Pest Control Valuation Template

Value your pest control business using SDE or EBITDA multiples, a recurring revenue analysis capturing RMR, attrition, and contract mix, an equipment and route asset approach, and a roll-up acquirer pricing model — built around the factors strategic buyers and independent acquirers actually use when pricing residential and commercial pest control operations.

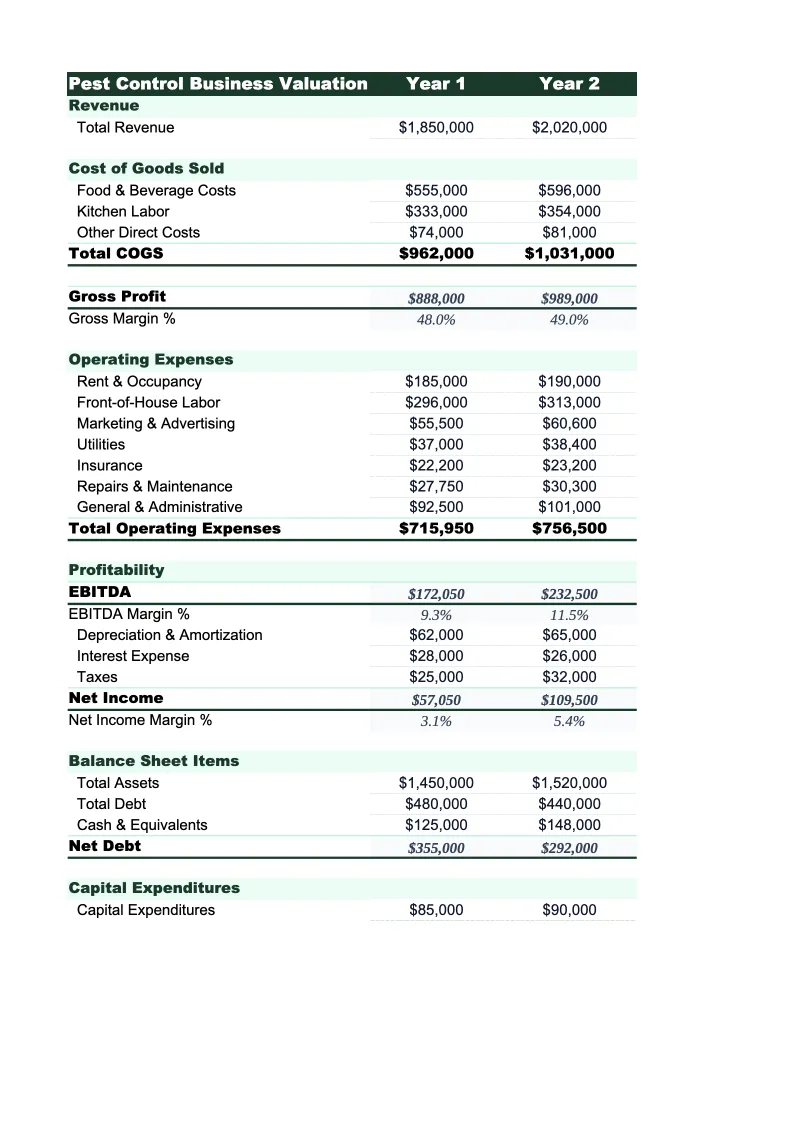

What's Inside This Pest Control Valuation Template

This template includes 5 worksheets, each designed for a specific part of your pest control financial workflow:

Business Inputs

The data entry foundation for the entire valuation model.

Recurring Revenue Analysis

The most important sheet in the model for pest control valuations, because the quality and stability of recurring contract revenue is the central driver of what buyers — particularly strategic acquirers and regional roll-up operators — are willing to pay.

Earnings Multiple Approach

Pest control business valuations apply different frameworks depending on the size and recurring revenue mix of the operation.

Asset-Based Approach

A floor-value calculation based on the tangible and intangible assets a buyer would be acquiring in a pest control transaction.

Valuation Summary

A single-page output consolidating the earnings multiple approach and the asset-based floor into one view across conservative, base, and optimistic scenarios.

Pest Control Valuation Template Features

- Recurring Revenue Analysis sheet calculating RMR by service category, annual attrition rate, average contract value, and recurring-to-total revenue ratio — the metrics strategic acquirers and roll-up operators use to price pest control acquisitions

- Dual earnings multiple framework covering SDE multiples for owner-operated residential operations (2.5–4.5x) and EBITDA multiples for larger managed businesses (4.0–7.0x), with a five-factor scoring matrix including recurring revenue quality, attrition rate, owner dependency, and route density

- Contract book intangible asset section calculating value from active contract count, average monthly billing, and an industry-standard contract multiplier (8–14x monthly billing) — typically the largest single asset component in a pest control transaction

- Roll-up acquirer premium section showing strategic buyer valuation alongside individual buyer valuation, with an RMR multiple comparison calibrated to industry transaction benchmarks (10–18x monthly recurring revenue for high-retention operations)

- License transferability risk assessment evaluating whether pesticide applicator licenses are held by the owner or transferable employees, and estimating the earnout or license acquisition condition that buyers impose when owner-held licenses are required for operation

- Three-scenario Valuation Summary with earnings multiple sensitivity table, attrition rate sensitivity analysis, individual versus strategic buyer value comparison, and deal structure section covering cash purchase, seller financing, and RMR-tied earnout arrangements

How to Use This Pest Control Business Valuation Spreadsheet

Start with the Business Inputs sheet. Pull your trailing twelve-month revenue by service category from your route management software or accounting system — separating recurring GPP contract revenue from termite, specialty, and one-time treatment revenue is critical because buyers value these streams differently and the Recurring Revenue Analysis sheet needs them disaggregated. For recurring service revenue, gather your active account count by service type (residential GPP, termite monitoring, mosquito programs, commercial accounts) and your average annual contract value per category — most route management systems can export this in a few minutes. Enter owner compensation fully and accurately: salary, any vehicle expenses, health insurance, and personal expenses running through the P&L, because the SDE normalization depends on these figures. For the vehicle and equipment section, collect each vehicle's year, make, and current market value using trade or auction references, and estimate the replacement value of spray equipment and tools.

The Recurring Revenue Analysis sheet requires the most careful attention because it drives the most important outputs. Calculate your annual customer attrition rate accurately by counting accounts that cancelled or did not renew over the last twelve months divided by active accounts at the start of that period — use your CRM or route management system export rather than estimating. This number matters more than almost any other input: the difference between 12% annual attrition and 22% annual attrition can move a pest control valuation by 20–35% when buyers are comparing your operation to their acquisition benchmarks. Enter your commercial account revenue by client tier and calculate concentration — if a single commercial account represents more than 10–15% of total annual revenue, flag it for the deal structure conversation, because buyers will either discount the multiple or propose an earnout tied to that account's retention. Review the recurring-to-total revenue ratio the sheet calculates; if your operation is below 60% recurring, there's genuine upside from converting more one-time customers to annual contracts before selling.

Know what your pest control business is worth before you sell

Enter your revenue by service category, recurring contract metrics, attrition rate, and owner compensation — and get a defensible valuation range with the earnings multiple approach, contract book intangible, roll-up acquirer premium, and license transferability risk assessment that buyers will use to structure their offer.

How Pest Control Businesses Are Valued When They Sell

Pest control business valuations are driven by one factor more than any other: the quality and stability of the recurring contract base. Unlike most service businesses that sell time or complete one-time projects, pest control operations built around annual or quarterly service agreements generate predictable, foreseeable revenue that buyers can model forward with confidence. The larger and more acquisitive buyers in this industry — national operators, regional roll-up platforms, and private equity-backed consolidators — have refined this insight into a precise methodology: they price acquisitions primarily on recurring monthly revenue (RMR) or annualized contract value (ACV), then apply a multiplier calibrated to the attrition rate, geographic density, and commercial account mix of the operation. An independent owner who doesn't understand this framework is likely to be negotiating against a buyer who understands it in significant detail.

The variables that determine where a pest control business lands in the multiple range are consistent across company sizes. Customer attrition is the primary driver: annual cancellation rates below 15% signal a retention-focused, referral-driven business that buyers can acquire with confidence in the projected revenue stability, while attrition rates above 25% signal customer satisfaction problems, promotional pricing dependency, or service quality issues that will cost the buyer money to repair. Owner dependency is the second driver: a pest control operation where trained technicians handle daily service delivery, office staff manage scheduling and customer communication, and managers oversee route quality is worth substantially more than one where the owner personally handles commercial sales, key account management, or customer retention calls. Route density matters operationally and financially — compact, geographically efficient routes produce higher revenue per technician per day and lower vehicle costs, which means more earnings available to support a higher multiple. Pesticide applicator license transferability is a structural risk that many sellers don't anticipate: if the owner personally holds the required licenses and no other employee is licensed, a buyer faces a mandatory condition involving either an earnout period or a requirement to hire a licensed qualifier before close, which they will price into the offer.

Pest Control Industry at a Glance

Financial templates built for pest control businesses — from solo operators to multi-route companies. Pre-loaded with recurring contract, termite, and specialty treatment categories.

Revenue Drivers

- Recurring GPP contracts

- Termite treatments and monitoring

- Bed bug and specialty treatments

- Rodent control and exclusion

- Mosquito and tick programs

- Commercial pest control contracts

Key Cost Categories

- Technician wages and payroll taxes

- Pesticides, rodenticides, and materials

- Vehicle fuel and fleet maintenance

- Liability and commercial auto insurance

- Pesticide applicator license fees

- Route management and CRM software

Typical Margins

Gross: 45-60% · Net: 10-20%

Seasonality

Spring through fall drives new contract sign-ups and mosquito/tick program revenue; core GPP and commercial contracts provide year-round base revenue; termite swarm season (March–June) is a major driver of new termite treatment sales.

Key Performance Indicators

Pest Control Business Valuation FAQ

More Pest Control Templates

Pest Control Balance Sheet Template for Excel

$29

Pest Control Budget Template for Excel

$29

Pest Control Business Plan Template for Excel

$39

Pest Control Cash Flow Template for Excel

$29

Pest Control Expense Tracker Template for Excel

$29

Pest Control Financial Model Template for Excel

$29

Pest Control Income Statement Template for Excel

$29

Pest Control Invoice Template for Excel

$29

Pest Control KPI Dashboard Template for Excel

$29

Pest Control P&L Template for Excel

$29

Pest Control Pro Forma Template for Excel

$29

Pest Control Project Budget Template for Excel

$29

Pest Control Sales Forecast Template for Excel

$29

Pest Control Valuation Template

$29