from each valuation method and calculates a weighted average.

SaaS Valuation Template Features

- ARR multiple valuation with Rule of 40 scoring and multiple selection matrix

- 5-year DCF model built for SaaS revenue and cost structure

- Net revenue retention (NRR) and gross margin inputs that adjust valuation range

- Comparable transaction table with SaaS M&A benchmarks by ARR tier

- Three-scenario output: conservative, base, and optimistic

- Sensitivity table showing valuation impact of multiple changes in 0.5x increments

How to Use This SaaS Valuation Spreadsheet

Start with the Company Inputs sheet. Enter your current ARR, trailing twelve-month revenue, gross margin, ARR growth rate, and net revenue retention. If you have EBITDA or operating income data, enter that too — it affects both the multiple selection and the DCF. The inputs sheet takes about 10 minutes to fill out if you have your financials handy. Everything else in the template pulls from here, so it's worth getting these numbers right before moving on.

Next, work through the ARR Multiple Approach sheet. Review the multiple selection matrix and find the row that matches your growth rate and gross margin tier. The template will highlight a suggested multiple range based on your Rule of 40 score, but you can override this with your own assumption. Adjust the low, mid, and high multiple inputs to bracket your valuation range. Then move to the DCF sheet and enter your five-year revenue growth assumptions and margin profile — for early-stage companies, it's fine to project negative EBITDA for the first few years.

15 minutes from download to your SaaS valuation

Enter your ARR, growth rate, and margins — and see your company's valuation range across multiple methods, with benchmarks to back it up.

Why SaaS Valuations Work Differently

SaaS companies are valued differently from most businesses because the financials that matter most aren't on the income statement — they're in the subscription metrics. ARR growth rate, net revenue retention, gross margin, and the Rule of 40 score collectively drive the ARR multiple that buyers and investors apply. A SaaS company growing at 50% with 120% NRR and 75% gross margins might command 10x ARR or more. The same company at 15% growth with 85% NRR and 65% margins might see 2–3x. Understanding which inputs move the needle is the whole point of a valuation model.

The Rule of 40 — growth rate plus EBITDA margin — has become the most widely cited benchmark for SaaS health. Companies scoring 40 or above are generally rewarded with premium multiples in both public markets and private M&A. But the rule has nuance: a company at 80% growth and -40% EBITDA scores the same as a company at 20% growth and +20% EBITDA, and buyers treat these very differently. The template captures this by showing your Rule of 40 score alongside your gross margin and NRR, so you can see the full picture of what's driving (or limiting) your multiple.

SaaS Industry at a Glance

Financial templates built for software-as-a-service businesses managing subscription billing, ARR growth, and recurring revenue operations.

Revenue Drivers

- monthly recurring revenue (MRR)

- annual contract value (ACV)

- seat-based or usage-based billing

- professional services and onboarding fees

- add-ons and tier upgrades

Key Cost Categories

- cloud infrastructure (AWS, GCP, Azure)

- employee salaries and benefits (engineering, sales, CS, marketing)

- customer acquisition (ads, events, SDR costs)

- SaaS tools and subscriptions

- payment processing fees

- R&D and product development

Typical Margins

Gross: 60-80% · Net: -5% to 20% depending on growth stage

Seasonality

Relatively flat month-to-month with Q4 spikes from enterprise budget cycles. Annual contract renewals cluster in January and July.

Key Performance Indicators

SaaS Valuation Template FAQ

More SaaS Templates

SaaS Balance Sheet Template for Excel

$29

SaaS Budget Template for Excel

$29

SaaS Business Plan Template for Excel

$39

SaaS Cash Flow Template for Excel

$29

SaaS Expense Tracker Template for Excel

$29

SaaS Financial Model Template for Excel

$29

SaaS Income Statement Template for Excel

$29

SaaS Invoice Template for Excel

$29

SaaS KPI Dashboard Template for Excel

$29

SaaS P&L Template for Excel

$29

SaaS Pro Forma Template for Excel

$29

SaaS Project Budget Template for Excel

$29

SaaS Sales Forecast Template for Excel

$29

SaaS Valuation Template

$29